Market watchers are waiting for the day the Fed starts cutting rates, but those hoping such an act will signal the beginning of a bull market are in for a rude awakening. At least, that is the opinion of Jeremy Grantham.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Across decades of investing, Grantham’s reputation has been built on predicating market meltdowns, and the legendary investor and GMO co-founder thinks the bear will only be halfway through its wrecking job once the Fed changes it inflation-combating strategy.

“Most of the decline in these great bear markets only happens after the first interest rate cut,” Grantham recently said. “So you tell me when the first interest rate cut is, and I will tell you when the second half of the pain is going to start.”

However, that doesn’t mean that Grantham has lost hope for all stocks. His portfolio still includes big bets on several names and he’s not the only one showing confidence in these equities. Banking giant Goldman Sachs has also been singing the praises of 3 Grantham-owned stocks, believing they are primed to push ahead from here. Let’s take a closer look.

SolarEdge Technologies (SEDG)

We’ll start with SolarEdge Technologies, the biggest supplier of photovoltaic inverters in the world. By creating a device that attaches to the back of the solar panel and increases the amount of power generated, the company essentially became the first to make power optimizers a commercially viable product, helping to reduce the cost of the energy the system creates.

Given Europe is looking to become less dependent on Russian natural gas, the company is well setup up to cater to increasing demand in the region, which now accounts for nearly 60% of its total solar inverter volume.

SolarEdge is showing strong growth, with its revenue soaring by 61.4% year-over-year to $890.7 million in Q4. This impressive increase was largely fueled by the solar segment’s record sales of $837 million. Adj. EPS climbed from $1.10 in the same period a year ago to $2.86. Both the top-and bottom-line displays came in ahead of the forecasts. For Q1, revenue is expected to come in between $915 million and $945 million. The Street was looking for just $914.70 million.

Grantham obviously thinks SolarEdge has what it takes to outfox the bear. In Q4, GMO increased its position by 59% and holds a total of 657,660 SEDG shares. These are currently worth $189.6 million.

Mirroring Grantham’s confidence, Goldman Sachs analyst Brian Lee believes the future is bright for this smart energy leader. He writes: “SEDG’s gross margin recovery story is still only in the middle innings with more drivers of upside yet to fully play out (e.g. freight, Sella 2 manufacturing, IRA credits), while the specter of potential upside and leverage to any further European policy support (e.g. IRA) would make SEDG well-positioned to see further upside in numbers, in our view. At the same time, the Euro could prove to be a tailwind again in the near-term.”

These comments form the basis for Lee’s Buy rating on SEDG, while his $420 price target suggests the shares will climb 46% higher over the coming months. (To watch Lee’s track record, click here)

Elsewhere on Wall Street, the stock garners an additional 14 Buys and 7 Holds for a Moderate Buy consensus rating. Going by the $369.57 average target, investors will pocket returns of 30% a year from now. (See SEDG stock forecast)

Salesforce, Inc. (CRM)

The next name endorsed by Grantham and Goldman is another leader in its field. Salesforce is a software colossus, specializing in customer relationship management (CRM). Its software and apps provide its client base with the means to offer their own clientele a higher level of service.

The offerings focus on sales, analytics, and automation to bespoke customer service, community management, and relationship intelligence, amongst others. The company touts itself as the world’s premier CRM platform for businesses, and with a market cap over $192 billion, that’s no idle boast.

After weathering some tough times like many other mega-tech names, Salesforce’s fiscal fourth quarter (January quarter) results were impressive. Revenue reached $8.38 billion, for a 14.4% year-over-year increase while beating the Street’s forecast by $390 million. Adj. EPS also trumped consensus expectations of $1.36, coming in at $1.68. for FQ1, Salesforce guided for revenue in the range between $8.16 – $8.18 Billion, also above the $8.03 billion expected by the analysts. Moreover, via shares repurchases, the company returned $2.3 billion to shareholders.

That must all be very pleasing to Grantham. GMO’s stake in Salesforce stands at 1,385,522 shares, currently worth $265.3 million.

For Goldman Sachs analyst Kash Rangan, when considering this tech giant’s future, there’s plenty to be upbeat about.

“We reiterate the company’s impressive organic growth rate given the company’s size at +$30bn estimated revenues (GSe) in FY23,” Rangan said. “We remain bullish on the company’s ability to drive continued y/y operating margin expansion beyond FY23. We would point out that companies such as Microsoft, Adobe, Intuit and Autodesk which embarked on a journey towards improving OM all benefited from their valuation multiples getting re-rated significantly higher on an EV/Sales basis. We think CRM could join this list especially as the company grows into a formidable $50 billion business in F26/C25, benefiting from a much lower starting point for OM relative to other companies, which on the flip side also offers plenty of room for improvement.”

