Inflation is high, the Fed is aggressively hiking interest rates, and the markets keep testing their lows for the year. The rest of this week will see several key monthly reports, including the consumer price index, or the inflation report, on Thursday. Currently, inflation is up 8.3% since last year, and economists are expecting that number to decline to 8.1%.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Jim Cramer, the well-known host of CNBC’s ‘Mad Money’ program, is finding a silver lining in the current situation, telling investors, “I always say there’s no give without a get. Right now, the give is that you get your portfolio all going down — the Fed’s bringing the pain. The get is that you’ll eventually be rewarded with lower inflation followed by lower rates. We’re very much in the first phase, though, the give phase.”

But when the Fed does switch away from hiking rates, the ‘get’ may be substantial – and Cramer recommends picking up some relevant stocks now, while markets generally are down, in preparation for a later true rally.

Cramer has made some specific calls on this end, and we’ve used the TipRanks databank to pull up the details on two of them; here they are, presented along with commentary from the Wall Street analysts.

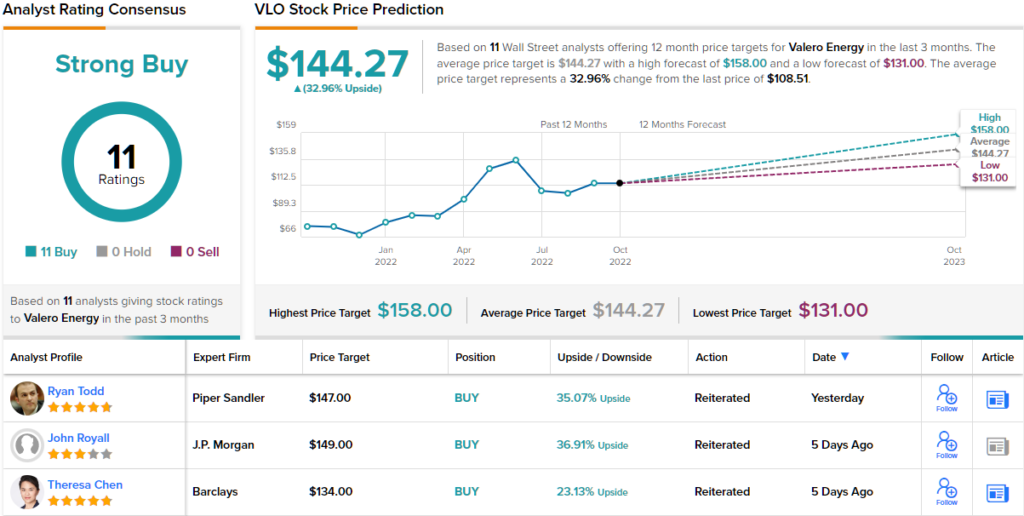

Valero Energy Corporation (VLO)

The first ‘Cramer pick’ we’ll look at is Valero Energy, a major producer and distributor of refined fuels. Valero works in the North American, Caribbean, and UK markets, and operates 15 refiners in the US, Canada, and the UK, along with a 50 megawatt wind farm and 11 ethanol biofuel plants. The company is the second largest producer of both corn ethanol and renewable diesel fuels on the global markets.

Valero ran net earnings losses through 2020, but in 2Q21 the company turned to profitability – and has seen earnings and revenues both rise since then. In the last reported quarter, 2Q22, both the top and bottom lines saw major jumps. Revenues hit $51.6 billion, up 86% from the year-ago quarter, and diluted EPS rose to $11.36, from just 63 cents one year prior. The company had a total adjusted net quarterly income attributable to shareholders of $4.6 billion.

The biggest support for Valero’s strong 2Q22 performance came from the company’s refining segment, which saw revenues increase from just $349 million in 2Q21 to $6.2 billion in 2Q22. Per the end of the second quarter, Valero reported total debt of $10.9 billion and cash on hand of $5.4 billion, compared to $13 billion of debt and $2.3 billion of cash one year earlier.

Valero has maintained its dividend in recent years, and the current payment, 98 cents per common share quarterly, or $3.92 annualized, yields a 3.5%.

Covering this stock for Morgan Stanley, analyst Connor Lynagh sees Valero with a clear path to maintain profits, writing: “On the most important debate right now — demand destruction — VLO’s commentary was upbeat, suggesting limited evidence that product demand is softening in response to high prices. VLO seems well-positioned to navigate continued market choppiness and capitalize on the opportunities potentially opened by Europe’s desire to wean itself off Russian refined products…”

“We continue to like shares here, but acknowledge that leading edge economic data points and evidence of the magnitude and duration of a potential recession will be the key driver of share price performance. For now, shareholders can simply count on VLO management to generate and return substantial sums of cash,” the analyst summed up.

