Top U.S. banks, including JPMorgan Chase (NYSE:JPM), Citigroup (NYSE:C), and Wells Fargo (NYSE:WFC), will announce their first quarter financial results on Friday, April 14. While tailwinds from a higher interest rate environment could support the top line, earnings might stay under pressure.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Key Trends to Look Out For

Banks will benefit from the combination of higher average rates and loan balances. However, an expected increase in provision for credit losses (cash set aside by banks to absorb losses on loans) led by macro headwinds, the recent regional banking chaos, and deposit repricing could pressure the bottom line.

Robert W. Baird analyst David George expects a deposit mix shift, an increase in deposit betas, and rising credit losses/costs to remain a drag. However, the analyst expects these large banks to benefit from higher interest rates and increases in loans.

While NIIs (Net Interest Income) are likely to grow, a higher interest rate environment and macro and geopolitical headwinds could continue to hurt mortgage and investment banking fees.

With this backdrop, let’s see what Wall Street thinks of these big banks slated to report Q1 earnings this week.

What is the Future of JPM Stock?

JPMorgan’s revenue and earnings are likely to benefit from higher net interest income. During the Q4 conference call, JPM’s management stated that NII (net interest income) could continue to be driven by higher rates. However, increased competition and the higher deposit rate could adversely impact NII growth.

Analysts expect JPM to report revenues of $36.17 billion in Q1, higher than Q4 revenues of $34.55 billion, driven by higher average rates and loans. Meanwhile, Wall Street expects JPM to post earnings of $3.41 per share in Q1, up from $2.63 in the prior-year quarter. However, EPS could decline slightly on a quarter-over-quarter basis, reflecting increased provisions.

Evercore ISI analyst Glenn Schorr lowered his price target on JPM stock to $146 from $157 ahead of Q1 earnings. The analyst expects continued pressure on investment banking fees and a challenging lending and deposit backdrop to hurt the financials of top banks, including JPM.

JPM stock commands a Strong Buy consensus rating on TipRanks based on 12 Buy and three Hold recommendations. Meanwhile, these analysts’ average price target of $151.80 implies 18.13% upside potential.

Is Citigroup a Good Stock to Buy?

Given the rise in average interest rates, Citigroup’s NII will probably increase. However, continued weakness in non-interest revenues could remain a drag. Its businesses, including wealth and investment banking, have slowed and could remain under pressure in the short term. Meanwhile, an increase in credit costs and higher expenses could pressure margins.

Analysts expect Citigroup to report revenues of $20.06 billion in Q1, higher than Q4 revenues of $18 billion. Also, the consensus estimate compares favorably with the prior year’s quarter. At the same time, analysts expect Citigroup to post earnings of $1.64 in Q1, reflecting a decline on a year-over-year basis. However, earnings are likely to improve on a quarter-over-quarter basis due to productivity savings.

Evercore’s Schorr cut his price target on Citigroup stock to $45 from $53, expecting lower investment banking income and a tough deposit and lending environment.

Overall, Citigroup stock is a Moderate Buy on TipRanks, based on four Buy and six Hold recommendations. Analysts’ average price target of $55.90 implies 19.14% upside potential.

What’s the Prediction for WFC Stock?

The rising interest rate environment will drive NII growth and could offset the weakness in non-interest income. However, an expected increase in WFC’s provisions and lower investment banking fees could remain a drag.

Wall Street expects Wells Fargo to report revenues of $20.09 billion in Q1 compared to revenues of $19.66 billion in Q4 and $17.59 billion in Q1 of the prior year. Meanwhile, analysts expect WFC to post earnings of $1.13 a share, higher than the $0.88 reported in the prior-year period. Also, it compares favorably to the previous quarter’s EPS of $0.67.

George maintains a Buy recommendation on WFC stock. However, he sees NIIs in Q1 as being down by a “few hundred million sequentially driven by lower day count.” Further, he expects deposit outflows to remain a challenge. Nevertheless, the analyst expects the bank to report higher NIIs for the full year and benefit from an increase in loan balances and higher average interest rates.

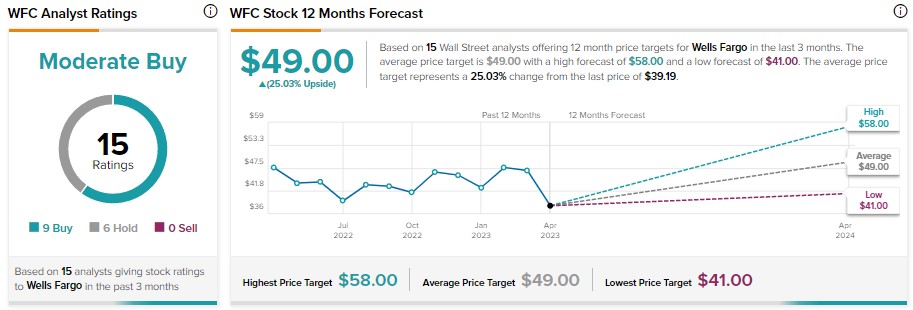

WFC stock has nine Buy and six Hold recommendations, translating into a Moderate Buy consensus rating. Further, the average price target of $49 implies 25.03% upside potential.

The Takeaway

Banks could continue to grow their NIIs due to higher interest rates and the expansion of loan books. However, increased provisions and lower investment banking fees could remain a drag. JPM, with its Strong Buy consensus rating, could outperform Citigroup and Wells Fargo with its quarterly performance.