Throughout my research over the years, I have stumbled across two companies whose capital allocation strategies have resulted in them becoming powerful stock buyback machines. O’Reilly Automotive (NASDAQ: ORLY) and AutoZone (NYSE: AZO) feature some of the most impressive and prolonged stock repurchase track records I have encountered when analyzing equities.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

However, their capital allocation strategies may not be ideal, with their valuations at somewhat elevated levels. Accordingly, I am neutral on both names.

Why ORLY and AZO Buy Back Shares

ORLY & AZO have made stock repurchases a fundamental part of their capital allocation strategies. This is due to their business models, which require modest capital expenditures and generate high amounts of free cash flow.

Both companies basically operate retail locations through which they sell automotive aftermarket parts, tools, supplies, relevant equipment, and accessories. As the companies grow the number of locations they run, they unlock operating efficiencies and expand their profit margins.

As comparable sales expand over a growing number of locations, SG&A expenses as a percentage of ORLY’s & AZO’s revenues decline, resulting in juicier margins. For instance, ORLY’s operating profit margin has gradually expanded from 15.8% to roughly 21% over the past decade.

The two companies will allocate some capital each year to open new locations, but other than that, the business model does not require additional spending, long-term investments, or any R&D, generating plenty of free cash flow.

This, combined with the favorable cash-flow dynamics of being a retailer and the tax advantage over distributing dividends, has resulted in both companies repurchasing shares in bulk.

How Significant are ORLY’s & AZO’s Buybacks?

To understand how influential ORLY’s & AZO’s stock repurchases have been to shareholder value creation, all you have to do is check the two companies’ share counts. Since 2011, ORLY has reduced its share count by 55.3%. That is more than half the company’s shares in just over a decade. Does that sound impressive? Wait until you hear that AZO has repurchased a staggering 87.5% of its outstanding shares since 1998.

Sure, that’s over 24 years, but that’s the majority of the company’s shares that ever existed. To illustrate the impact of such an aggressive stock repurchase policy, even if AZO’s net income was the same today as it was in 1998, the company’s earnings per share would still be more than eight times higher compared to back then, just from the company’s buybacks alone.

In reality, combined with the company’s underlying net income growth amid a growing number of locations and comparable sales per store, AZO’s earnings-per-share is currently 80 times higher than what it was in 1998! This is somewhat arbitrary, but it once again highlights how ORLY’s & AZO’s business models combined with stock buybacks can result in massive shareholder value creation.

What is the Big Risk Linked to This Strategy?

The biggest risk associated with ORLY’s & AZO’s aggressive stock buyback strategies is overpaying for their own shares. If a company overpays for its own shares, it can even destroy shareholder value. Because the two companies don’t really have many other options when it comes to allocating their free cash flow somewhere, buybacks appear to be the only avenue.

You could argue that if their shares get expensive, they could switch to dividends. However, after featuring such prolonged and committed share repurchase track records, there is a good chance the majority of their shareholder bases have been consolidated by investors who praise this strategy. A change here could be unwelcome, even if it would be to the benefit of shareholders.

Over the past 20 years, ORLY and AZO have had their forward P/Es mostly hover between 13-20x and 10-18x, respectively. The two stocks are currently trading at a forward P/E of 21.3x and 17.8x, respectively. That’s above or on the high end of their historical averages.

Combined with the fact that aftermarket parts likely won’t experience the same sales growth they did over the past two decades moving forward, investors should not expect the same pace of shareholder value creation the two companies delivered prior.

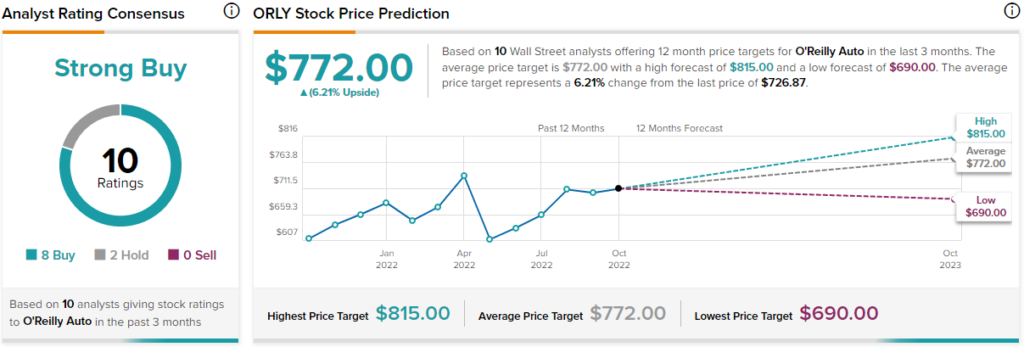

What is the Target Price for ORLY Stock?

As far as Wall Street’s sentiment goes, O’Reilly Automotive has a Strong Buy consensus rating based on eight Buys and two Holds assigned in the past three months. At $772, the average O’Reilly Automotive stock forecast implies 6.2% upside potential.

What is the Target Price for AZO Stock?

In the case of AutoZone, the stock has also attracted a Strong Buy consensus rating based on nine Buys and one Hold assigned in the past three months. At $2,399.60, the average AutoZone stock forecast implies 6.65% upside potential.

Conclusion: Watch Out for Their Valuations

Due to their distinct capital allocation strategies, ORLY’s & AZO’s shareholder value creation prospects are entirely dependent on the underlying valuation of their shares. Thus, you should exercise caution due to their elevated, in my view, valuation multiples.

That’s not to say that the two companies may not end up being fruitful investments over the long term, but that one should not expect the past explosive returns the two companies delivered in prior years.

At 15x earnings or below, ceteris paribus, I would consider being a buyer of both names, nonetheless.