Spring is coming up , and investors will need to break out the crystal ball when looking at the market conditions. There’s a growing consensus that even though inflation is down from last summer’s peak, it has plateaued at a high level.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Watching the situation from banking giant JPMorgan, CEO Jamie Dimon takes the view that we won’t be getting back to the Fed target of 2% any time soon.

Furthermore, while Dimon hails an economy that is “doing quite well” with plenty of jobs to go round, he also stresses that there are plenty of uncertainties to consider. Or as Dimon succinctly puts it, “Russia, Ukraine, oil, gas, war, migration, trade, China” are all potential headwinds. “Out in front of us, there’s some scary stuff. And you and I know there’s always uncertainty,” he warned.

The standard play for investors to cope with this sort of uncertainty is to take a strong defensive portfolio position – and that will naturally bring us to look at the high-yield dividend stocks. These are the reliable payers that will give shareholders plenty of defensive attributes: a steady income stream, reliable payments, and inflation-beating yields.

So, let’s take a look at two stocks JPMorgan’s analysts have tagged as ones to favor in today’s climate. These are both Buy-rated stocks, with high dividend yields – over 13%, in one case. Here are the details.

AGNC Investment (AGNC)

We’ll start with a real estate investment trust (REIT). These companies have long been known as true dividend champions, and JPM’s pick, AGNC Investment, has long been known for its high-yielding payments. The company operates in the mortgage-backed security (MBS) niche of the REIT world, holding a portfolio totaling $59.5 billion in securities. That total includes $39.5 billion in residential mortgage-backed securities, and another $18.6 billion in net TBA (to-be-announced) positions. The largest part of AGNC’s portfolio, some 92%, is in 30-year fixed mortgage instruments.

The quality of the portfolio can be judged from the recent 4Q22 results. At the bottom line, the company realized net income per common share of 93 cents, some distance above the 66-cent forecast. In addition to solid earnings, the company had $4.3 billion in cash assets as of December 31, 2022. This total represented 59% of AGNC’s total equity.

For defensive-minded dividend investors, however, this company’s dividend payment is the real news. AGNC pays out monthly rather than quarterly, giving shareholders a more frequent payment schedule. The dividend, at 12 cents per common share annualizes to $1.44 per share and gives a powerful yield of 13.3%. That beats the last reported inflation data – 6.4% annualized in January – by 6.9 points, ensuring that shareholders won’t just have a reliable real rate of return, but that the return will be substantial.

