After a grisly 1H22 which represented the stock market’s worst performance since 1970, the second half is shaping up to be a bit of a disappointment too. After clawing back some of the losses, it’s been onto the slide again with the S&P 500 almost back to the mid-June lows.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The bad news, according to billionaire investor Carl Icahn, is that things could still get worse from here.

“I think a lot of things are cheap, and they’re going to get cheaper,” said Icahn, pointing to the economic malaise, and laying the blame squarely at the Fed’s feet, whose years-long fast and easy monetary policy Icahn see as the main reason behind 2022’s rampant inflation.

“We printed up too much money, and just thought the party would never end,” he went on to say before announcing that the “party’s over now.” For most, for sure, but it looks like Icahn’s nous has kept him way ahead of the pack this year too. Throughout the first six months of 2022, Icahn Enterprises’ net asset value rose by 30%.

So, it might be prudent for investors to follow Icahn’s lead right now and do so by leaning into the classic defensive play – dividend stocks.

With this in mind, let’s take a look at a pair of dividend stocks which form part of the activist investor’s portfolio; Both stocks significantly outperformed the market this year — highlighting their defensive strength in the current bearish environment. In tandem, we’ll open up the TipRanks platform and see how Wall Street’s analyst corps feel about these two choices.

FirstEnergy Corp. (FE)

We’ll kick off with FirstEnergy, an electric utility whose ten operating companies make up one of the country’s biggest investor-owned electric systems. The company provides electricity to millions of clients in the Midwest and Mid-Atlantic regions – all the way from the Ohio-Indiana border to the New Jersey shore. That is the main bread and butter for FE but it also has transmission operations; these include around 24,000 miles of lines and a pair regional transmission operation centers.

The past few years have seen the revenue haul stay pretty steady – ranging between $10.61 billion and $11.06 billion annually. In the latest set of results – for 2Q22 – revenue just outperformed that trend, growing by 7.7% year-over-year to $2.8 billion, while also beating the Street’s call by $70 million. The company also just beat expectations on the bottom-line, with adj. EPS of $0.53 coming in $0.01 above the $0.52 forecast.

As far as the dividend is concerned, it has remained steady at a quarterly payout of $0.39, providing a yield of 3.85%, above the sector average of 2.74%.

All of this makes for an interesting stock, at a time when defensive plays are gaining ground, and it’s clear that Carl Icahn would agree. His Icahn Capital hedge fund owns 18,967,757 shares worth $748 million right now.

However, there are some big changes taking place at FE. The company recently announced the retirement of president and CEO Steven Strah.

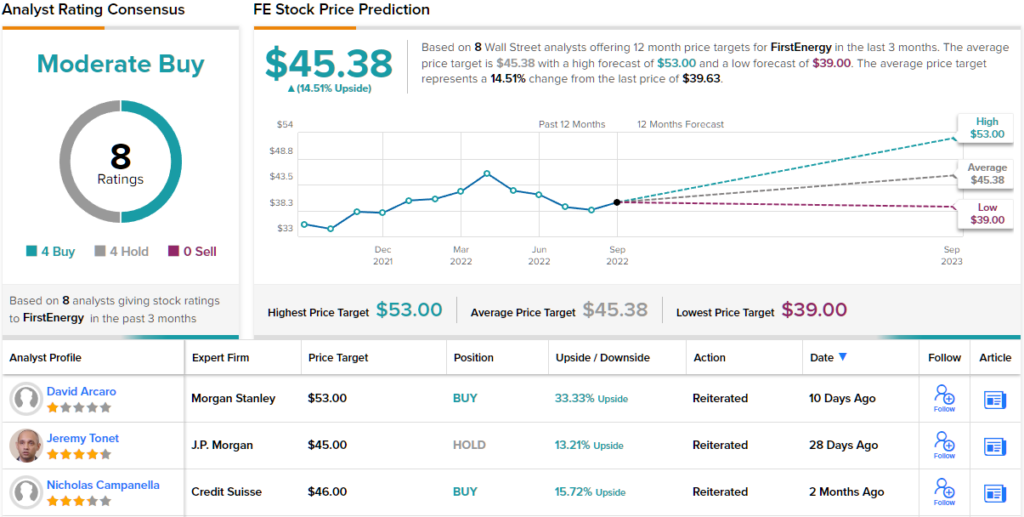

This does not stop Morgan Stanley’s David Arcaro from rating the stock an Overweight (i.e., Buy). With a price tag of $53, the analyst believes shares could surge 33% in the next twelve months. (To watch Arcaro’s track record, click here)

Backing his bullish stance, Arcaro writes: “We think the conclusion of the management review and the management transition underway together begin to resolve a key overhang on the stock around CEO uncertainty.”

