Investors searching for that feeling telling you market sentiment is shifting to a more positive outlook have been brought down to earth again. Following 2022’s market behavior to a tee, the recent rally has run into a brick wall. To wit, the S&P 500 notched 5 consecutive negative sessions over the last week with investors mulling over the prospect of a recession.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Indeed, financial experts have been sounding the warning bells on the precarious state of the global economy. One of the doomsayers has been J.P. Morgan CEO Jamie Dimon, who said recently that the Fed’s rate-hiking endeavors might not be enough to stave off a recession after all.

However, not all stocks are destined for the bargain bin. In fact, while Dimon fears for the economy, the analysts at JPMorgan see two names bucking the trend and pushing higher over the coming months – to the tune of 90% or more. Do other analysts agree with JPM? We’ve opened the TipRanks database to find out. Here’s the lowdown.

Norwegian Cruise Line (NCLH)

The first JPM-endorsed name we’ll look at is Norwegian Cruise Line, one of the biggest cruise companies in the world. Norwegian owns and operates three separate cruise lines, Norwegian Cruise Lines, Oceania Cruises, and Regent Seven Seas Cruises, with a total ship count of 28, riding the waves to 490+ destinations worldwide.

The last few years have been one long headache for the cruise-line industry. Unable to operate during the pandemic, the reopening came as welcome relief. The return to normalcy, however, has been interrupted with worries about the struggling global economy amidst soaring inflation and rising input costs. However, there appears to be plenty of pent-up demand too and with Norwegian focused on the premium market, its target audience might be less likely to feel the pinch of a recession.

In the company’s latest quarterly report, for 3Q22, revenue saw a huge 958% year-over-year increase to reach $1.62 billion, while the company delivered adj. EPS of -$0.64. Both results beat Street expectations. Occupancy rates are also getting better and reached around 82% of pre-pandemic levels. These are expected to keep on improving and reach the mid-to-high 80% range in Q4.

Covering the stock for J.P. Morgan, analyst Daniel Adam writes that he’s bullish on NCLH’s prospects, including among his reasons: “(1) disciplined market-to-fill (as opposed to discount-to-fill) pricing strategy; (2) outsized growth potential versus peers, as NCLH has a smaller, nimbler, and younger fleet with premium pricing; and (3) attractive relative valuation — particularly using estimates two or more years out.”

“In terms of size,” Adam went on to add, “NCLH commands only ~9% of the global cruise market. Accordingly, while it lacks the same scale benefits enjoyed by larger peers (CCL at ~38% capacity share and RCL at ~18%), NCLH has a greater opportunity for growth, which we consider a positive against the backdrop of strong pent-up leisure travel demand and the attractive value proposition that cruise lines offer versus land-based vacation alternatives.”

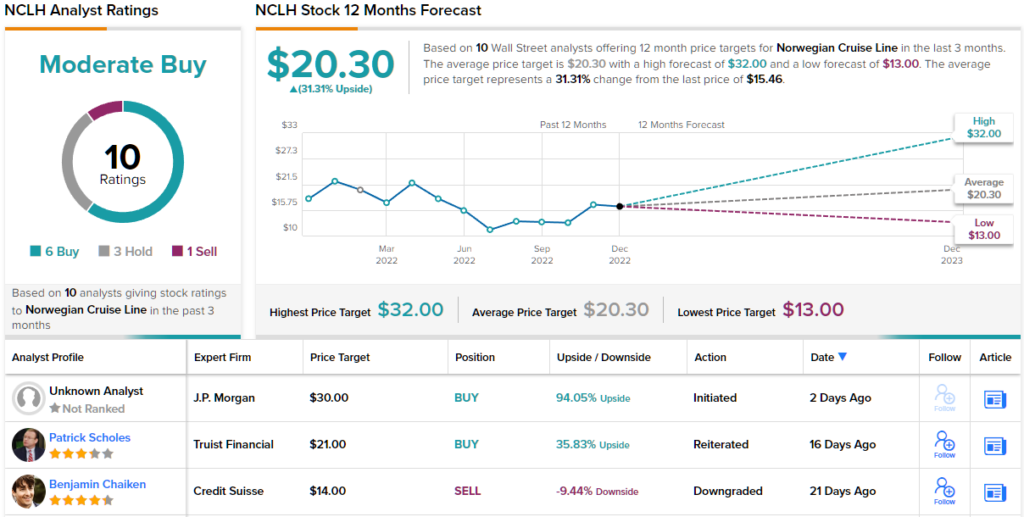

Accordingly, Adam rates NCLH shares an Overweight (i.e. Buy), while his $30 price target makes room for 12-month gains of 94%. (To watch Adam’s track record, click here)

What does the rest of the Street think? Looking at the consensus breakdown, opinions from other analysts are more spread out. 6 Buys, 3 Holds and 1 Sell add up to a Moderate Buy consensus. The shares are expected to reward investors with returns of 31% a year from now, considering the average target stands at $20.30. (See NCLH stock forecast on TipRanks)

Pliant Therapeutics (PLRX)

We’ll now pivot to a completely different sector for the next JPM pick. Pliant Therapeutics is a clinical biotech company with a remit to develop and bring to market novel treatments for a range of fibrotic diseases. The aim is to halt their progression, thereby safeguarding organ function.

The company’s lead candidate is bexotegrast (PLN-74809), an inhibitor of the αvβ6/αvβ1 integrins, which is being assessed in phase 2 studies for Idiopathic Pulmonary Fibrosis (IPF) and primary sclerosing cholangitis (PSC). In partnership with Novartis, the company is also developing αvβ1 inhibitor PLN-1474, whose phase 1 trial concluded in 2021 with the drug now moving towards phase 2 studies. There are also treatments for solid tumors and muscular dystrophy still in the pre-clinical stages.

PLRX shares have surged 156% higher over the past 6 months. The gains can be attributed to the results in the phase 2a study (INTEGRIS) of PLN-74809 in IPF, in which the drug met both its primary and secondary endpoints. Further updates from the high dose (320mg) cohort are expected in early 2023 and mid-way through the year.

It is LN-74809’s potential that has piqued the interest of JPMorgan’s Eric Joseph.

“In our view,” said the analyst, “lead candidate bexotegrast (PLN-74809) – a novel, dual selective αvβ1 inhibitor enjoys compelling biologic rationale for the treatment of IPF with an emerging mid-stage development field. In view of the multi-billion dollar commercial opportunity in IPF, we see current levels as not reflecting bexotegrast’s commercial potential in IPF and see additional optionality for bexotegrast in PSC.”

“Relative to some other mid-late-stage IPF development programs,” Joseph further explained, “we believe the INTEGRIS data set and (phase 3 program expected to similarly incorporate SoC) should set up ‘809 for a differentiated label breadth and flexibility of utilization- furthermore, our physician feedback indicates high preference for orals over IV administrated products in this category.”

Underpinning these comments with an Overweight (i.e. Buy) rating and $42 price target, Joseph sees the stock yielding additional returns of 130% over the one-year timeframe. (To watch Joseph’s track record, click here)

Joseph’s confident outlook is no anomaly; all 4 other recent analyst reviews are positive too, making the consensus view here a Strong Buy. The average target is slightly higher than Joseph’s objective; at $43.60, the figure suggests share gains of 139% are in the cards for the coming year. (See PLRX stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.