The economy is presenting us with a mixed picture lately. The jobs numbers are showing underlying strength, but inflation remains sticky, and the Fed, in response, has committed itself to a policy of high-interest rates and monetary tightening. Consumer spending is still strong, but savings rates and credit availability are both down. And with an election just one year away and geopolitical crises flashing hotter every day, the only certainty is uncertainty.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

For David Kostin, chief US equity strategist from Goldman Sachs, the overall outlook for stocks is not as grim as that picture might have it. Kostin sees opportunities ahead and believes that with careful investment strategies, investors can still find potential for growth and profitability in the current market conditions.

“‘Higher for longer’ means that highly levered stocks will continue to face cash flow headwinds and that equity valuations are unlikely to expand meaningfully from current levels. However, a key reason our economists expect interest rates to remain elevated is the demonstrated resilience of the economy to current elevated policy rates and the expectation that this resilience continues. Our economists’ 2024 real GDP growth forecast of 2% compares with a consensus forecast of 1%. We, therefore, remain wary of long-duration and highly levered stocks but think investors should treat cyclical sell-offs as a buying opportunity.”

The stock analysts at Goldman, following this lead, have picked out three stocks that are primed for gains in the year ahead. And it’s not only the Goldman experts who are showing confidence in this trio. When checking the TipRanks database, we find that analyst consensus rates all three as ‘Strong Buys’ as well. Let’s see why investors might want to consider loading up on these stocks right now.

Taiwan Semiconductor Manufacturing (TSM)

We’ll start with one of the tech world’s major players, Taiwan Semiconductor. This company, with its $455 billion market cap, holds an important role in the semiconductor industry – it is a leader in the foundry business, an advanced semiconductor manufacturer that produces mass runs as a third-party contractor for other chip firms and their customers.

TSM is a giant in Taiwan’s chip industry, and that small island is already producing more than 60% of the world’s semiconductor output. TSM’s share of its home country’s chip production stands near 56%. Some numbers show the scale of the operation: TSM uses 288 different process technologies to produce more than 12,698 chip products – for hundreds of customers.

A look at the macro picture, the company’s revenue and earnings, shows that in Q323, the last reported quarter, TSM had a top line of US$16.89 billion. This was down more than 10% year-over-year, but beat the forecast by almost US$183 million. The company’s EPS, of US$1.29 per American Depositary Share, was 12 cents per share better than had been expected.

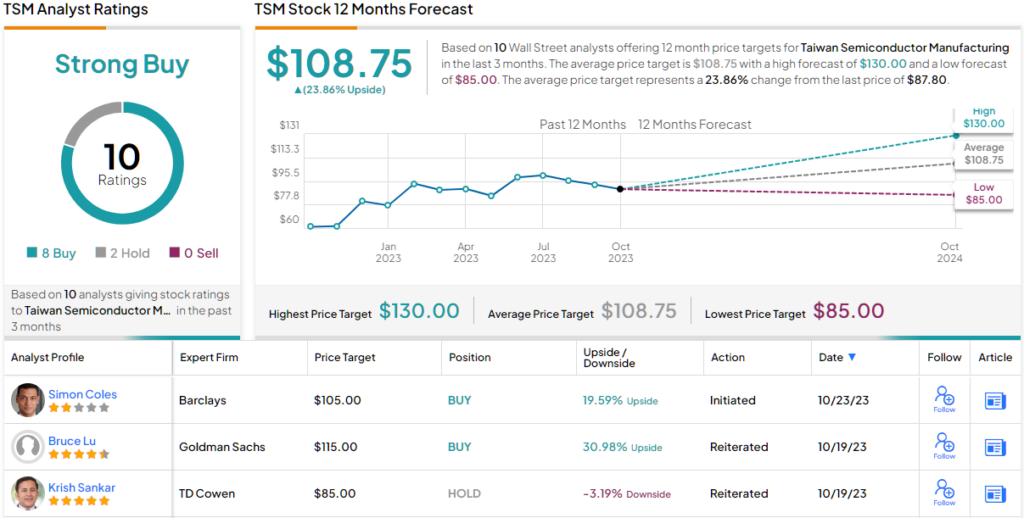

The company’s scale and market share have earned it a spot on the Goldman Sachs conviction list. Firm analyst Bruce Lu believes that Taiwan Semiconductor presents a sound option for investors. He writes of the company, “We like TSMC as we think its solid technology leadership and execution better position it vs. peers to capture the industry’s long-term structural growth, particularly in areas such as 5G/AI/HPC/EV. In addition, the valuation looks attractive, with the shares trading at the lower end of their 10-year trading history. Furthermore, we view TSMC as the key AI enabler among our Taiwan semi coverage thanks to its leadership stance in leading-edge nodes and advanced packaging technology – CoWoS (chip on wafer on substrate).”

For Lu, this adds up to a Buy rating and a $115 price target that implies a 12-month gain of 31% for TSM. (Watch Lu’s track record)

In general, the rest of the Street is on the same page. With 8 Buys and 2 Holds received in the last three months, the consensus rating on TSM comes in as a Strong Buy. TSM shares are trading for $87.80 and carry a $108.75 average target price, which together imply the stock will appreciate ~24% in the coming year. (See TSM stock forecast)

SharkNinja, Inc. (SN)

From semiconductors, we’ll shift our focus to the world of home appliances with SharkNinja. This company, which was founded in 1994, gets its name from its two main brands – Shark, which is known for its high-end vacuum cleaners, and Ninja, which offers lines of small kitchen appliances, everything from indoor grills to blenders and smoothie makers. SharkNinja operated under the aegis of JS Global Lifestyle Company Limited, but at the end of July this year, it completed a separation from the parent firm and went public.

