As the final quarter of 2023 gets fully underway, analysts and investors alike are trying to divine just what is likely to happen in the next few months. There’s a growing feeling that, with September behind us, stock investors can look forward to better times – perhaps sooner rather than later.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

In some recent comments to CNBC, Scott Chronert, Citi U.S. equity strategist, gives several reasons why investors should load up on stocks now. First, Chronert points out that fears of a hard recession have faded, or as he puts it, “We’ve been pricing in a soft landing since the first part of June.” Backing this, Chronert states that the Fed’s rate cycle is near its peak, and that corporate earnings are likely to remain resilient. At his bottom line, Chronert adds, “I think all told the balance is still to the upside into the end of the year, and we’re going to fall back on our ongoing view that the fundamental underpinning for the S&P remains pretty positive at this point.”

Against this backdrop, the equity analysts at Citigroup have picked out two stocks that they feel will make solid portfolio additions should market conditions improve. And they are not alone, according to TipRanks’ database, both are also rated as ‘Strong Buy’s by the analyst consensus. Let’s see why they are drawing plaudits across the board.

Coherus Biosciences (CHRS)

The first stock we’ll look at is Coherus Biosciences, a developer and manufacturer of biosimilar drugs. This drug class fills an important niche in advanced medicines; they are designed to have functions and targets similar to approved biologic reference medications with expired patents. Biosimilars are a lower-cost alternative to biologics and are seen as a way to expand patients’ access to cutting-edge biologic medicines.

Coherus is both a commercial and clinical-stage biopharma firm, with several approved biosimilar drugs on the market and multiple research tracks ongoing, ranging in stage from preclinical development to BLA submissions. The long-term goal of the company’s research program is to expand the range of cost-effective medicines and deliver significant savings to the U.S. healthcare system.

The three approved medications are a good start in that direction. Coherus currently markets Udenyca, a biosimilar to Neulasta (pegfilgrastim), which is used in the stimulation of bone marrow activity and white blood cell production in patients undergoing chemotherapy. The drug, which was approved in 2018, is marketed as a lower-cost option to Neulasta. Coherus followed up Udenyca with two additional approved drugs. Yusimry, a biosimilar to Humira, was approved in 2021, and Cimerli, a biosimilar to Lucentis, was approved in August of last year.

On the biologics license application (BLA) front, Coherus has two recent updates. First, the company has submitted a BLA supplement for Udenyca, and on September 25, announced it had received a complete response letter (CRL) from the FDA. The response was based on inspection findings at a third-party filler and did not identify any issues with the medication or the trial data. The company has committed to working with the FDA to resolve the issues as soon as possible.

In addition, Coherus has submitted two BLAs for its drug candidate toripalimab, a potential treatment for metastatic or recurrent nasopharyngeal carcinoma. Coherus has received feedback from the FDA following site inspections related to clinical studies of the drug. Only one observation was noted, and again, the company is committed to resolving the matter with the FDA.

In his coverage of this stock for Citi, analyst Yigal Nochomovitz notes that shares in CHRS are down – but lays out a case for the company to turn the corner.

“Coherus shares have underperformed over the last two years largely because of declining Udenyca (Neulasta biosimilar) sales. However, we think Coherus is now entering a significant period of re-growth, driven by new biosimilar launches, the pending toripalimab approval/launch, and clinical advancement of the company’s existing I/O assets and those gained in the recent acquisition of Surface Oncology (SURF). We think the strategy of funding I/O development with biosimilar revenues is attractive in a challenging capital formation environment and sets Coherus up well for long-term value creation,” Nochomovitz opined.

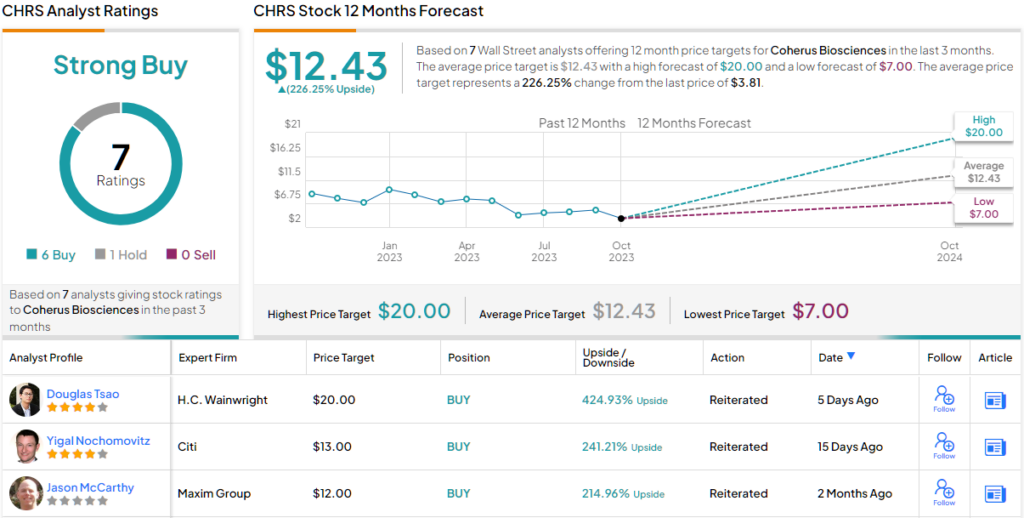

That value creation may be substantial indeed. Nochomovitz rates CHRS shares a Buy, and his $13 price target implies the shares will gain as much as 241% over the next 12 months. (To watch Nochomovitz’s track record, click here)

