Wednesday is set to be a big day for market watchers, with the Fed expected to announce another interest rate hike, a move that will no doubt impact the stock market’s behavior.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Rate hikes have been de rigueur in 2022 and this will be the fourth instance of such an act. The effort to curb soaring inflation has rocked the markets but heading into the Fed’s decision, Jim Cramer, the well-known host of CNBC’s ‘Mad Money’ program, thinks there could be more turbulence ahead. Or as Cramer puts it, “Welcome to the living hell that is a true Fed tightening cycle.”

The new conditions merit a fresh approach, then, and Cramer says it’s goodbye to growth-oriented tech stocks and time to usher in a new era.

“You have to go to the new leaders of this market. Leaders like health care, leaders like the oils, leaders like the financials that lay off people as a matter of course,” Cramer explained. “You buy the industrials that are levered to travel, you buy consumer packaged-goods stocks that have lots of commodity costs that are now coming down.”

So, with this as backdrop, let’s pull up the details on two Cramer picks that are set to benefit from this new paradigm. It’s not only Cramer that is getting behind these names. According to the TipRanks database, both are rated as Strong Buys by the analyst consensus. Let’s see why.

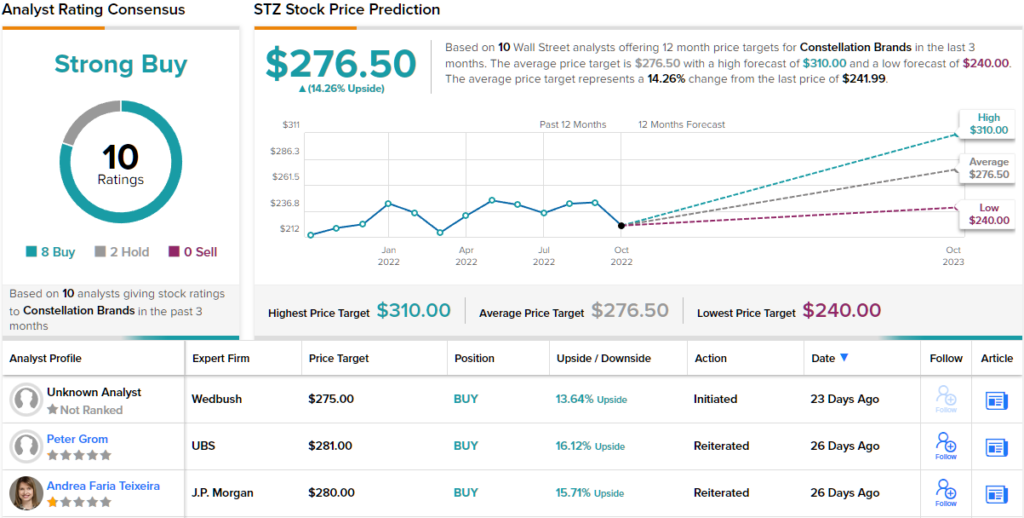

Constellation Brands (STZ)

Recession or not, people will always need a stiff drink to either get the party started or make it through hard times and that’s why alcoholic beverage giant Constellation Brands, the first Cramer pick we’ll look at, could be somewhat immune to the macro whims.

This large-cap company’s portfolio boasts over 100 brands, including Robert Mondavi, Simi Winery, Ruffino (wines), Svedka Vodka, Casa Noble Tequila (spirits), and Corona, Modelo Especial and Negra Modelo on the imported beers front. In fact, sales-wise, Constellation is the U.S.’s largest beer importer, whilst amongst major beer suppliers, it also claims the third-biggest market share (7.4%). Constellation is also invested in cannabis and healthcare.

This kind of value proposition helped the company beat expectations in its latest quarterly statement – for the second quarter of fiscal 2023.

Buoyed by strong demand for its beer portfolio, revenue climbed by 12.2% year-over-year to $2.66 billion, in turn beating the Street’s call by $150 million. There was a beat on the bottom-line too; the company delivered adj. EPS of $3.17 vs. the analysts’ expectation for $2.82.