The analyst added, “The potential for an accretive sale of a minority interest in the business and resulting improvement to the balance sheet supports a higher valuation and could come in the next few months. Execution on earnings through the year will help build the company’s track record and we think 2023 guidance next February could help reduce the investor concern related to pension EPS headwinds next year. Finally, the stock could begin to price in the possibility of M&A given the management transition.”

So, that’s Morgan Stanley’s view, let’s take a look now at what the rest of the Street has in mind for FE. Based on 4 Buys and Holds, each, the stock has a Moderate Buy consensus rating. The shares are selling for $39.75 and the $45.38 average price target implies an upside of ~15% from that level. (See FE stock forecast on TipRanks)

Southwest Gas Holdings (SWX)

For the next stock, will cross country to Southwest Gas, a Las Vegas, Nevada-based energy infrastructure holding company.

As part of Its regulated operations, the company provides natural gas, and boasts more than 2 million residential, commercial, and industrial clients in Nevada, Arizona, and California. The company also owns MountainWest Pipelines, an owner of 2,000 miles of interstate natural gas transmission pipelines. These are located in Utah, Wyoming and Colorado.

The unregulated arm of the business consists of Centuri, a utility infrastructure services company which caters to the North American utility, energy, and industrial markets.

Southwest has capitalized on the rising energy prices, as was evident in its latest financial statement – for 2Q22. Revenue increased by 40% year-over-year to $1.15 billion. However, the company was impacted by higher-than-anticipated expenses and supply chain snags which impacted the bottom-line. As such, EPS of -$0.10 fell some distance short of the $0.54 expected on Wall Street.

That had no effect on the dividend, however, which stands at a quarterly rate of $0.62, providing a yield of 3.15%.

It will be hardly surprising to learn that much of Icahn’s success this year has been by backing the energy sector – given the global crisis caused by Russia’s invasion of Ukraine, it is the one segment of the market which has rewarded investors. SWX stock has provided returns of ~12% on a year-to-date basis, far better than any of the major indexes, which all sit firmly in negative territory.

Icahn is evidently confident SWX will keep on outperforming. After loading up on shares in Q2, Ichan made another purchase in August, and he now owns ~5.8 million SWX shares worth around $445 million. With an 8.6% stake, Icahn is the company’s third largest shareholder.

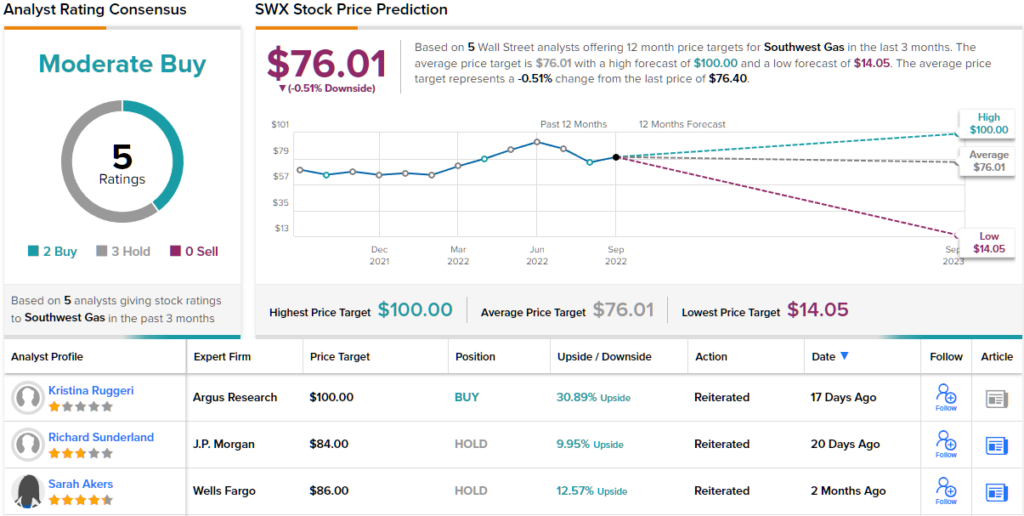

Like Icahn, Argus analyst Kristina Ruggeri likes the look of SWX, and sees the Q2 headwinds abating.

“The company was hurt this quarter by higher than planned operation and maintenance expense, higher interest expense from the MountainWest acquisition, proxy settlement costs and supply chain challenges that hindered infrastructure projects,” Ruggeri commented. “Southwest should overcome these challenges later this year. We have a favorable view of its long-term potential and its dividend, which yields about 3%. We note that the company is in the process of settling a rate case that should add over $50 million in annual rate relief and at least a 9.3% return on equity.”

Accordingly, Ruggeri rates SWX stock a Buy, while her $100 price target implies 12-month share appreciation of ~31%. (To watch Ruggeri’s track record, click here)

Overall, SWX receives a Moderate Buy rating from the analyst consensus. The stock has 5 recent reviews, including 2 Buys and 3 Holds. However, following the shares’ outperformance, the $76.01 average target suggests most think they are currently fairly valued. (See SWX stock forecast on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.