There’s no one investing style guaranteed to generate big returns but for those looking to make headway in the markets, it’s worth checking out the systems used by the best in the business – the ones whose investing endeavors have pocketed billions in the process.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

For example, Steve Cohen, the founder of point72 Asset Management, has favored a high-risk, high-reward style, an aggressive mode of investment that has obviously worked wonders, given he has a net worth of $19.8 billion.

On the other hand, Fisher Investments founder Ken Fisher has built his $7.1 billion fortune on being able to identify data that is not commonly known or interpret well-known information in a unique and accurate manner compared to other participants in the market.

While their paths to success might be different, both strategies have seen the pair reach the same conclusion at times and there are specific equities that take up space in both market sages’ portfolios.

That is bound to pique investor’ interest, and with that in mind, we decided to check out 2 stocks held by both and see why they are such fans. We ran these tickers through TipRanks’ database and found that both are rated as ‘Strong Buys’ by the analyst consensus. Let’s see what makes them so.

American Tower (AMT)

First up, a big name in the real estate investment trust (REIT) sector. American Tower is one of the largest global operators of wireless and broadcast communication infrastructure. The company is a key player in the telecommunications industry and owns and manages a vast portfolio of cell towers, rooftop sites, and other communication infrastructure assets, providing essential support to wireless carriers and broadcasters. Its extensive network spans across the United States and numerous international markets, making American Tower a crucial part of the modern telecommunications ecosystem.

American Tower’s business model revolves around leasing its infrastructure assets to a diverse range of tenants, including major wireless carriers like AT&T, Verizon, and T-Mobile, as well as radio and television broadcasters.

This strategy has allowed the company to generate steady and recurring revenue streams. In Q2, these streams reached $2.77 billion, amounting to a 3.7% year-over-year increase, surpassing the Street’s call by $50 million. Similarly, Q2 AFFO (adjusted funds from operations) of $2.46 also exceeded analyst expectations by $0.04.

Both Cohen and Fisher are heavily invested here. During Q2, Cohen nearly doubled his stake; he now owns 850,703 shares, worth ~$136 million at the current share price. Fisher’s holdings are even larger, totaling 1,219,731 shares, representing a market value of approximately $195 million.

They are not the only ones showing confidence. Goldman Sachs analyst Brett Feldman points out how this name stands out from the crowd.

“The structure of AMT’s comprehensive agreements has enabled the company to maintain both its 2023 outlook for ~5% domestic organic growth and its longer term domestic organic growth outlook (averaging >=5% in 2023E – 2027E). This stands in contrast to CCI, which recently lowered its 2023 outlook for tower core leasing activity with its 2Q23 results. We remain constructive on AMT, as we expect that it will have the highest domestic organic growth rate of any US tower operator over the next five years (5.6% vs. ~4% for peers), which should drive peer-leading AFFO/share growth (~7.5% CAGR vs. 3% to 6% for peers),” Feldman opined.

These comments underpin Feldman’s Buy rating while his $232 price target implies shares will gain 45% over the one-year timeframe. (To watch Feldman’s track record, click here)

Elsewhere on the Street, the stock claims an additional 8 Buys and 2 Holds, all coalescing to a Strong Buy consensus rating. Moreover, the $228.20 average target suggests shares will be changing hands for ~43% premium a year from now. As an added bonus, AMT pays a forward annual dividend yield of 4%. (See AMT stock forecast)

Las Vegas Sands (LVS)

We’ll now shift to the world of hospitality and entertainment, and take a look at Las Vegas Sands, a company famous for its opulent resorts and casinos. The brainchild of the late billionaire Sheldon Adelson, LVS was instrumental in transforming the Las Vegas Strip into a center of opulence and luxury. Although they sold their Las Vegas properties in 2021, they have expanded their presence worldwide, with properties in Macau (including The Venetian Macao, Sands Macao, and The Londoner Macao) and Singapore (Marina Bay Sands).

Ken Fisher has been heavily invested here for a while and currently owns 9,567,353 shares worth ~$427 million. As for Steve Cohen, he made a recent big addition, more than doubling his holdings in Q2, which now stand at 2,425,516 shares, currently worth ~$108 million.

LVS shares, though, are down for the year, having retreated by 30% since the May peak. The bulk of the pullback took place following the company’s July Q2 results.

At first, that might look strange as LVS posted beats both on the top and bottom line. Revenue soared by 142% compared to the same period a year ago, reaching $2.54 billion and surpassing analyst expectations by $160 million. Additionally, adj. EPS stood at $0.46, exceeding the consensus estimate by $0.03.

Investors, however, were disappointed by the 6.7 million visitors in Macau during the quarter, a figure representing about 68% of the 9.9 million visitors recorded in the second quarter of 2019, which serves as the last comparable period before the Covid-19 pandemic started affecting operations.

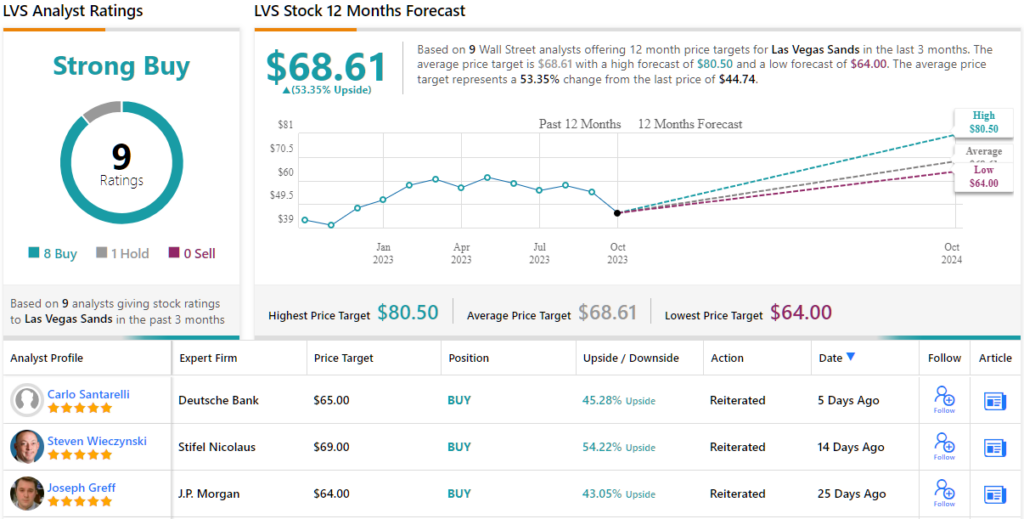

However, Deutsche Bank analyst Carlo Santarelli argues that investors shouldn’t be worried here and advises to stay focused on the long-term opportunity at play.

“We see considerable value in LVS shares at current levels and we believe some of the concern around the trajectory of the recovery in Macau is misguided, with too much being read into short term and somewhat inconsequential datapoints,” the 5-star analyst said. “We see this rationalizing over time and believe LVS, from both a fundamental and valuation perspective, represents a compelling long idea moving forward.”

Quantifying his bullish stance, Santarelli rates LVS shares a Buy, backed by a $65 price target. This suggests the stock will climb 45% higher in the year ahead. (To watch Santarelli’s track record, click here)

Almost all of Santarelli’s colleagues agree. Barring one fencesitter, all 8 other recent reviews are positive, making the consensus view here a Strong Buy. At $68.61, the average target is more bullish than Santarelli will permit and makes room for one-year gains of 53%. (See LVS stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.