Elon Musk touched upon many themes on Tesla’s recent earnings call, one of which was the lack of lithium refining options. Given lithium is an essential component in EV batteries, there is an unmet need for refined lithium in the EV industry.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

During the call, Musk said: “Can other people please do this work? That would be great. We’re begging you. We don’t want to do it. Can someone please? Instead of making a picture-sharing app, try lithium mining and refining, heavy industry, come on.”

In short, Musk was trying to draw attention to the opportunity at play for lithium producers.

Covering this industry for Deutsche Bank, analyst Corinne Blanchard agrees and has an idea about which companies could also represent an opportunity for investors.

“Our fundamental view of Lithium has not changed in the medium to long-term, as we believe Supply will remain short of Demand. We anticipate market tightness over the coming years, followed by a growing deficit thereafter,” Blanchard wrote. “We have a preference for the most established Lithium producers, as we believe they can offer better execution with a lower risk profile, and they are well positioned for growing volumes in key jurisdictions.”

Against this backdrop, we’ve opened the TipRanks database and pulled up the details on two of Blanchard’s recommendations. Both are Buy-rated stocks, with double-digit upside potential for the coming year. Let’s take a closer look.

Lithium Americas (LAC)

We’ll start with Lithium Americas, a lithium mining and refining company with big growth potential ahead. While still a pre-revenue concern, LAC fully owns the Thacker Pass Mine, which is situated in northern Nevada, and is its crowning asset given that it boasts the greatest lithium reserves in the US. That makes the mine a valuable resource for the nation’s developing EV industry, which needs first-rate Li-ion batteries. Furthermore, LAC also holds complete ownership and joint venture deals for high purity lithium mines in Argentina.

Although Thacker Pass is an exciting project, production is still a while away and slated for 2026. The company announced the start of construction activities in early March.

However, on the recent Q4 earnings call, the company announced that construction at the Argentine Cauchari-Olaroz mine was “substantially complete,” with production expected to kick off before the conclusion of the first half of 2023. To achieve production and positive cash flow, the company said it requires less than $50 million in extra capital costs. LAC anticipates reaching the full production rate of 40,000 tpa (tonnes per annum) of lithium carbonate by the first quarter of next year.

Assessing the company’s prospects, it is the long-term potential of the Thacker Pass Mine that is core to Blanchard’s positive thesis.

“We remain Buy rated on LAC,” said the Deutsche Bank analyst, “given its asset portfolio and strategic geographic exposure to Argentina and the US… We are positive on management’s ability to develop the Thacker Pass, although we recognize the inherent challenges to the asset being a clay-based deposit. That being said, Thacker Pass is a ~80ktpa hydroxide project, in the US, which should be highly valuable to the US domestic Lithium market.”

That Buy rating is supported by a $26 price target, and should it be met, will represent one-year share appreciation of 36%. (To view Blanchard’s track record, click here)

Blanchard is not alone in her positive take for this prospective lithium producer. LAC has garnered 5 analyst reviews over the past 3 months, and all are positive, naturally making the consensus view here a Strong Buy. In the year ahead, the analysts see the stock surging 73.5%, considering the average target stands at $32.85. (See LAC stock forecast)

Sociedad Quimica Y Minera de Chile (SQM)

We’ll now shift to Chile, a country in possession of the world’s largest lithium reserves and the second-biggest producer on earth. As such, Sociedad Quimica Y Minera de Chile is one of the world’s largest producers of lithium, iodine, and potassium nitrate. The company produces lithium hydroxide and lithium carbonate from brine in Chile’s vastest salt flat, the Salar de Atacama.

The positive price environment seen during 2022 helped the company deliver robust results in its most recently reported quarter – for 4Q22. Revenue climbed by 189.8% from the same period a year ago to $3.13 billion, while beating the consensus estimate by $110 million. Gross profit hit $1.64 billion, way above the $542.8 million generated in 4Q21. That helped the company deliver EPADR (Earnings per American Depositary Receipt) of $4.03, a big increase on the $1.13 delivered in the year ago quarter and well ahead of the $3.77 forecast.

However, more recently, on last Friday, the shares took a big beating, crashing by 18.5% after Chilean President Gabriel Boric unveiled plans to nationalize the country’s lithium industry and establish a state-owned company that will be involved in lithium exploration.

Before their contracts run out, the state-controlled Codelco is expected to negotiate an agreement with SQM (and peer Albemarle) to purchase an interest in their operations.

With SQM’s contract to extract lithium in Chile’s Atacama salt flat coming to an end in 2030, Deutsche Bank’s Blanchard notes that despite believing there won’t be any major changes to current contracts, given the ongoing renewal process, SQM could be affected.

Still, whether the Chilean government’s plan actually takes place remains to be seen, and in the meantime, Blanchard highlights SQM’s value proposition and opportunity for investors.

“As we are increasingly positive on the fundamentals of the market in the medium-term, we value SQM’s upcoming volume expansion, with a focus in Chile on existing operations, but also the upcoming 20kt of hydroxide capacity in China and Mt Holland in Australia,” the analyst wrote. “We like SQM’s shareholder returns with a ~12% dividend yield expected this year, based on our numbers.”

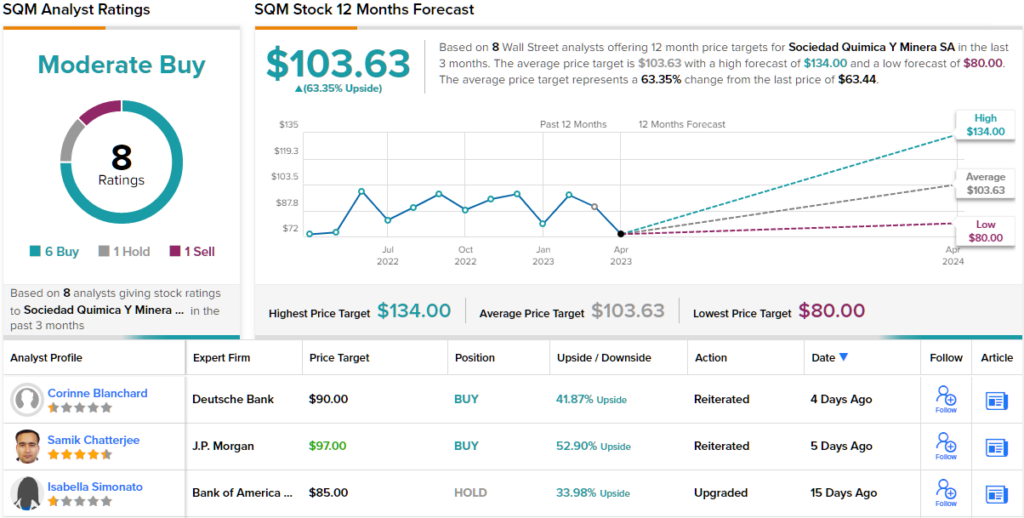

All told, despite the Chilean government’s actions, there’s no change to Blanchard’s Buy rating on SQM or to the price target, which remains at $90 and is set to generate returns of ~42% over the coming months

Looking at the consensus breakdown, with a total of 6 Buys vs. 1 Hold and Sell, each, the analyst consensus rates this stock a Moderate Buy. At $103.63, the average target is more bullish than Blanchard allows and could see investors pocket gains of 63% a year from now. (See SQM stock forecast)

To find good ideas for lithium stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.