The broader basket of retail stocks may not have been dealt the best hand in the world at the start of this year, with consumers continuing to hurt from inflation, geopolitical turmoil, and macro headwinds. Now that inflation is approaching its target (in the ballpark of 2%), it’s becoming less of a problem.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Still, don’t count on consumers to be any less selective, cost-conscious, and cautious, as the price increases from past years are in the books, so to speak — that is, unless some goods are in for a bit of deflation (think fast food) in the coming quarters. At this juncture, it’s likely best to be optimistic but still somewhat cautious when it comes to the retailers as a whole.

Like in the fast food scene, discounts and a high perception of value could continue to be the key to success in this environment. The following trio of retailers—JD, TJX, and TPR—seem to deliver on each front. Therefore, let’s check out TipRanks’ Comparison Tool to compare the names.

JD.com (JD)

Shares of Chinese e-tailer JD.com are fresh off a 26% plunge off 52-week highs. Undoubtedly, the multi-month plunge followed an underwhelming (but in-line) first-quarter showing that saw revenue rise 7% while operating profit fell 5%. The quarter may have been nothing to write home about, but with lower expectations, a depressed valuation, and ambitious expansion efforts, I’m inclined to stay bullish on the stock.

Perhaps the biggest draw to JD stock is the rock-bottom multiple. At 7.8 times forward price-to-earnings (P/E), JD is close to the cheapest it’s been in the past year.

The Chinese economy may be in a historic slump, and, of course, there are geopolitical uncertainties to account for. Either way, patient investors with a high pain tolerance may wish to back JD on the cheap as China attempts to turn a corner while JD looks to pull off a Temu of sorts by expanding internationally.

Unlike Temu, which sells dirt-cheap items at rock-bottom prices, JD tends to sell higher-quality, authentic products at still reasonable prices. When it comes to aggressive discounting, Temu is tough to top. However, JD may find success internationally as it brings goods that offer more on the quality front.

More recently, JD reportedly showed interest in buying British parcel firm Evri, a deal that could help accelerate its European expansion. I think acquiring its way to a solid logistical foundation is a pretty smart way to kick the international expansion into high gear. Whether such efforts to grow beyond China pay off in the medium term, though, remains to be seen.

What Is the Price Target for JD Stock?

JD stock is a Strong Buy, according to analysts, with 14 Buys and three Holds assigned in the past three months. The average JD stock price target of $40.58 implies 53.8% upside potential.

TJX Companies (TJX)

TJX is a discount retailing juggernaut that’s been in an unstoppable rally since bottoming out in the middle of 2022. The company behind TJ Maxx, Homesense, and Marshalls offers a wide range of brand-name merchandise at competitive prices. In the U.S., bargain hunting has kept TJX head and shoulders above most other retailers. And as TJX eyes an international expansion, there are reasons to believe TJX stock’s great bull run has legs. All things considered, I’m staying bullish on the off-price retailer.

In the (latest) first quarter of Fiscal Year 2025, TJX saw net sales grow 6% while comparable store sales crept 3% higher. Clearly, demand for a bargain has remained robust, even as inflation hit the brakes. What’s more remarkable is that the firm seems to have done a good job of maintaining inventory levels. After all, there’s nothing more off-putting than going to the local Winners or TJ Maxx to find a bunch of empty racks and shelves after other shoppers have scooped up the bargains with both hands.

Looking ahead, the firm sees comparable sales rising by 4%. That’s pretty impressive. But what’s even more impressive is the company’s expansion, which will see “at least another 1,300” new stores be opened. Ascending comparable sales and a solid store expansion plan is a formula for surging earnings and, with that, a rising stock.

At 26.8 times forward P/E, TJX stock looks quite rich now compared to the past-year range. However, when you consider the winning formula and continued demand for value, the premium seems more than warranted.