The company has put up some impressive numbers over the years, and currently holds more than 3,000 patents covering 27 product sub-categories, and sells in 26 markets worldwide. The company generated approximately $3.7 billion in revenues last year, operating through a network of more than 150 global retailers, as well as selling through its own website. From 2008 through 2022, SharkNinja saw a net sales CAGR of 20%.

The company reported $950.3 million in net sales for 2Q23, the last quarter before going public, for a 22% year-over-year gain. SharkNinja will report its Q3 results, the first as a publicly traded firm, on November 9. The Street is expecting to see $1 billion in revenues.

Covering this stock for Goldman is analyst Brooke Roach, who sees SharkNinja’s history as a strong foundation to build on a public firm. He writes, “SN has a solid history of growth across categories and product lines. Looking ahead, we believe the company’s innovation focus will enable growth even against a choppy macro backdrop, evidenced by SN’s ability to outperform peers in 2022 and 2023 YTD on strength in beauty/outdoor.”

Roach goes on to outline a likely trajectory that investors should approve, saying, “We see significant margin opportunity on the horizon, with near-term profit set to benefit from transitory cost recapture tailwinds (freight and input costs), while longer-term EBIT margins can benefit from leverage and marketing efficiency.”

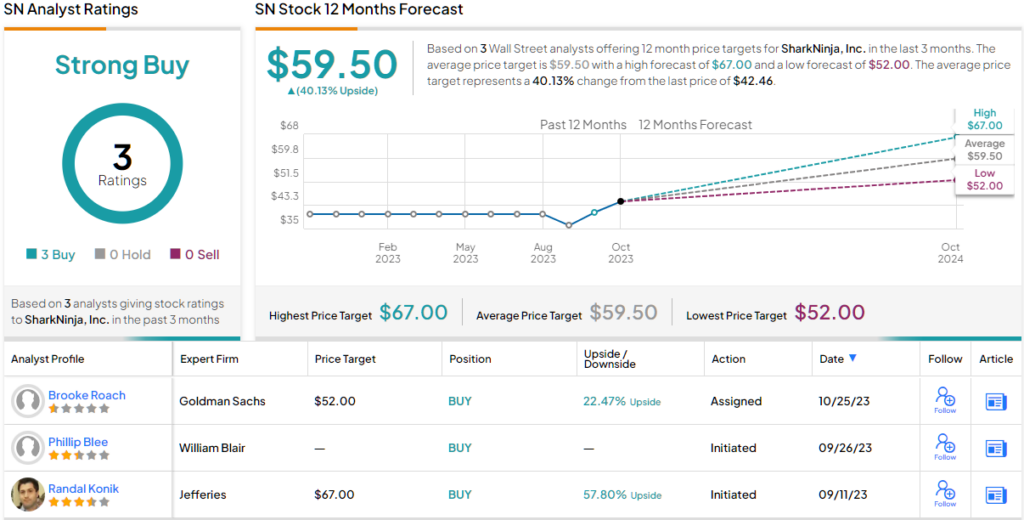

To this end, Roach gives SN shares a Buy rating and $52 price target, suggesting a one-year gain of ~22%. (Watch Roach’s track record)

Overall, there are 3 recent analyst reviews for this recently public stock, and all four are unanimously positive – giving SN its Strong Buy consensus rating. The shares are selling for $42.46, and their $59.50 average price target implies an upside potential of 40% on the one-year horizon. (See SharkNinja stock forecast)

Kontoor Brands (KTB)

The last Goldman pick we’re looking at is Kontoor Brands, a soft goods manufacturer and distributor – and the owner of two of the world’s best-known brands in denimwear, Lee and Wrangler. Kontoor, from its North Carolinian base, is dedicated to producing and marketing superior products that ‘look good and feel right.’

Kontoor’s focus on quality clothing hasn’t held the company back from being a good ‘global citizen,’ however. The company has had a long-term goal of reducing freshwater consumption and waste – an important issue in the garment industry, which uses a great deal of water in preparing and dyeing fabrics. Since 2008, that goal has been set at saving 10 million liters of freshwater by 2025. Earlier this month, Kontoor announced it had met that goal two years ahead of schedule.

While Kontoor worked hard to save water, it has also worked to make returns to its investors. The company pays out a quarterly common share dividend, and in its last declaration, on October 27, the company announced a 4% increase in the payment, from 48 cents per share to 50 cents. The new dividend annualizes to $2 per common share and gives a forward yield of 4.3%.

The dividend was supported by Kontoor’s sound financial results. For the second quarter of this year, the company reported $616 million in revenue – flat year-over-year but nearly $8.5 million ahead of the forecast. At the bottom line, Kontoor’s non-GAAP earnings per share of 77 cents were 14 cents better than had been anticipated, and fully covered the increased dividend payment.

We’ll check in again with Goldman Sach’s Brooke Roach, who outlines a multi-faceted positive outlook for Kontoor. She’s impressed by the company’s ability to deliver for investors in multiple ways, and writes, “Our constructive thesis is driven by KTB’s: (1) strong brand momentum, which is manifesting in market share gains; (2) opportunity for better sell-in trends to key wholesale partners, following a year of destocking in the channel; (3) significant margin tailwinds in 2H23E and 2024E, including raw material cost recapture and cycling prior year manufacturing fixed cost deleverage; (4) strategic investments in brand diversification and DTC distribution that are beginning to scale; and (5) an attractive dividend.”

Roach’s Buy rating on KTB comes along with a $56 price target that points toward a 23% upside potential over the course of the next year.

All in all, the Strong Buy analyst consensus rating on Kontoor shares come from 4 recent analyst reviews – 3 Buys and 1 Hold. The stock is selling for $45.46 and has a $57 average price target; that combination suggests a 25% gain in the next 12 months. (See KTB stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.