As if the past year has not provided enough bearish developments, there was more bad news for Tesla (NASDAQ:TSLA) investors last week. On Friday, the company announced that it is slashing the prices of its EVs in North America and Europe, with the cuts ranging from 6% to 20%, depending on model.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The aggressive cuts come in the wake of deteriorating demand against a weakening macro backdrop and increasing competition. Tesla missed Street expectations for 2022 deliveries, and CEO Elon Musk had warned that with a recession on the menu amidst rising interest rates, the company could reduce pricing to encourage volume growth while sacrificing the bottom-line.

While investors did not seem pleased, Wedbush analyst Daniel Ives thinks Tesla is making a canny move.

“Its no secret that demand for Tesla is starting to see some cracks in this global slowdown for 2023 with price cuts in China over the last week now being followed by eye-popping US/Europe reductions,” the 5-star analyst said. “While the initial reaction to these cuts will naturally be negative on the Street at first, we believe this was the right strategic poker move by Musk & Co. at the right time.”

While a few years ago the company would not be able to make such aggressive moves so to capture further market share in the “EV arms race,” with the Austin and Berlin factories at play and further build-out in China taking place, it has the “global scale” and “margin flexibility” to do so.

Ives believes the price cuts could result in demand/deliveries increasing by 12%-15% this year in what is obviously an “offensive” move. It is also a “clear shot across the bow at European automakers and US stalwarts (GM and Ford)” that with an EV price war now afoot, Tesla is “not going to play nice in the sandbox.”

“Margins will get hit on this,” Ives sums up, “but we like this strategic poker move by Musk and Tesla.”

To this end, Ives rates Tesla shares an Outperform (i.e., Buy) along with a $175 price target. If everything goes as planned, TSLA will soar about 33% over the next 12 months. (To watch Ives’ track record, click here)

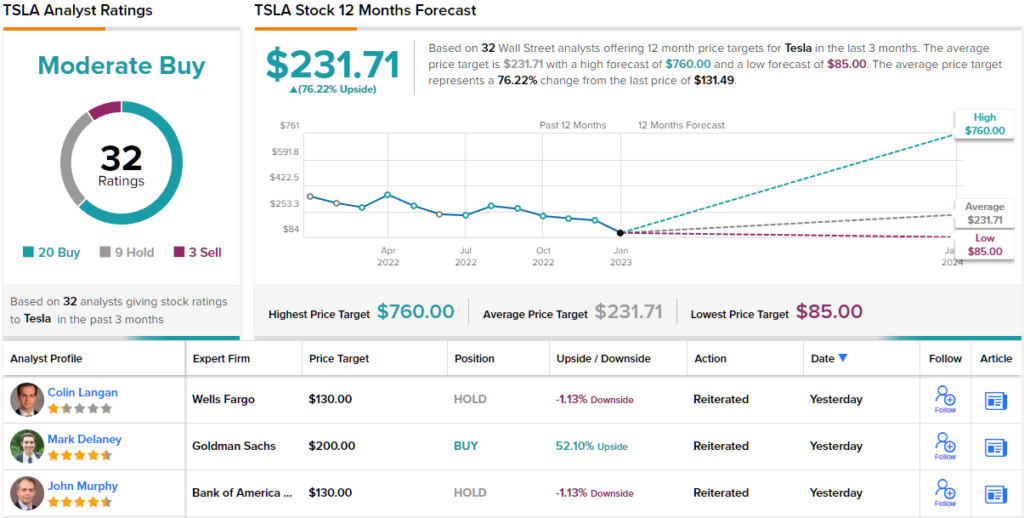

The Street’s average target is even more upbeat; at $231.71, the figure makes room for 12-month returns of 76%. The ratings offer a more balanced take; based on 20 Buys, 9 Holds and 3 Sells, the stock claims a Moderate Buy consensus rating. (See Tesla stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.