In this piece, I evaluated two pharmaceutical stocks, Eli Lilly (NYSE:LLY) and Pfizer (NYSE:PFE), using TipRanks’ comparison tool to determine which is better. A deeper analysis reveals a clear neutral case for Eli Lilly and a bearish case for Pfizer.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Both are juggernauts engaging in the discovery, development, manufacture, marketing, sales, and distribution of pharmaceutical products. Eli Lilly’s top-selling drugs consist primarily of diabetes medications, while Pfizer’s top-selling drugs include the COVID-19 vaccine Comirnaty and the antiviral drug Paxlovid, which treats COVID-19.

Eli Lilly shares have surged 67% year-to-date, including a 34% rally over the last three months, and are up 86% over the last 12 months. However, Pfizer stock has plummeted 37% year-to-date, including a 13% plunge over the last three months, and is off 24% over the last 12 months.

With these two pharmaceutical giants trading in complete opposite directions, it’s interesting that one company’s price-to-earnings (P/E) ratio is roughly one-tenth of the other’s P/E. We’ll compare their P/E ratios to each other and to that of their industry to try to determine what each might be worth.

For comparison, the U.S. pharmaceutical industry is trading at a P/E of 39.2 versus its three-year average of 42.6.

Eli Lilly (NYSE:LLY)

At a P/E of 85.8, Eli Lilly is trading at a steep premium to its industry, but that’s not the only concern with this stock. If it rises much further, the stock will move into overbought territory, suggesting it could be ripe for a correction. However, Eli Lilly’s positive fundamentals and momentum, and its sheer size, suggest a neutral view may be appropriate — pending a more attractive entry point.

First, Eli Lilly’s relative strength index (RSI) stands at 66.2, which is technically neutral. However, with its steady upward momentum, it seems likely to enter overbought territory, which would mean an RSI of over 70. If Eli Lilly does enter overbought territory, it could become ripe for a correction, but even if not, it’s hard to justify paying such a high valuation for this company — no matter how successful it is. At some point, its valuation will matter, even if it doesn’t right now.

On the other hand, it’s easy to see why investors are so excited about Eli Lilly. While Pfizer has been relying heavily on COVID-19 for its drug sales, Eli Lilly is more dependent on diabetes, a market estimated to be worth $61.9 billion last year and projected to reach $118 billion by 2032, a compound annual growth rate of nearly 7%.

Three of the company’s top-selling drugs in 2022 were diabetes medications, and three of the top four are seeing rapidly growing sales. Thus, the best advice for Eli Lilly right now seems to simply wait for a more attractive entry point.

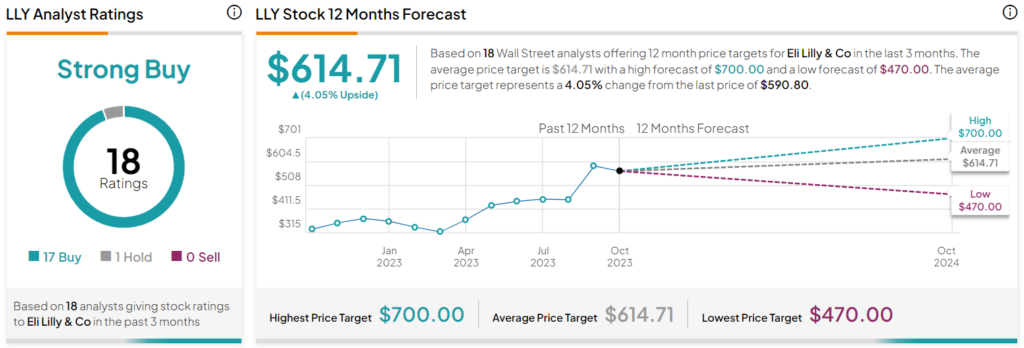

What is the Price Target for LLY Stock?

Eli Lilly has a Strong Buy consensus rating based on 17 Buys, one Hold, and zero Sell ratings assigned over the last three months. At $614.71, the average Eli Lilly stock price target implies upside potential of 4.1%.

Pfizer (NYSE:PFE)

At P/E of 8.4, Pfizer is significantly undervalued relative to its industry and Eli Lilly. Additionally, its RSI of 34.2 means it is falling dangerously close to oversold territory (an RSI of less than 30). However, the company’s looming patent cliff suggests there may not be any upside in the near term. Thus, a bearish view seems appropriate for now, except possibly for fixed-income investors purely seeking dividend stocks.

As arguably the largest pandemic beneficiary from a healthcare standpoint, Pfizer has much to lose when its COVID-19-related patents lose exclusivity in the coming years. In 2022, the company raked in over $56 billion in sales from the vaccine it developed with BioNTech (NASDAQ:BNTX) and its antiviral drug Paxlovid.

Pfizer projected that its COVID-related revenue would plunge to $21.5 billion in 2023, although some analysts have warned that this total may still be too optimistic. In fact, the company sliced $9 billion off its 2023 revenue estimate just days ago in connection with its falling COVID-related sales. Pfizer’s plunging sales are already evident, as its revenue tumbled from $100.3 billion in 2022 to $77.9 billion over the last 12 months.

If there were one reason to hold Pfizer, it would be because of its dividend. Due to its plummeting stock price, the company’s dividend yield has soared to 5.2%. Pfizer also has a long history of paying dividends, with this year marking the 14th straight year of dividend increases.

What is the Price Target for PFE Stock?

Pfizer has a Moderate Buy consensus rating based on five Buys, nine Holds, and zero Sell ratings assigned over the last three months. At $39.54, the average Pfizer stock price target implies upside potential of 26.8%.

Conclusion: Neutral on LLY, Bearish on PFE

Of course, neither Eli Lilly nor Pfizer will be going anywhere anytime soon. Normally, I would say that Pfizer is too cheap to pass up at its current P/E. However, it’s hard to see any near-term upside in this stock until it moves beyond COVID-19 as its top disease market and latches onto more stable, revenue-generating drugs. While Pfizer could be a solid dividend play, investors shouldn’t expect any stock-price gains.

On the other hand, the neutral call on Eli Lilly is merely based on its valuation and RSI rather than anything negative about the company itself. In fact, it looks like nothing but blue skies for Eli Lilly ahead, so it makes sense to wait for a more attractive entry price for its stock.