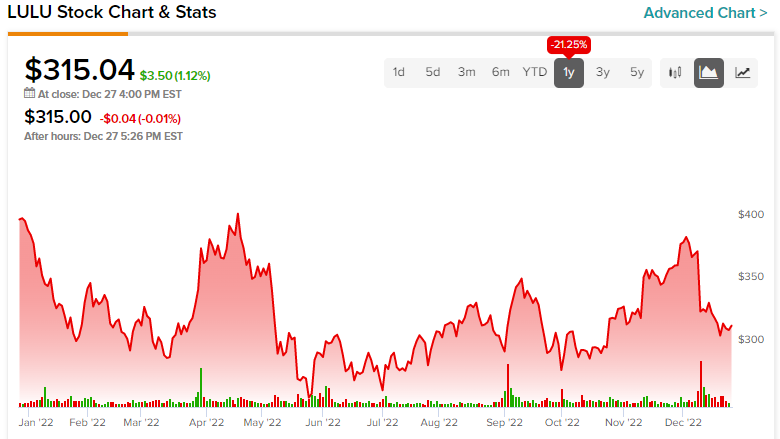

Shares of popular yoga wear maker Lululemon (NASDAQ:LULU) may be off around 35% from their all-time high hit in the back half of 2021. Still, the stock has held up far better than most other apparel plays over the past year. As we enter a likely recession year, questions linger as to whether Lululemon can keep outperforming peers going down the stretch or whether LULU stock will succumb to the same forces that have weighed down its rivals. Nonetheless, I believe LULU can hold up.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Undoubtedly, Lululemon boasts one of the strongest brands in the athletic apparel space. That said, Nike’s (NYSE:NKE) profoundly influential brand didn’t save its stock from shedding more than 53% from peak to trough.

Indeed, Nike had its fair share of company-specific issues. Most notably, supply-chain hurdles have caused the firm (and its stock) to stumble. More recently, inventory gluts and markdowns have been on investors’ minds.

Though the Nike brand entails strong pricing power, markdowns seem like the only solution to clear out old products at a time when consumers are being more prudent with their spending patterns.

Strong Growth Prospects Make Current Headwinds Forgivable

Lululemon isn’t immune to supply issues and swelling inventories. Industry headwinds are still hitting Lululemon. Much like Nike, Lululemon’s inventory levels have trended higher over the last few quarters. Undoubtedly, Lululemon’s growth runway looks more compelling than Nike or any other blue-chip athletic apparel play, for that matter.

Menswear and international growth opportunities are two non-traditional growth arenas that are relatively untapped. As Lululemon continues investing in such areas, there’s a good chance the firm can take market share and resist a portion of the hit from a global recession.

In any case, Lululemon seems better poised to pick up where it left off once the recession passes. Even if there’s more pain ahead, it’s hard to find a long-term growth story as compelling as that of Lululemon.

At writing, shares of Lululemon trade at 34.3 times trailing earnings, 27.5 times cash flow, and 5.3 times sales. All multiples are considerably higher than the apparel & accessories industry averages of 25.3, 18.0, and 4.3, respectively.

Indeed, bargain hunters in the apparel space may not be getting much of a discount with Lululemon shares. Still, I think Lululemon’s premium price tag is well-earned. I am bullish on LULU stock.

Higher rates and winds of a recession may have curbed the appeal of growth stocks. As a profitable growth company with enviable (and growing) margins, Lululemon seems like the type of growth play that could lead the way in a world where rates could stay elevated for longer.

Growth still matters as long as there’s more clarity on the type of return to expect from an investment. Lululemon’s pristine balance sheet (barely any debt) and robust free cash flows have done wonders for soothing investors amid the Fed’s tightening cycle.

Is LULU Stock a Buy, According to Analysts?

Turning to Wall Street, LULU stock comes in as a Moderate Buy. Out of 18 analyst ratings, there are 13 Buys, four Holds, and one Sell recommendation.

The average Lululemon price target is $412.06, implying upside potential of 30.8%. Analyst price targets range from a low of $200.00 per share to a high of $542.00 per share.

Takeaway: Expect LULU to Continue Outpacing Its Peers

Lululemon remains a discretionary firm. Demand for pricy yoga pants and hoodies will likely hit a snag in 2023 as a recession nears. Still, a “mild” downturn is unlikely to have a long-lasting effect on the company’s growth profile.

The company’s “Power of Three x2” five-year plan is still in place. Innovation, e-commerce, and international growth remain arenas that could help Lululemon pressure the competition as it looks to pad its margins further. Gap’s (NYSE:GPS) Athleta has proven a worthy contender with a lower sticker price.

Lululemon’s brand and innovation-driven five-year plan may help it stave off rivals like Athleta. Only time will tell if Athleta can tilt the market in its favor as economic times get more challenging. Regardless, I think Lululemon’s brand power may be more potent than many analysts believe.

Going into the first quarter of 2023, I expect inventory markdowns could weigh on near-term margins. Lululemon’s managers have already warned of above-average inventory levels. Nike and other well-run retailers can’t do much about the matter — elevated inventory is just another sign of the times for the apparel firms.

Fortunately, discounting may be viewed as more of a double-edged sword than a dagger to the heart. Steep discounts and a potentially sizeable Boxing Day sale could help Lululemon overcome its sales slowdown.

In short, Lululemon’s a long-term winner that’s been tripped up of late. I bet the firm will find its footing and not fall flat on its face, even with hostile conditions.