Johnson & Johnson (NYSE:JNJ) stock’s investment case is highly correlated with its underlying dividend prospects. As a healthcare giant with iconic brands like Band-Aid and Listerine, along with a diverse pharmaceutical and medical device portfolio, Johnson & Johnson has earned the trust of income-focused investors. With 61 consecutive years of dividend increases and another hike imminent, let’s explore what is worth considering in the interim and why I am neutral on JNJ stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Johnson & Johnson’s Dividend is Utterly Recession-Proof

The first point that I want to make clear is that Johnson and Johnson’s dividend is utterly recession-proof. That’s a bold claim, I know. In fact, it’s important to address the skepticism that often surrounds the term “recession-proof.” Numerous companies previously deemed recession-proof have cut their dividends, as illustrated by the case of AT&T (NYSE:T).

Despite its surely recession-proof business model, as a provider of essential telecommunication services, the company was forced to cut its dividend in 2022 due to its unsustainable debt burden. This cautionary tale underscores the significance of being prudent and never taking any past trend for granted, especially when it comes to dividend growth.

Nevertheless, and despite my efforts to scrutinize and challenge this claim, it is very hard to question the strength of Johnson & Johnson’s dividend regardless of the underlying economic landscape.

Johnson & Johnson boasts an incredibly diverse portfolio featuring a multitude of cutting-edge MedTech products. From general surgery and orthopedics to pharmaceuticals, vision care solutions, and a wide array of consumer health products, investing in Johnson & Johnson is more like buying a healthcare and consumer staples ETF rather than a single company.

The company’s healthcare products are critical for doctors to treat their patients. Simultaneously, the company’s consumer staple products, like Band-Aid and Listerine, benefit from highly consistent sales due to their household staple nature. Therefore, Johnson & Johnson’s cash flow profile tends to be extremely robust, ensuring its dividend remains well covered at all times.

To support this argument with data, no three-year period in Johnson & Johnson’s history has featured no revenue growth. The company has also continuously grown its adjusted earnings per share, maintaining a healthy payout ratio despite increasing the dividend year after year for more than six decades. Fiscal 2023 was no different, with Johnson & Johnson reporting adjusted earnings per share growth of 11.1% to $9.92, implying a payout ratio of just under 48% based on the $4.76 annualized dividend per share.

Finally, it’s worth mentioning that Johnson and Johnson is one of the only two publicly-traded companies, along with Microsoft (NASDAQ:MSFT), that have been granted a AAA credit rating by Standard & Poor’s (as of August). The company is considered more creditworthy than the U.S. Government, whose credit rating has been downgraded to AA+. I believe this speaks volumes in terms of its overall financial soundness and, thus, ability to sufficiently cover its dividend along with other obligations/commitments.

Another Dividend Hike is Coming — What to Consider

With Johnson & Johnson having already declared four $1.19 quarterly dividends, another dividend hike is likely coming. The company has increased its dividend every April or May as far back in time as one can see, so it’s safe to assume that this year will be no different. While a dividend hike usually marks a reason to celebrate, particularly when it comes from seasoned dividend growers that income investors love, I believe that this is not the case with Johnson and Johnson and more.

Specifically, despite the company’s legendary dividend growth history, there is no doubt that dividend growth has undergone a clear deceleration trend, reaching a point of frustration. The company’s 10-year compound annual growth rate seen over various periods paints a clear picture. Johnson & Johnson’s 10-year dividend per share CAGR stood at:

- 14.8% in 2006

- 14.0% in 2008

- 13.4% in 2010

- 12.4% in 2012

- 9.7% in 2014

- 8.8% in 2016

- 7.0% in 2018

- 6.6% in 2021

- 6.4% in 2023

The trend is clear, with gradually smaller increases over time reducing the company’s average dividend growth rate. Last year’s dividend increase of just 5.3% was the weakest of them, pointing toward the fact that this trend won’t be reversing anytime soon.

Given that Johnson & Johnson’s yield is not tremendous, standing at 2.9%, it’s hard to be excited about the company’s dividend prospects in the face of such a continuous deceleration. The deceleration appears rather puzzling, considering the ample coverage provided by earnings. Nevertheless, the sustained nature of this trend suggests a deliberate strategy by management. In my view, this will weigh negatively on JNJ stock investors despite the company’s otherwise unparalleled qualities.

Is JNJ Stock a Buy, According to Analysts?

Regarding Wall Street’s view on the stock, Johnson & Johnson has a Moderate Buy consensus rating based on eight Buys and seven Holds assigned in the past three months. At $177.67, the average JNJ stock forecast implies 11.4% upside potential.

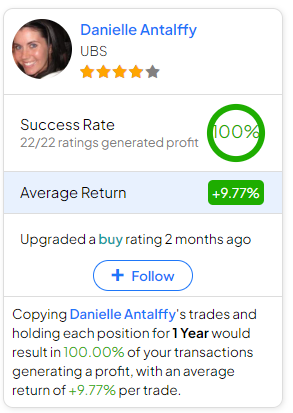

If you’re wondering which analyst you should follow if you want to buy and sell JNJ stock, the most profitable analyst covering the stock (on a one-year timeframe) is Danielle Antalffy of UBS, with an average return of 9.77% per rating and a 100% success rate. Click on the image below to learn more.

The Takeaway

Overall, while Johnson & Johnson’s dividend growth track record displays remarkable resilience and underscores the company’s recession-proof characteristics, the evident deceleration in dividend growth is a cause for concern.

The company’s diverse portfolio and robust cash flow position it as a reliable investment, but the slowing trend in dividend increases may impact investor sentiment. With another dividend hike on the horizon, I believe that investors should expect another below-average growth rate despite the company posting double-digit adjusted EPS growth in its Fiscal 2023 results.