How does this translate to investors? Rangan rates CRM shares a Buy, backed by a $320 price target. That figure makes room for 12-month gains of 69%. (To watch Rangan’s track record, click here)

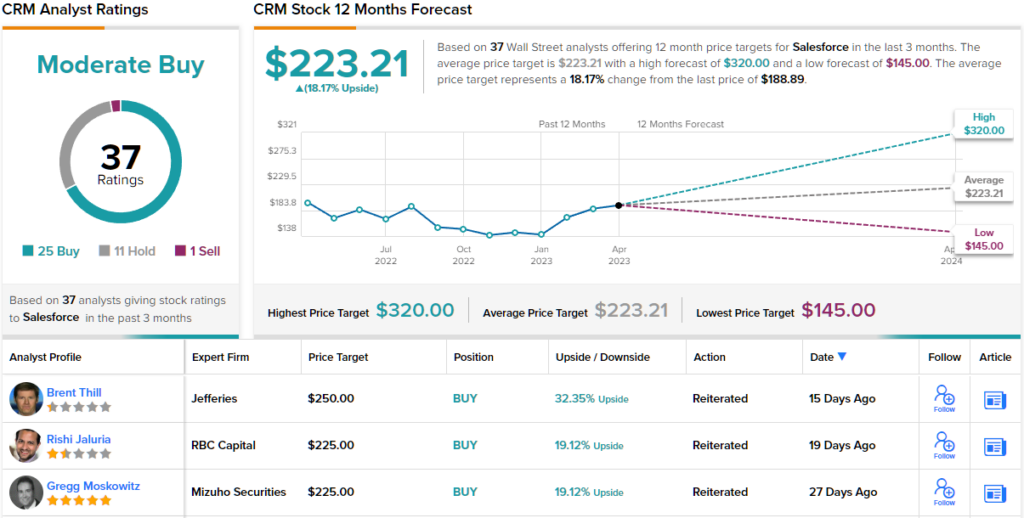

Turning now to the rest of the Street, where CRM has robust support among Rangan’s colleagues. Based on 25 Buy ratings, 11 Holds and just 1 Sell, the stock has a Moderate Buy consensus rating. The average price target stands at $223.21, implying shares will appreciate by 18% over the coming months. (See CRM stock forecast)

Carrier Global (CARR)

Last but not least on our Grantham-Goldman backed list, we have Carrier Global, a company formed way back in 1915 as a specialist in the making and distribution of HVAC (heating, ventilation, and air conditioning) systems.

While Carrier is most famous for its residential and commercial air conditioners, its remit has expanded since its early days and now includes the manufacturing of commercial refrigeration and food service equipment, while the company is also an expert in fire and security technologies.

For the most part, over the past couple of years, Carrier has managed to beat bottom-line expectations, and while it did not manage to do so in the most recent quarterly update, for 4Q22, at $0.40, adj. EPS still met the analysts’ forecast. Likewise at the top-line; the company might have seen revenue drop by 1% year-over-year to $5.1 billion, but that figure edged ahead of the consensus estimate by $30 million. Looking ahead to the full year 2023, the company guided for sales of $22 billion, also improving on Wall Street’s $20.39 billion forecast, while adj. EPS is expected in the range between $2.50 and $2.60 – at the mid-point, the same as consensus at $2.55.

Jeremy Grantham is clearly upbeat about Carrier. His GMO fund currently owns 1,138,546 shares worth $49.55 million.

When assessing Carrier’s prospects, Goldman Sachs analyst Joe Ritchie thinks the company is playing it safe with regards to its outlook. He writes, “Improving price/cost, ongoing cost savings, and continued strength in Commercial HVAC suggest EPS guide is likely conservative, and we remain bullish on the company in the long-term given the self-help opportunity coupled with strong growth tailwinds from education stimulus, healthy building orders, and heat pump demand.”

Putting these words into ratings and numbers, Ritchie says Buy CARR shares while his $53 price target suggests upside of 22% could be in the cards over the coming year. (To watch Ritchie’s track record, click here)

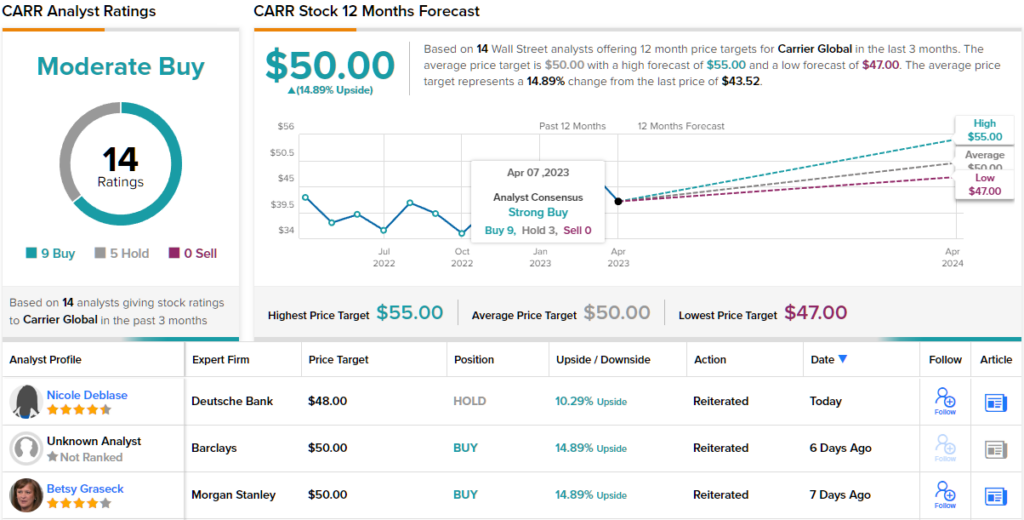

Overall, CARR gets a Moderate Buy rating from the analyst consensus, based on 9 Buys vs. 4 Holds. The forecast calls for one-year returns of ~15%, considering the average target stands at $50. (See CARR stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.