The question in the title is straightforward, but the answer is less so. However, in my opinion, CRWD stock is a Hold, and I will explain why I hold this position.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Cybersecurity giant CrowdStrike (CRWD) is set to report its June quarter results on August 28. Despite a mild correction following a recent massive selloff caused by a global outage, I still consider it too risky to adopt a bullish stance ahead of its earnings report, and so, contrary to Wall Street analysts, I remain neutral on CRWD stock.

Over the past year and a half, the company has been one of the main beneficiaries of AI tailwinds, with its market cap nearly quadrupling during this period. While CrowdStrike is likely to report a strong Q2, the financial and reputational impacts of the outage remain uncertain, raising concerns about how this may affect the company in both the short and long term.

In this article, I will discuss recent developments and what to expect from the company’s Q2 results.

CrowdStrike’s Outage

CrowdStrike’s investment thesis is based on its position as arguably the best-placed company in the cybersecurity space. Known for its user-friendly Falcon platform, which uses artificial intelligence and behavioral analysis to detect and prevent threats in real-time, CrowdStrike stands out as the leading AI-driven cybersecurity company.

With the ongoing AI gold rush in the tech space, CrowdStrike’s stock has been one of the major beneficiaries. From January 2023 to early July, the company’s shares surged over 300% to reach all-time highs, reflecting the strong momentum driven by an impressive three-year revenue CAGR of 48.7%.

However, the bullish thesis took a significant hit on July 19, when CrowdStrike faced a substantial and unprecedented outage that caused service interruptions and affected several industries, including healthcare, banking, airlines, and retail.

Although the company’s management responded quickly and seemed to handle the aftermath of the crash effectively, the incident left a mark that transcended mere financial aspects; it struck at the company’s reputation, something much harder to quantify. On the positive side, the outage was not related to security flaws but to a specific update problem. For a cybersecurity company, a hack would have been a far more serious problem.

Nonetheless, I remain neutral as this incident halted the bullish momentum and led to the company’s devaluation by around 42% in just over two weeks. Although this devaluation might have been overly extreme – since it was likely a one-off event – there are a few unresolved points to consider.

First thing to consider is before the outage, CrowdStrike traded at a price-to-sales ratio of over 29x, a very high multiple compared to Palo Alto Networks’ (PANW) 15x. This high valuation left CrowdStrike with little room for error. The highly competitive cybersecurity space further complicates the situation, where even minor missteps can lead to a loss of market share and trigger sell-offs. Additionally, there may be potential litigation related to the outage, which caused losses across various industries.

Another thing to consider is the extent to which this event will financially impact the company in the coming quarters or years. This aspect remains uncertain, as does how CrowdStrike will address this issue with its customers.

While this one-off event has undoubtedly shaken the company’s fundamentals, introducing numerous uncertainties, it’s still unclear how much of this has been fully priced in. Investors who attempt to catch the falling knife may get hurt.

Could Q2 Earnings Shift the Outlook for CrowdStrike?

As CrowdStrike’s earnings for the June quarter approach, I remain highly skeptical about the chances of an immediate turnaround in the bearish momentum.

While I believe CrowdStrike is likely to report a good quarter, potentially topping estimates, the effects of the outage are unlikely to be reflected in Q2 results. Analysts have a mid-point EPS projection of $0.97 for Q2, which, if achieved, would represent an annual growth of 30.7%. On the top line, analysts expect Q2 revenue to come in at $957.8 million, marking an annual growth of 31%.

These top-and-bottom-line projections still reflect a degree of optimism among analysts over the past three months. Thirty analysts have revised their EPS forecasts upwards, while only six have revised downwards. For revenue, 24 analysts have revised upwards, and 11 have revised downwards.

The situation is less optimistic when looking at full-year estimates, where 15 analysts have revised EPS downwards and 27 upwards, now expecting annual growth of about 27%. Meanwhile, 16 analysts have revised revenue downwards and 24 upwards, reflecting annual growth of 29.7%.

Outage-affected customers are very likely to renegotiate their deal terms with CrowdStrike, which could influence churn rates. Therefore, it will be crucial to see how management handles its guidance for the full fiscal year, which currently forecasts revenue between $3.97 billion and $4.01 billion.

It will be challenging to maintain this guidance and given the difficulty in predicting the outage’s financial impacts on their operations, I believe taking any position before Q2 earnings could be speculative.

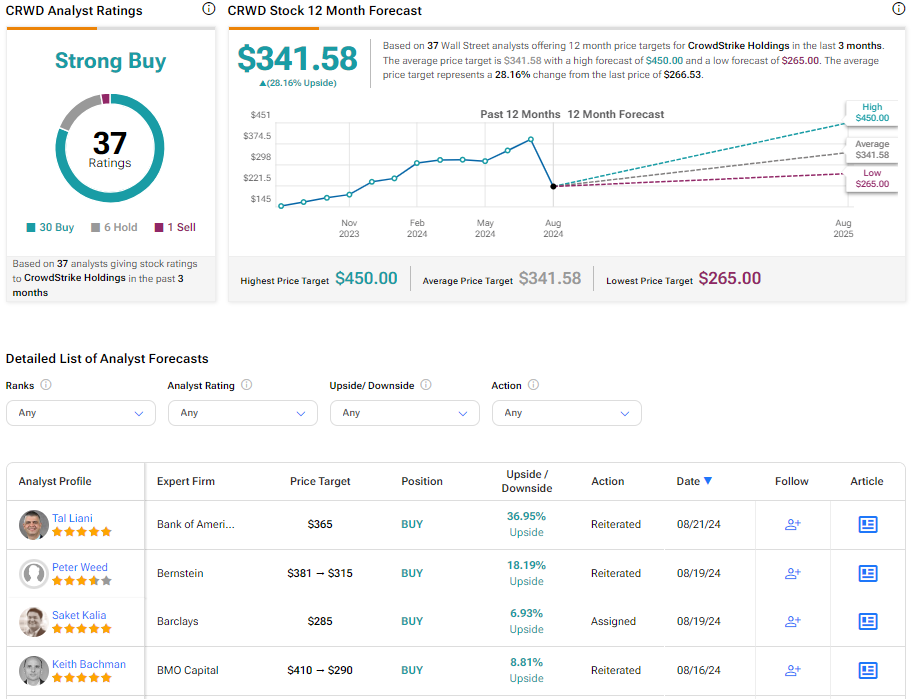

Is CRWD A Buy, According to Wall Street Analysts?

The consensus around CrowdStrike remains mostly bullish, with 30 out of 37 analysts recommending a buy despite four downgrades following the outage incident. Additionally, 16 analysts trimmed their price targets for CrowdStrike shares after the outage. Based on the latest share price, the average price target now stands at $341.58, which still represents a sizable upside potential of 28.16%.

Key Takeaways

CrowdStrike remains a leading player in the cybersecurity sector, bolstered by AI-driven growth. However, the recent global outage has introduced significant risks to its investment thesis. While Q2 earnings are expected to be strong, the full impact of the outage remains uncertain, making a bullish stance questionable. With potential legal issues, customer renegotiations, and a high valuation, caution is advised despite Wall Street’s largely intact bullish consensus. Therefore, as state before, I am neutral on CRWD stock.