Our love for music is unwavering, but the ways we enjoy it are constantly evolving. The music industry has undergone significant changes with the advent of social media, which has democratized access for talented performers and broken the monopolies of traditional recording companies. After two decades of musicians utilizing social media, the emergence of streaming platforms, and the enduring appeal of live performances, we can now identify some clear trends.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The first is that streaming is here to stay, and it has opened up opportunities for music companies that can master the format and its delivery. The second is that legacy recording firms, with their ownership of classic recording libraries, have assets they can use to continue signing new performers. We’re witnessing the emergence of a hybrid music industry, in which recording firms continue to operate alongside streamers, while social media provides a large background platform.

Jefferies analyst James Heaney has been watching the music industry and has selected two promising music stocks for investors to check out. These are interesting picks, and they come from both the old and the new in the industry – a combination that highlights the advantages that both can offer.

We used the TipRanks database to understand why the analyst believes these stocks are worth considering now. Let’s take a closer look.

Spotify Technology (SPOT)

We’ll start in the streaming world, with Spotify. This company got its start in Sweden – its headquarters are in Stockholm – back in 2006, as an early leader in the field of music streaming. Since then, the company has grown, expanding both its audience base and its streaming programming by adding podcasts, including some of the best-known podcast franchises out there. Spotify has a multi-year contract, for example, with Joe Rogan. The company boasts that it hosts more than one million creative artists on its platform.

Spotify has become a well-liked platform, and attracts users through the use of the freemium service model. Anyone can access Spotify, and can stream songs and other programming, for free – but upgrades, including ad-free access, and premium content are available to paying subscribers. In addition, Spotify has made use of AI technology to monitor users’ playlists, and create a personalized listening experience through accurate suggestions.

Turning to Spotify’s last set of financial results, from 1Q24, we find that the company reported important gains in multiple key metrics. At the base, Spotify’s monthly active users, or MAUs, expanded by 19% year-over-year to reach 615 million. That number included a 14% year-over-year increase in subscribers, which reached 239 million. These large increases in the audience base reflect the popularity of online streaming – and provide a sound base for increased revenue. Spotify earned a top line of 3.6 billion Euros during Q1, up 20% year-over-year. We should note that the company’s revenues have been trending upward for the past several years.

The strong gains in user base and revenue underlie analyst Heaney’s thesis on SPOT shares, as he writes, “We are increasingly confident in SPOT’s ability to comfortably deliver sustainable 15%+ rev growth over the next 3 years. Underscoring our confidence in 15%+ sustainable rev growth is our view that music is about to undergo a multi-year repricing. At just $12/mo for a Spotify subscription (vs. $61/mo spent in aggregate on video streaming), we believe there is room for price increases AT LEAST every other year.”

Going on, the Jefferies analyst explains why his stance is more bullish than the average, saying of this stock and its prospects, “In our view, street ests. do not reflect the pricing potential, as we are 2% and 4% ahead on street rev in FY25 and FY26. Price increases from Apple and other streaming services would validate our bull thesis.”

Looking ahead, Heaney’s bull thesis leads to a Buy rating on SPOT, along with a $385 price target that suggests a one-year upside of almost 33%. (To watch Heaney’s track record, click here)

Overall, Spotify’s consensus rating from the Street’s analysts stands as a Moderate Buy, based on 29 recent recommendations that break down to 21 Buys, 7 Holds, and 1 Sell. The shares are priced at $290.16, and their average price target of $354.92 implies a gain of 22% over the next 12 months. (See SPOT stock forecast)

Warner Music Group (WMG)

The second stock on our list is one of the music industry’s legacy companies, Warner Music Group. This company is one of the three large-cap firms that dominate the recording industry, the historical gateway to a professional music career; its peers are Universal Music Group and Sony Music Entertainment. Warner owns some of the recording industry’s best-known labels, including Warner Records, Atlantic Records, and Elektra, and can boast of numerous high-profile musicians on its labels. Warner shows that, while social media and streaming have ‘leveled the field’ in the recording industry, the old school connections – and scale – still count.

In addition to its recording business, Warner is also a major power in music publishing. The company owns the rights to a huge library of recordings, with more than 1.4 million copyrights on music dating back 200 years. The company’s library spans a wide range of musical styles and eras, and also includes works by such major modern names as Prince, Madonna, and the Rolling Stones.