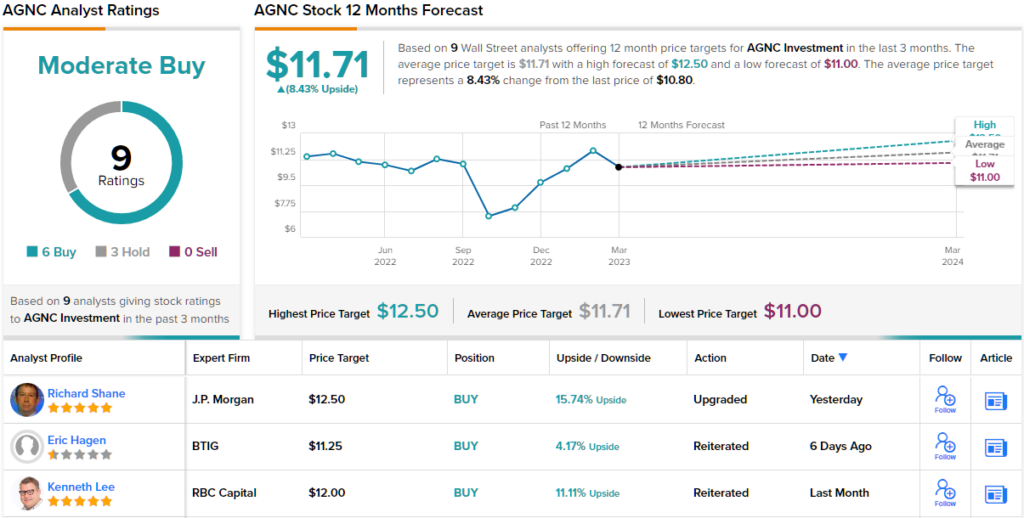

JPMorgan 5-star analyst Richard Shane covers AGNC, and in his most recent note saw fit to upgrade the stock’s rating from Neutral to Overweight (i.e. Buy). Backing his stance, Shane wrote: “We expect AGNC’s primarily Agency MBS portfolio to drive book value recovery as MBS prices recover and offer investors credit protection in a deteriorating economic environment. AGNC’s earnings fully cover its dividend and offer an attractive yield. AGNC is one of the best-managed MREITs within our coverage universe. In our view, being internally managed represents a long-term value driver.”

Putting some numbers to this, Shane gives AGNC shares a $12.50 price target, suggesting a one-year upside potential of ~16%. Based on the current dividend yield and the expected price appreciation, the stock has ~29% potential total return profile. (To watch Shane’s track record, click here)

Overall, with 9 recent analyst reviews on record, breaking down 6 to 3 in favor of Buy over Hold, AGNC shares get a Moderate Buy rating from the analyst consensus. (See AGNC stock forecast)

The Williams Companies (WMB)

For the second high-yield dividend pick, we’ll shift our gaze from REITs to energy. Williams Companies works in the US natural gas industry, operating a network of transport pipelines, gathering and storage facilities, and processing plants for natural gas. The company’s network is centered along the Texas-Louisiana coastline, extends into the Gulf of Mexico, and spreads out to Florida, the Mid-Atlantic and Appalachia, and northwest to the Rocky Mountains and the Pacific Northwest. Approximately 30% of the natural gas used daily in the US passes through Williams’ network.

The company recently released its results for the full year and fourth quarter of 2022. For the full year, Williams reported revenues of $10.9 billion, compared to $10.6 billion in 2021. From this, the company realized a net income of $2.04 billion, or a diluted EPS of $1.67. Drilling down to the quarterly level, the net income came to $668 million, or 55 cents per share. In non-GAAP adjusted terms, this gave a net income of $653 million, for a non-GAAP diluted EPS of 53 cents – that figure beat the forecast by 3 cents and was up almost 36% year-over-year.

It was also enough to guarantee full funding of the firm’s common share dividend, which in the January declaration was raised by 5.3%. The new payment, scheduled to be sent out this coming March 27, now stands at $0.4475 per common share. With an annualized rate of $1.79 per common share, the newly raised dividend yields a shade under 6%. While slightly lower than the current inflation numbers, the Williams’ dividend is still approximately triple the average payment found among S&P-listed div payers – and better yet, Williams has a rock-solid reputation for dividend reliability, having kept up its payments every quarter since 1974.

JPMorgan analyst Jeremy Tonet follows Williams Companies, and he likes what he sees. Tonet believes that Williams is one of the best-positioned natural gas companies, and writes: “WMB’s premiere existing ‘steel in the ground’ footprint provides clear competitive advantages to execute the company’s wellhead to market strategy… While current natgas S/D dynamics drives fears of rig drops and shut-ins to balance the market, we see the next leg of LNG demand balancing the market over the next one to two years, supporting an eventual uptick in natgas production levels. As such, with the potential for mid-single digit EBITDA CAGR, YE22 leverage sitting at 3.55x, and a peer leading ESG track record, we see a constructive backdrop over time, with the current ~6% yield providing support.”

Tracking his stance forward, Tonet gives WMB shares an Overweight (i.e. Buy) rating and sets his price target at $36, implying an upside of ~18% on the one-year time horizon. (To watch Tonet’s track record, click here)

Overall, WMB gets a Moderate Buy rating from the Street’s analyst consensus, based on 13 recent reviews that include 8 to Buy against 5 to Hold. (See WMB stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.