To this end, Lynagh rates VLO an Overweight (i.e. Buy), and his $140 price target shows his confidence in a one-year upside potential of ~29%. (To watch Lynagh’s track record, click here)

So, that’s Morgan Stanley’s view, what does the rest of the Street make of Valero’s prospects? All are on board, as it happens. The stock has a Strong Buy consensus rating, based on a unanimous 11 Buys. Moreover, the $144.27 average target, suggests shares have room for ~33% growth in the year ahead. (See VLO stock forecast on TipRanks)

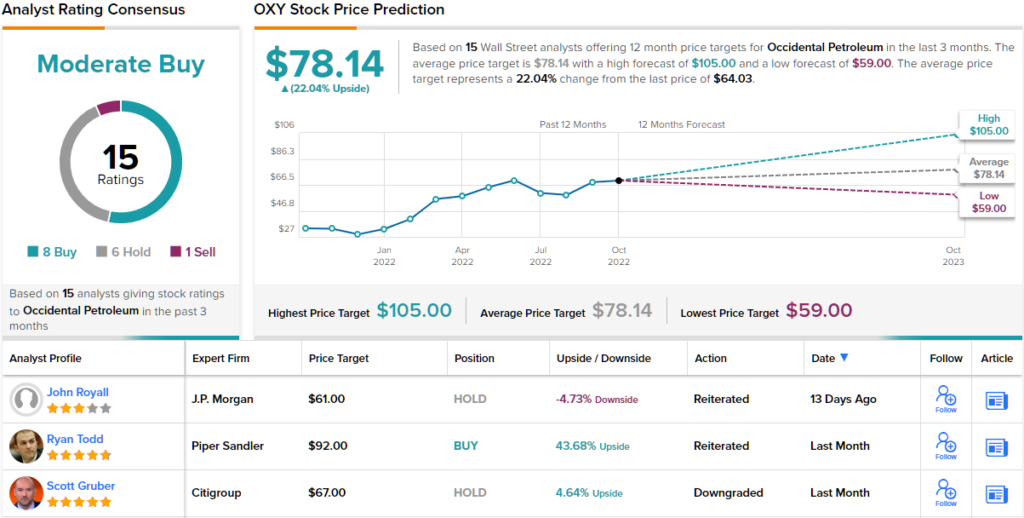

Occidental Petroleum Corporation (OXY)

For the second stock, we’ll stick with the energy industry and look at Occidental Petroleum, one of the largest hydrocarbon exploration and production firms in the business. Occidental has hydrocarbon production ops in the US, North Africa, and the Middle East, and its activities include midstream transport and power generation. In addition to petroleum and petroleum products, Occidental also works in industrial chemicals, producing chlor-alkalis, vinyls, and chlorinated organic chemicals. And on a third important track, the company has a Low Carbon Venture, aimed at transforming the use of CO2 emissions to a sustainable model.

Occidental’s top line revenues in the last reported quarter, 2Q22, hit $10.3 billion, up 68% year-over-year. This solid result led to further sound financials in the drill downs. Cash from operations was listed at $5.3 billion, and free cash flow came in at $4.2 billion. The company repaid some 19% of its total debt in quarter, and was still able to repurchase 18 million shares for $1.1 billion (as of August 1, 2022). The company increases its shareholder return with a modest 13-cent common share dividend, paid out quarterly.

Shares in OXY have dramatically outperformed the overall markets this year. OXY is up 107%, compared to the 25% drop in the S&P 500 and the 20% drop in the Dow Jones. Yet, according to Cramer, OXY “could have some upside here.” The company’s position as a producer of an essential product, and its willingness to monetize the more socially acceptable ‘low carbon’ track, have undergirded its share strength.

Writing from Truist, 5-star analyst Neal Dingmann believes that Occidental can continue to both maintain profits and pay down debt, improving its overall position and its leverage.

“Occidental continues to maximize its diversified portfolio resulting in ~$4B of quarterly FCF, that the company has prudently used to materially pay down debt to $22B recently from nearly $36B just a year ago. The much improved leverage has allowed OXY to increase shareholder returns (base dividend and buybacks)… We forecast the company to continue with their ~20 rig US onshore program that along with the GoM and international operations should result in mid-single digit growth, by our estimates,” Dingmann opined.

Looking ahead from this bullish stance, Dingmann rates OXY shares a Buy, while his $105 price target implies a potential upside of ~64% for the year ahead. (To watch Dingmann’s track record, click here)

Overall, OXY gets a Moderate Buy rating from the analyst consensus, with 8 Buys, 6 Holds, and a single Sell set in the three months. The stock is selling for $63.74, and the average price target, now at $78.14, implies a one-year upside potential of ~22%. (See OXY stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.