This company has a market above $16 billion, although its stock has underperformed in recent months; over the past year, shares in WMG are up just under 7%, where the broader NASDAQ has gained 29% in the same period. That said, Warner Music Group consistently generates quarterly revenue in the neighborhood of $1.5 billion.

In the company’s last quarterly release, covering 2Q24, Warner reported a top line of $1.49 billion, up 6.4% from the prior-year period and skating over the forecast by $10 million. At the bottom line, Warner reported earnings of 18 cents per share by GAAP measures, a figure that was 2 cents per share better than had been anticipated. Warner finished Q2 with a total debt of $3.984 billion, and cash holdings of $587 million – but on a positive note, saw capital expenditures decrease by 26% year-over-year, from $35 million to $26 million.

Assessing this stock, Jefferies analyst Heaney views the “current entry point for WMG as attractive,” and sees potential for long-term gains. He writes, “With the stock down YTD vs. UMG and the valuation now at a ~40% discount to UMG, we expect the stock to re-rate on more consistent release slates (e.g., Zach Bryan, Dua Lipa) and margin expansion via the recently announced cost savings program which should help drive ~200bps of adj. OIBDA margin expansion in FY24… Continued release strength and margin improvements lead us to be +1% / +3% in Adj. OIBDA vs the street in 25E / 26E.”

Altogether, this supports the analyst’s Buy rating, which he complements with a $38 price target that implies a one-year upside potential of 18%.

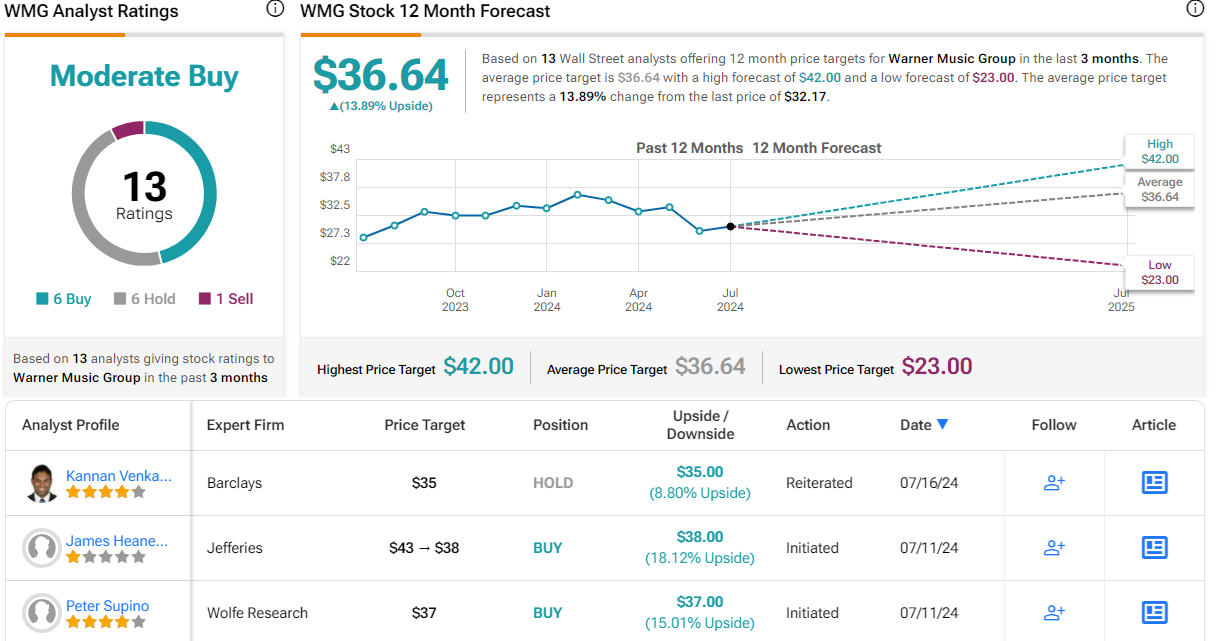

The analyst consensus on WMG shares is a Moderate Buy, based on 13 reviews that include an even split of 6 Buys and 6 Holds with 1 Sell thrown in the mix. The stock’s current trading price, $32.17, and its average target price, $36.64, together indicate room for a 14% gain on the one-year horizon. (See WMG stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.