Axon Enterprise (NASDAQ:AXON) is a manufacturer of electrical weapons and technological solutions for the military, law enforcement, private security, and civilians. In a year that stocks have been hammered, Axon’s market value has increased by more than 18%. As a result, the stock is no longer cheaply valued at a forward price-to-earnings ratio of 92x. However, Axon seems well-positioned to grow by double digits in the next five years, similar to how it has grown in double digits over the last 10 years. Based on valuation concerns, I am neutral on the prospects for Axon Enterprise stock, but I believe investors with a higher risk appetite will find Axon stock appealing.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

What Does Axon Enterprise Do?

Axon Enterprise operates in two segments: TASER and Software and Sensors. Under the Taser segment, the company manufactures and sells conducted energy devices for user protection and virtual reality training. The Software and Sensors segment develops fully-integrated hardware and cloud-based software solutions such as on-officer body cameras, fleet in-car systems, digital evidence management systems, and signal-enabled devices.

Axon has a global presence, and its customers include U.S. state and local governments, the U.S. federal government, international governments, commercial enterprises, and more.

Axon Continues to Smash Wall Street’s Expectations

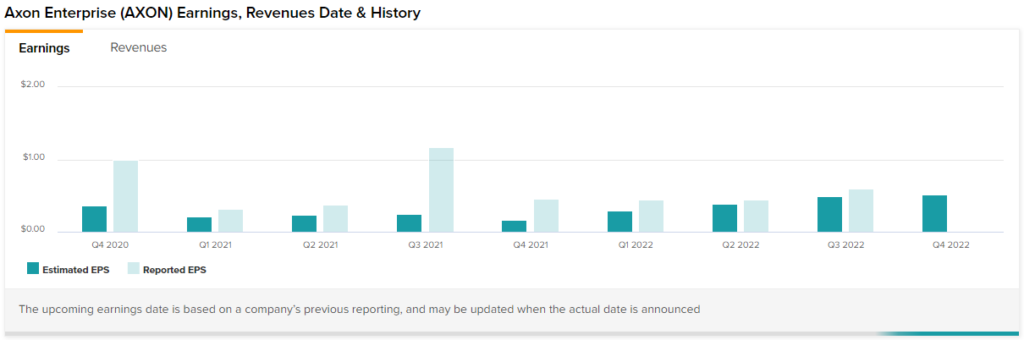

On November 8, Axon reported third-quarter revenue of $312 million, up 34% year-over-year and beating estimates of $279.9 million, driven by robust growth across all of its segments. Earnings per share also came in at $0.60 vs. the $0.49 consensus estimate.

TASER segment sales increased by 19% to $144.9 million. Management emphasized that the growth was driven by a significant customer adopting the premium TASER 7, which has a higher average selling price and includes a greater number of cartridges in bundles. Furthermore, Axon has successfully transitioned its TASER hardware business into a subscription service, with 63% of TASER devices sold on a subscription in the third quarter.

With the positive response to its subscription services, Axon is gradually introducing subscription services in mature markets and expanding into new markets. Cloud and Sensors segments, on the other hand, both reported a 51% increase in revenue to $96 million and $71 million, respectively.

In terms of customers, the U.S. federal government booked contracts worth more than $200 million in the first three quarters of 2022, with deliverables spanning several years. In addition, Axon extended partnerships with several federal offices, which employ approximately 137,000 federal civilian law enforcement agents. The company also received contracts for body camera programs from the United States Marshals Service, the Drug Enforcement Administration (DEA), and the United States Park Police.

Following the May 20, 2022 issuance of the “Executive Order on Advancing Effective, Accountable Policing, and Criminal Justice Practices to Enhance Public Trust and Public Safety,” which requires federal agencies to adopt body-worn camera policies, the U.S. Department of Veterans Affairs became the first agency to award a contract to Axon for a new body camera program. The department signed a $60 million contract that has the potential to expand in the future. Axon was also awarded a contract by the United States Secret Service Uniformed Division to deploy TASER 7, a less-lethal technology.

In the third quarter, total future contracted revenue increased to $3.73 billion, with the company expecting to recognize 15% to 20% of this balance over the next 12 months and the remainder over the next 10 years. Annual recurring revenue of $403 million increased by 40% year-over-year in Q3, and its gross margin of 62% saw an improvement of more than 100 basis points sequentially.

Additionally, Axon’s renewed agreement with Microsoft Azure boosted gross margins in Q3. For reference, in 2015, both companies collaborated to provide agencies with integrated cloud, mobile, wearable, and analytics solutions. The company renewed its cloud-hosting contract for another six years in the hopes of gaining long-term pricing certainty and cost visibility for its Axon Cloud business.

Axon Enterprise’s Guidance Gets a Boost

Axon lifted its fourth-quarter guidance, given the ongoing growth trend. In Q4, the company anticipates revenue of $300 million to $310 million, representing a 40% year-over-year increase at the midpoint. The company also raised its revenue forecast for Fiscal 2022 to a range of $1.15 billion to $1.16 billion, representing approximately 34% year-over-year growth at the midpoint. Axon had previously guided to a revenue range of $1.07 billion to $1.12 billion.

Axon still has a lot of room to grow. During the quarterly conference call, management stated that the company’s global addressable market is still only 10% penetrated. Axon continues to invest in new technologies to improve global public safety, such as virtual reality training, next-generation body cameras, and real-time and remote response devices, to achieve its goal.

Is Axon Enterprise a Good Stock to Buy, According to Analysts?

Axon is gaining popularity among Wall Street analysts as the company continues to win long-term contracts and report substantial top and bottom-line growth. Axon has a Strong Buy consensus rating based on seven Buys and one Hold rating assigned in the past three months.

Nonetheless, at $170.75, the average Axon price target implies 5.8% downside risk. However, analysts have positively adjusted their price targets for Axon in recent months. If this trend continues into the next couple of quarters, the company could soon be viewed as fairly valued at a time when many growth companies are struggling to book any growth.

Takeaway: Axon Enterprise is Worth Monitoring Closely

Axon is firing on all cylinders, as evidenced by its most recent quarterly report. The company’s Cloud and Subscription businesses are gaining traction, and it is adding new categories of customers. With its distinct product offering and little direct competition in the law enforcement and public safety sectors, Axon Enterprise is well-positioned to grow exponentially in the next decade. Although the company seems richly valued today, growth investors should closely monitor future developments to identify a possible entry point to invest in this fast-growing, under-the-radar company.