Stingray Group (TSE:RAY.A), a Canadian music, media, and technology company that provides audio television channels, radio stations, SVOD content, 4K UHD television channels, and more, recently rebounded from an earnings miss that saw the stock slip over 11% on November 9. Earnings per share (EPS) came in at C$0.15, less than the C$0.20 consensus. Also, revenue of C$77.6 million came in C$2 million under expectations. Despite the stock’s rebound, it still yields a very generous 6%, and it looks like a relatively safe 6% despite the company’s high debt level.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Let’s analyze Stringray’s profitability, growth, and dividend safety.

How Profitable is Stingray Group?

In the past four quarters combined, Stingray reported C$0.42 in EPS. For a C$4.95 stock, that’s pretty good. Its free cash flow in the same period is C$67.4 million, or C$1.05 per share – even more impressive. Additionally, management noted that it expects the company to generate about C$70 million of free cash flow this year, and Stingray has been consistently profitable on a free-cash-flow basis since at least 2013 (as far back as the data goes).

Regarding its growth, Stingray’s revenue is expected to grow by 12.4% in Fiscal 2023 (ending March 2023) and by 4% the following year. Earnings growth estimates for 2023 are -0.7% but are expected to rebound by 16.4% in 2024.

Is Stingray’s Dividend Safe?

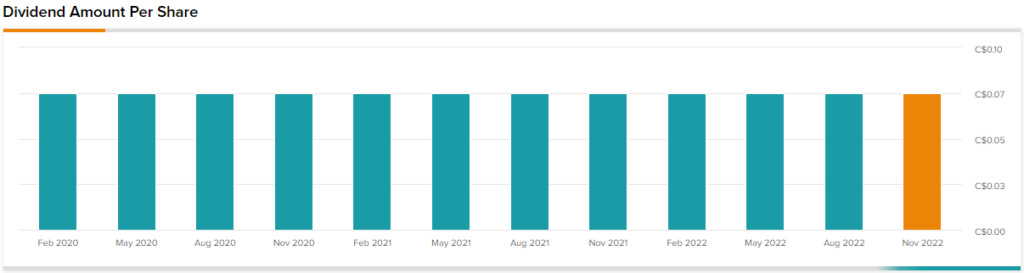

Some high-yield stocks are deceptive because those high dividends can be cut if the company in question is not in good shape. The good thing is that Stingray’s dividend does look safe. Its free-cash-flow payout ratio is a low 31.1%, meaning that only 31% of the company’s free cash flows are paid out as dividends. This leaves plenty of room for Stingray to raise its dividend if it wants to in the future.

Given that the company is expected to still be profitable in the next two years, we reckon that its dividend is healthy. However, there is one thing to consider – its high debt level.

Why Stingray’s High Debt is Manageable

Investors may become cautious when they see a C$344 million company with almost C$394 million in debt (and only C$15.4 million in cash). However, we believe that its debt levels are in the safe zone for a few reasons. First, the company’s trailing-12-months interest coverage ratio is 3.4x, meaning that it was able to cover its interest payments 3.4x over. Also, management stated its intention to reduce its debt load using its free cash flow.

Therefore, it’s possible that dividend growth and buybacks are going to be put on hold until debt comes down. Still, this is a prudent move from management, especially in a higher-rate environment.

Is Stingray Group a Good Stock to Buy, According to Analysts?

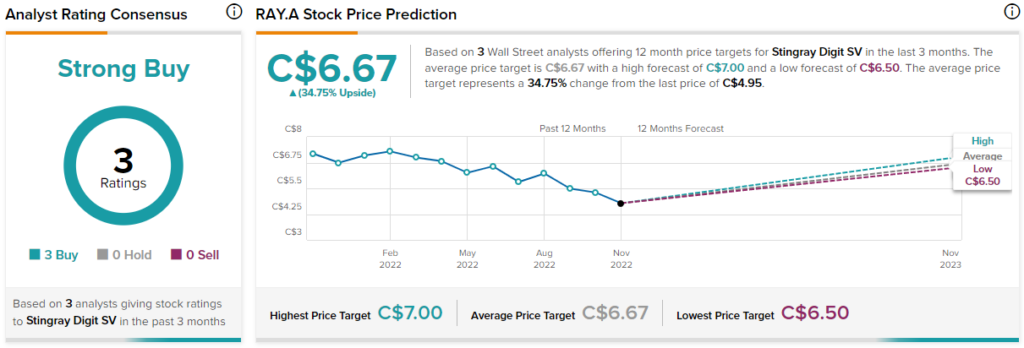

According to analysts, RAY.A stock comes in as a Strong Buy based on three unanimous Buy ratings. The average Stingray stock price target comes in at C$6.67, implying 34.75% upside potential.

Conclusion: Stingray Could be a Solid Income Stock

Stingray stock could be solid for income investors. The company even does buybacks, boosting shareholder returns. Its 6% dividend is well covered and has room to grow after the company deleverages its balance sheet. The company is consistently profitable and makes enough money to cover its interest payments. To top it off, all three analysts that cover the stock are bullish, giving it high upside potential.