It’s that time of year again and Wall Street’s quarterly earnings extravaganza is about to kick off. As is customary, the banks will step up first to deliver Q1’s financials and Goldman Sachs (GS) will be amongst the first batch to report.

The banking giant will release its statement next Tuesday (April 18) against a backdrop of an industry rocked by multiple collapses, not that Goldman is in danger of joining that club. In fact, with a history spanning over 150 years, Singapore banking giant DBS calls this “oldie but goodie” a “world-class broker with top talent.”

“Goldman has consistently occupied the top spots of investment banking league tables and meaningfully expanded the wallet share of its top trading clients, thanks to its excellent culture and ability to attract top talent via a performance-driven compensation system,” DBS analyst Ken Shih went on to explain. “Going forward, the company would trim its principal investment balance sheet while (1) refocusing on its core banking and markets business, (2) growing its asset and wealth management fees, and (3) scaling its young platform solutions business with the aim of achieving profitability.”

Leaving aside the short-term outlook, Shih believes that from FY23F forward, the detrimental effects of sluggish market activity and the decline in asset values are anticipated to “bottom out,” supporting a recovery in Goldman’s income from investment banking fees and principal investments. Efficiency should also be improved by management’s strict control over its workforce and non-compensation costs.

Historically, Goldman has also been good to its shareholders, returning capital both via dividends and share repurchases. Amongst its global peer group, Shih notes that both the historical and projected ROE (return on equity) are above average and during the last five years, the modified payout ratio has averaged over 41%. “Its healthy capital ratios and plans to trim its principal investment balance sheet leave room for a further uplift in shareholder return,” Shih summed up.

Down to business, what does it all mean for investors? Shih rates GS shares a Buy while his $420 price target makes room for 12-month growth of 27%. (To watch Shih’s track record, click here)

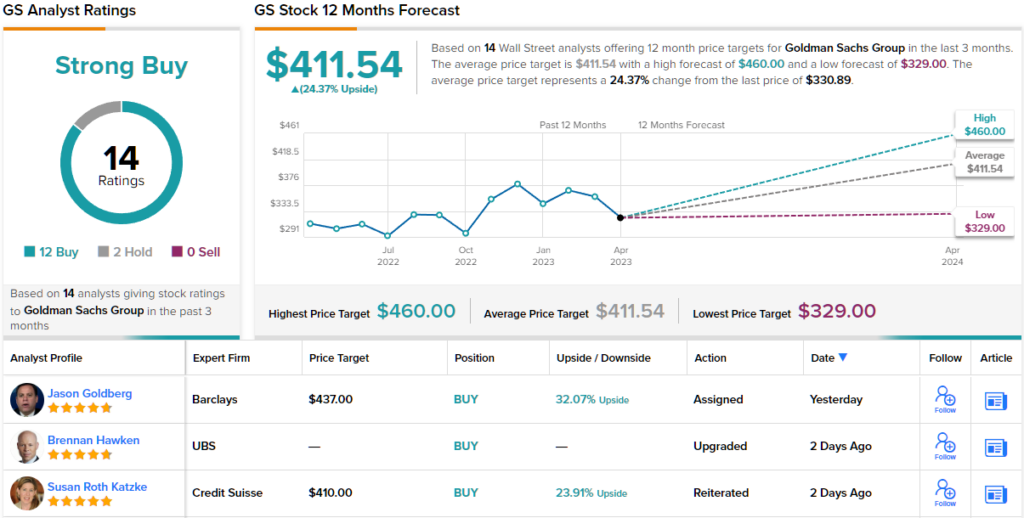

And what about the rest of the Street? Most are on board here, too. The stock claims a Strong Buy consensus rating based on 12 Buys against just 2 Holds. The analysts see shares generating returns of 24% over the one-year timeframe, considering the average target currently stands at $411.54. (See GS stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.