Micron (NASDAQ:MU) shares are pushing higher in Thursday’s trading, but that’s hardly a rare occurrence these days. Investors have been rewarding the memory giant for a while now, with the stock up by 177% since April’s lows.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Micron is riding a wave of AI-driven demand for its products, the rally boosted by record earnings, a recent estimate-crushing guide, and plenty of support on the Street, making the company one of the winners of the AI boom. And it looks like demand is not about to slow down anytime soon.

Citi analyst Christopher Danely believes that the next major development in the AI supply chain will be excellent news for one of Micron’s core offerings. “We believe DRAM will be the next type of chip to secure long-term contracts with the AI food chain given its importance and projected undersupply, similar to what happened with NVDA, AMD and AVGO,” Danely said.

And that should help extend the current DRAM upcycle. Danely believes this trend is being driven by AI companies seeking to lock in DRAM supply amid surging demand across the AI sector, and Micron is set to benefit via “higher and sustainable DRAM pricing.”

That, in turn, will help push gross margins back to previous peaks and help EPS peak above $23.00. Accordingly, Danely has made some changes to his MU model.

The analyst expects gross margins to rise from 44.7% in F4Q25 to 60.0% in F3Q26E, approaching the previous peak of 60.8% during the 2018 DRAM upturn. Recall, in the current cycle, Micron’s gross margins hit a low of -14.4% in 2023.

Danely also forecasts peak EPS will reach $23.02 in calendar year 2026, nearly double the prior peak of $12.26 in 2018. Reflecting this outlook, the analyst has raised his estimates: F2026 sales and EPS are now expected to land at $62.5 billion and $21.05, up from $56.0 billion and $16.93; driven by the prospect of long-term contracts, F2027 sales and EPS are bumped to $65.0 billion and $20.31, up from $52.5 billion and $15.93; lastly, F2028 sales and EPS are lifted to $65.0 billion and $19.71, up from $52.5 billion and $15.93.

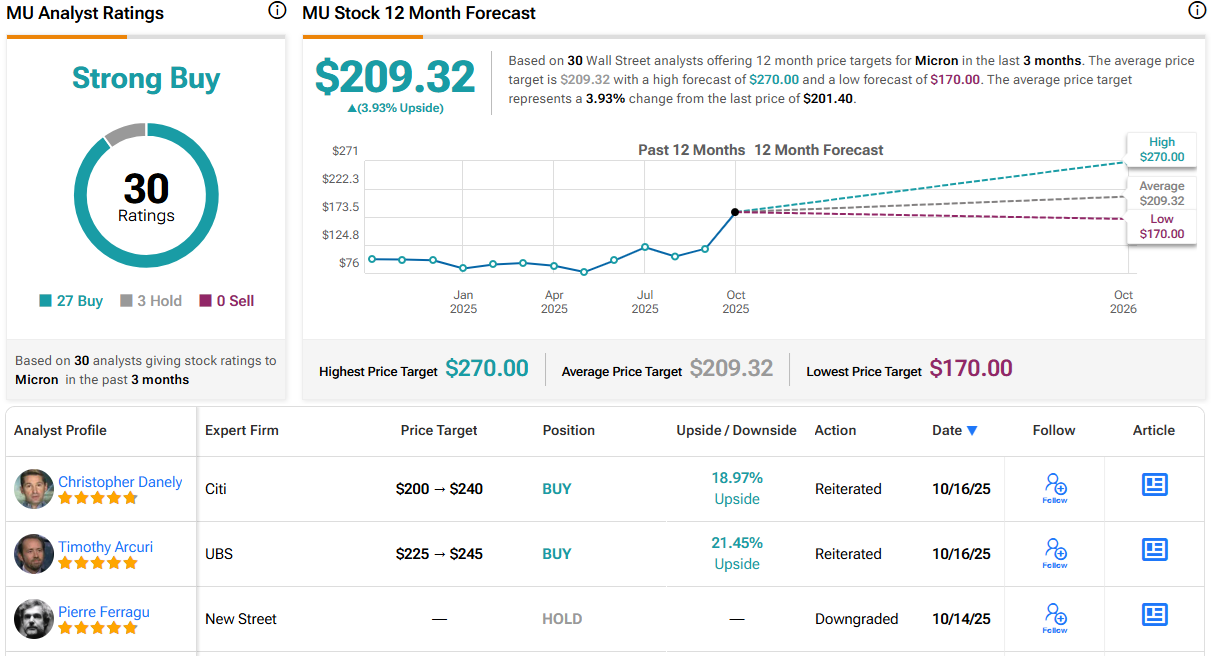

All of that merits a new price target; Danely’s objective goes from $200 to $240, suggesting the stock will gain 19% over the one-year timeframe. Danely’s rating stays a Buy. (To watch Danely’s track record, click here)

Elsewhere on the Street, the stock claims an additional 26 Buys and 3 Holds, all coalescing to a Strong Buy consensus rating. Considering the big gains, the $209.32 average target factors in modest 12-month returns of 4%. (See Micron stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.