Overall, the Strong Buy consensus on Coherus is based on 7 recent analyst reviews that include 6 Buy ratings and 1 Hold. The shares are currently trading for $3.81, and their $12.43 average price target suggests a one-year upside of 226%. (See CHRS stock forecast)

Patterson-UTI Energy (PTEN)

From biotech, we’ll shift our focus to oilfield services, a vital niche in the energy sector. Patterson-UTI Energy works with oil and natural gas exploration and production companies, offering the drilling and completion services needed to put hydrocarbon extraction wells into operation. In addition, Patterson-UTI develops directional drilling solutions, as well as specialized drill bits. In short, the company has the unique engineering expertise needed to make the oil patch productive.

Patterson-UTI Energy has its roots in West Texas and is today one of North America’s top-tier oilfield services firms. The company boasts an array of talent, technology, and equipment needed to develop the full potential of oil and gas wells.

The oil and natural gas industry is highly profitable, and Patterson-UTI has successfully leveraged this profitability to transition to a profitable operation over the past year. In the first two quarters of the last year, the company saw its net earnings change from net negative to net positive. In its last reported quarter, 2Q23, the firm had a bottom line of 44 cents per share by non-GAAP measures – a result that exceeded estimates by a penny. The EPS was supported by revenues of $758.9 million, which were up 22% year-over-year, although it fell $23.1 million short of the forecast.

In addition to its sound financial results, Patterson-UTI also pays out a regular dividend. The current payment, at 8 cents per share, annualizes to 32 cents and yields 2.4%. While the yield is modest, it’s worth noting that Patterson-UTI has a history of paying out regular dividends dating back nearly two decades.

This stock caught the eye of Citi’s Scott Gruber, who explains why the company is likely to see improvements in the near future: “The upcoming recovery in U.S. drilling is likely modest by historical standards which we believe is currently weighing on PTEN’s stock. Yet PTEN’s quality operations and deal synergies should still drive outperformance. PTEN offers a top-tier drilling business with a pumping business that appears poised to separate from the pack post-deal. This should facilitate solid margin generation as E&Ps focus on efficiency.”

Gruber goes on to quantify the stock’s upside potential, writing, “Further, management targets $200mm of deal synergies mainly around optimizing within frac. This should help 2024 EBITDA and drive 2025 EBITDA toward $2B, or up ~25% from the 4q23 run rate and double the rig count growth rate. At PTEN’s current stock price, this equates to a sub-3x 2025 EBITDA multiple and ~20% FCF yield. Thus, the stock appears to be discounting a far weaker outcome. This presents a compelling opportunity…”

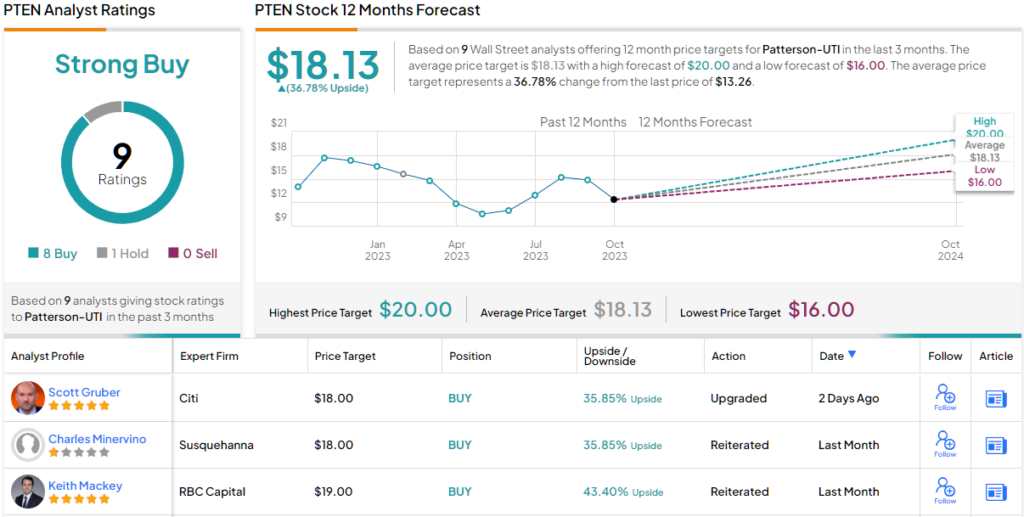

In Gruber’s view, this opportunity worth a Buy rating and an $18 price target, which implies a potential gain of ~36% on the one-year horizon. (To watch Gruber’s track record, click here)

All in all, this oilfield services stock has picked up a Strong Buy consensus rating from the Street’s analysts, based on 9 recent reviews that include 8 Buys and 1 Hold. The shares are priced at $13.23 and have an average price target of $18.13, indicating a potential 12-month upside of ~37%. (See PTEN stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.