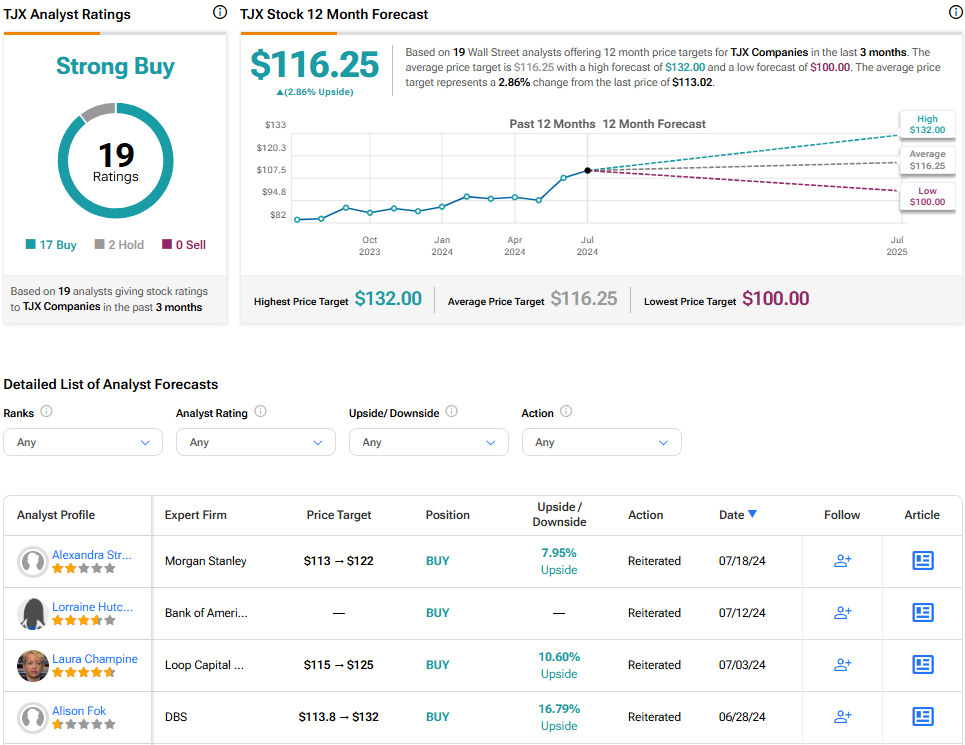

What Is the Price Target for TJX Stock?

TJX stock is a Strong Buy, according to analysts, with 17 Buys and two Holds assigned in the past three months. The average TJX stock price target of $116.25 implies 2.7% upside potential.

Tapestry (TPR)

Tapestry is a firm behind affordable luxury and fashion brands such as Coach and Kate Spade. These brands are a relatively cheap way for some to look and feel rich. The stock has been on an awful run since peaking back in February. Now down more than 17% from 52-week highs, questions linger as to how Tapestry can lift itself off the canvas following a mediocre third quarter that saw sales come roughly in line with expectations. With a depressed multiple and a potential path higher, I’m staying bullish.

Currently, the stock is trading at 8.1x forward P/E, which puts it at the low end of the past year’s historical range. With new product innovations over at Coach, like the Quilted Tabby, perhaps Tapestry can convince consumers to loosen the purse strings a bit, even as luxury demand (especially affordable luxury) hits a bit of a soft spot.

For now, it looks like Tapestry’s bid to buy Capri (CPRI) is dead in the water. Either way, Tapestry has more than enough dry powder to make deals elsewhere. Maybe now is as good a time as any to pursue other opportunities while the industry is still in a tough spot.

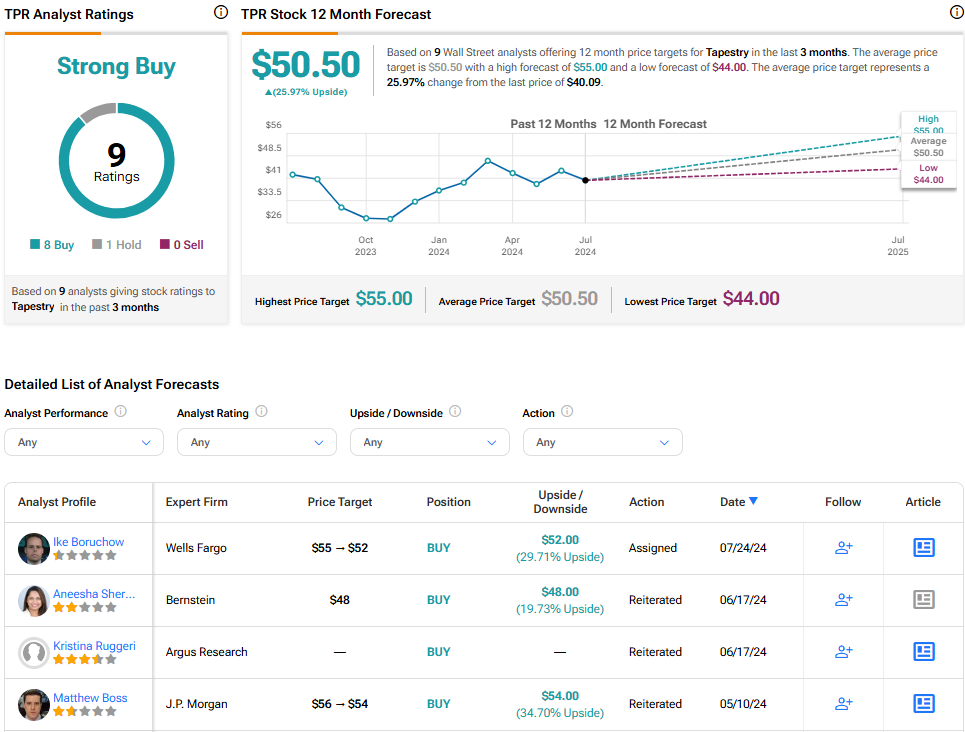

What Is the Price Target for TPR Stock?

TPR stock is a Strong Buy, according to analysts, with eight Buys and one Hold assigned in the past three months. The average TPR stock price target of $50.50 implies 26% upside potential.

The Takeaway

The following retail plays look quite enticing, according to numerous Wall Street analysts. Whether we’re talking about JD and its international push, TJX and its own expansion, or Tapestry and its fashionable new Coach bags and war chest, each name has overlooked strengths that may yet be factored into the share price. Of the trio, Wall Street sees JD as having the most room to gain (53.9%!) in the year ahead.