The company also impressed with the outlook, raising its comparable EPS forecast for FY2023 to the range between $11.20 to $11.60 from the prior $11.20 to $11.50. The consensus estimate stood at just $11.06 per share.

It’s also the kind of performance which has ensured the stock has remained relatively stable compared to the overall 2022 market rout. The shares might be down by 3% on a year-to-date basis but that is a much better display than the S&P 500’s 19% pullback.

Assessing the company’s prospects, Jefferies analyst Kevin Grundy calls Constellation his “favored large-cap growth idea.”

“STZ’s beer segment is clearly sustaining momentum in an environment where the market is naturally concerned about slowing consumer demand,” Grundy opined. “FY23 guide is conservative, and at ~15x EV/EBITDA (ex. Canopy), we see ample scope to close the multiple gap vs high growth peers MNST/BFB trading at ~24x/24x. STZ is uniquely positioned as there are very few businesses in global staples with leading market share, a long runway to grow sales/OI 7-9% p.a., and 43-44% EBITDA margins/30% returns on capital.”

To this end, Grundy rates STZ stock a Buy while his $310 price target suggests shares will climb ~28% higher over the one-year timeframe. (To watch Grundy’s track record, click here)

Looking at the consensus breakdown, other analysts have also been impressed. Based on 8 Buys and just 2 Holds (i.e. Neutral), the word on the Street is that STZ is a Strong Buy. The average target stands at $276.5 and represents 12-month returns of 14% from the current share price of $242. (See STZ stock analysis on TipRanks)

Eli Lilly and Company (LLY)

Let’s pivot from one industry giant to another, albeit in a completely different sector. Eli Lilly, Cramer’s second market leader, is a pharmaceutical titan and boasts a market cap of $334 billion, making it second only to Johnson & Johnson in the global pharma industry. Founded all the way back in 1876, the company’s products are available in 120 countries while it has a total of 37,000 employees spread across the globe.

Such size and reach are based on an illustrious track record. For history buffs take note: in 1923, the company released Iletin, the first insulin medication to be sold commercially, indicated to treat diabetes. Additionally, LLY was the first firm to produce and distribute Jonas Salk’s polio vaccine on a global scale. Amongst its most well-known products now are the antipsychotic drug Zyprexa (1996), the clinical depression treatments Prozac (1986), and Cymbalta (2004), as well as the diabetic medications Trulicity (2014) and Humalog (1996).

The pharma giant just released its Q3 report, posting beats on both the top-and bottom-line. Revenue rose by 2.5% from the same period a year ago to $6.94 billion, while adj. EPS climbed by 12% year-over-year to $1.98. However, the company disappointed with the outlook and 2022 revenue is now expected in the range between $28.5 billion to $29 billion compared to $28.8 billion to $29.3 billion beforehand. Likewise, the adj. EPS guidance was lowered from $7.90-$8.05 to between $7.70 and $7.85. The analysts were expecting $28.76 billion and $7.95, respectively.

Nevertheless, boosted by robust patient demand and broadening insurer coverage, its new diabetes drug Mounjaro saw global sales of $187.3 million, far above the $82 million anticipated by Wall Street.

The drug’s potential remains central to Morgan Stanley’s Terence Flynn’s thesis: “We remain bullish on the outlook for Mounjaro (LLY’s key product cycle) coming out of 3Q given strong demand trends for GLP’s, as well as LLY’s margin expansion opportunity. Our refreshed scenario analysis continues to suggest upside to 2023 Mounjaro+Trulicity estimates and we see LLY’s 2023 guidance call on Dec 13 as the next catalyst for the stock.”

Accordingly, Flynn rates LLY shares an Overweight (i.e. Buy), while his price target is raised from $408 to $441, suggesting the stock will generate returns of ~25% in the year ahead. (To watch Flynn’s track record, click here)

All of Flynn’s colleagues agree this is a name to own; based on a unanimous 11 positive analyst reviews, the stock naturally claims a Strong Buy consensus rating. The shares have significantly outperformed the market this year, rising ~32%. (See LLY stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.