The video gaming scene seems to be on the cusp of some sort of consolidation as mega-cap tech looks to add to their services arsenals. Meta Platforms (NASDAQ:META), Take-Two (NASDAQ:TTWO), and NetEase (NASDAQ:NTES) are just three tech-savvy firms with major skin in the game (forgive the pun), and they’re Strong Buy stocks right now, at least according to the Wall Street community.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Indeed, it’s not hard to imagine the Magnificent Seven and FAANG firms striving to become more “fun” through the eyes of consumers as new technologies like the Metaverse become more widely adopted. Over time, I think gaming pure-plays will end up in the hands of a much larger tech firm that’s eager to “one up” peers who have shown they’re more than willing to expand their circles of competence and growth opportunities in the process.

So, without further ado, let’s check in with TipRanks’ Comparison Tool to see how the following highly-rated gamer plays stack up.

Meta Platforms (NASDAQ:META)

Meta Platforms is the Magnificent Seven stock that went from dud to top performer in a year. Undoubtedly, the stock crashed, shedding more than 76% of its value from peak to trough before kicking off one of the most impressive melt-up rebounds I’ve seen in mega-cap tech in quite a while. At writing, the stock has soared more than 250% from its early November 2022 lows. That’s an incredible return that will be nearly impossible to replicate for the next year.

That said, analysts still think the social media powerhouse could have more room to run, thanks in large part to its generative artificial intelligence (AI) prowess. In many ways, Meta has evolved into more of an AI company than anything else. Perhaps Mark Zuckerberg should change Meta’s name to LLM (Large Language Model) Platforms?

Moving forward, I expect Meta to stay on the cutting edge of consumer-facing AI tech. All the while, the firm continues to stay in its front-row seat to the still-nascent metaverse (or spatial computing) market. The Metaverse upside, I believe, may still be severely downplayed by the market, as the masses have almost all of their shifted focus to AI. AI is a massive growth driver for Meta, but so too could be the Metaverse. Given both powerful growth drivers, it’s hard to be anything but bullish on the stock.

Regarding Meta’s gaming/metaverse ambitions, its Quest 3 mixed-reality headset has received pretty solid reviews. It builds on its predecessors quite well while offering a competitive price of $499.99. However, there’s one thing that seems to be missing: a killer app. I believe that killer app is a triple-A game.

There’s no shortage of fun experiences and mini-games on the Meta platform. However, if Meta really wants to take the ball and run with it as Apple (NASDAQ:AAPL) looks to release its Vision Pro to the masses early next year, it needs to go big on gaming. As the spatial computing race gets more crowded next year, I’d argue the value (and pace) of video game acquisitions could surge.

Apple and Meta already have plenty of “game.” But for the metaverse to take off, they have to take it to the next level. And I believe that the next level lies in a big-budget virtual-reality production.

What is the Price Target for META Stock?

Meta’s a Strong Buy, according to analysts, with 36 buys and one Hold assigned in the past three months. The average META stock price target of $384.62 entails 23.7% upside potential.

Take-Two Interactive Software (NASDAQ:TTWO)

Take-Two Interactive Software is one such pure-play gaming firm that may be worth a great deal in the hands of a Magnificent Seven firm like Meta or Apple. Now that Activision Blizzard is off the market, I view Take-Two as the next best target. The $23.3 billion market cap makes Take-Two easily digestible for a firm in the Magnificent Seven. Still, the firm still seems like a two-hit-wonder with its Red Dead Redemption and Grand Theft Auto (GTA) titles.

Aside from its big two titles, Take-Two’s social and mobile gaming business looks impressive after its Zynga deal. Personally, I think Take-Two is a perfect fit for a firm like Meta as it seems to catapult the Metaverse to the mainstream.

Indeed, speculating on a takeover is a dangerous game. However, I view TTWO stock as cheap at current levels. Most of Wall Street seems to agree. Raymond James analysts are raging bulls over the potential for GTA VI (the latest title) to post “big numbers” once it releases. The title could be released “soon,” but there’s no release date set in stone quite yet. Raymond James is smart to look at TTWO through a longer-term lens. A new game is coming, and odds are it’ll be a profound hit, just like prior titles.

At writing, TTWO goes for 4.1 times price-to-sales, in line with the electronic gaming & multimedia industry average of 4.04 times. Given the big catalyst in GTA VI, TTWO probably deserves to trade a hefty premium to the peer group.

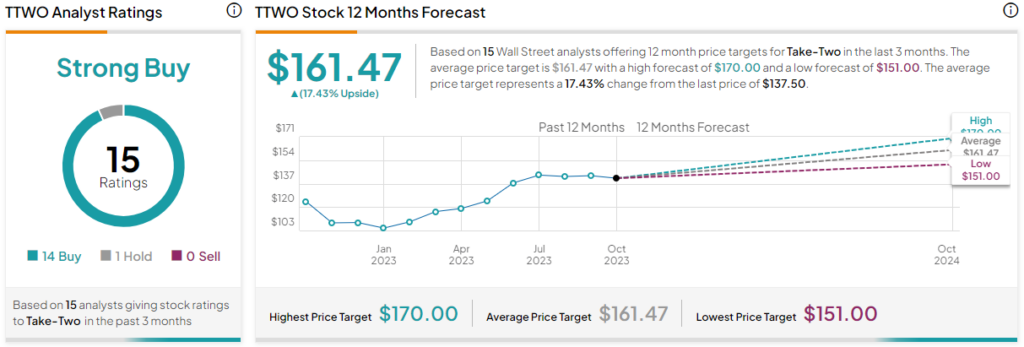

What is the Price Target for TTWO Stock?

Take-Two’s a Strong Buy, according to analysts, with 14 Buys and one Hold assigned in the past three months. The average TTWO stock price target of $161.47 and implies 17.4% upside potential.

NetEase (NASDAQ:NTES)

Finally, we have a Chinese gaming firm, NetEase, which has been off to the races this year, with shares now up more than 43% year-to-date. Just over a month ago, JPMorgan (NYSE:JPM) upgraded the stock over a line of new games. Indeed, China’s economy has been rather sluggish. But as a relatively cheap form of entertainment, I think NetEase could rise, even without help from the broader economy. As such, I’m staying bullish as the stock recovery continues.

The company’s margins may be weighed down for longer as Chinese consumers opt to spend less on microtransactions. In any case, I expect such spending could heat up should consumers really get absorbed into new releases. Further, China’s economy can’t keep sinking forever, opening the door to potential upside in the face of an eventual economic recovery.

Also, NTES stock looks quite cheap at 20.5 times trailing price-to-earnings, well below the gaming industry average of 31.9 times. Of course, investing in the Chinese market accompanies additional risks. However, if you’re willing to bear said risks, I view the potential rewards as compelling. However, NetEase seems like less of a takeover target than the likes of Take-Two. That rules out a potential spike for those looking to speculate on M&A.

What is the Price Target for NTES Stock?

NetEase is also a Strong Buy, according to analysts, with nine unanimous Buy ratings and an average price target of $128.00, suggesting 16.6% upside from here.

Conclusion

It’s not just fun and games for video game pure-plays and mega-cap tech titans looking to get into the game. As the economy heals, while big-tech firms become more competitive when it comes to gaming and the Metaverse, I’d look for gaming stocks to rise steadily over the coming years. Of the trio outlined in this piece, Wall Street expects the most upside from Meta stock (23.7%).