High-end luxury goods stocks do not tend to do well in the face of an economic downturn. Although many investors have braced for a coming recession, not all high-end stocks have sunk into the abyss. Surprisingly, the highest-end luxury brands have done a remarkable job holding their own. And at this pace, they could continue to do so even as a recession comes and goes.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

With inflation driving up the cost of goods through the roof, a select class of Veblen goods — goods that tend to experience more demand as prices rise — have been in a unique and enviable spot. Consumer flock to the very high end of the luxury apparel space for brands that offer them status. The higher the price, the more exclusive an item tends to be.

In that regard, some high-end brands have been able to steer clear of the inflation and macro headwinds that have caused most to tighten their purse strings. Recessions don’t always hit income classes equally. And in that regard, investors may wish to give some of the luxury plays a second look.

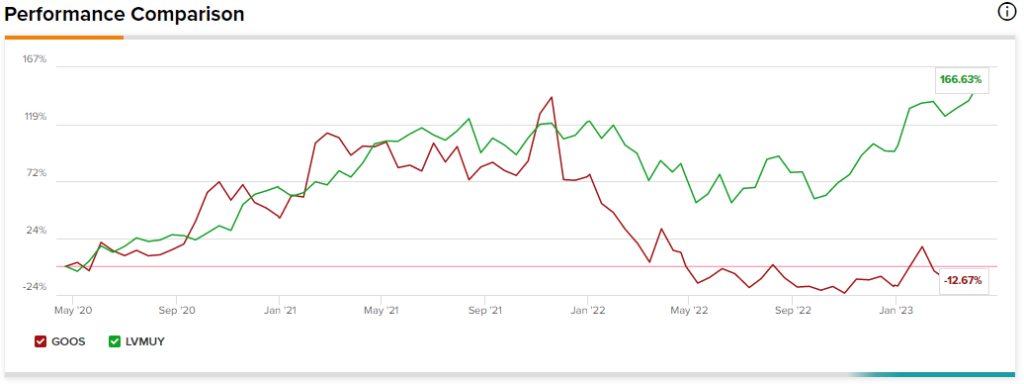

Therefore, let’s use TipRanks’ Comparison Tool to check in on two high-end “Veblen” plays to see how they stack up as we inch closer to a much-anticipated recession.

LVMH Moët Hennessy Louis Vuitton SE (OTC:LVMUY)

LVMH is a French luxury firm behind some very high-end brands, including Louis Vuitton, Dior, and Tiffany. Regarding status symbols, it’s tough to stack up against LVMH’s lineup. Even as recession winds give a chilling blow to consumer spending levels, LVMH stock seems unshakeable, with 48% gains over the past year and more than 240% gains since its lows of 2020. At writing, shares are at an all-time high, right around $200 per share.

The marvelous run has helped mint CEO Bernard Arnault as the world’s richest man, surpassing ultra-wealthy tech pioneers Elon Musk and Jeff Bezos. Despite the overheated run, I remain bullish on LVMH as its demand seems unlikely to back off anytime soon as the firm keeps bucking the trend, clocking in incredible growth in a sluggish global economy.

Earlier this month, LVMH clocked in a stellar fiscal first quarter that saw a 17% pop in revenue. The firm saw strength across the board and across different markets. The Asian region, in particular, saw a nice rebound as COVID restrictions were lifted.

Moving forward, I view China’s booming middle class as a significant driver of long-term sales growth. Indeed, high-end brands are a big deal in China. In that regard, the company has a front-row seat to a generational secular boom that could make LMVH stock tough to pass up.

As it turns out, it’s not so easy to build a brand to the magnitude of the likes of a Louis Vuitton or a Dior. It takes many decades to build brand affinity and a reputation among consumers. In that regard, LVMH has a very wide moat and is worth venturing into the OTC markets for American investors seeking exposure.

Undoubtedly, LVMH isn’t the only way to play the luxury space. There are alternatives that are more easily accessible to U.S. investors who wish to stick with the NYSE or Nasdaq exchanges. That said, I see few (if any) publicly-traded firms that can match LVMH’s profoundly powerful roster of brands.

The French firm is essentially the gold standard of luxury goods, and these days, high-end consumers seem to be giving the highest end of the luxury goods waters the most love.

At 32.1 times trailing price-to-earnings (P/E), shares are trading slightly below the apparel and accessories industry average of 32.5 times. Indeed, the premium apparel play has a stock that itself lacks a premium to the peer group.

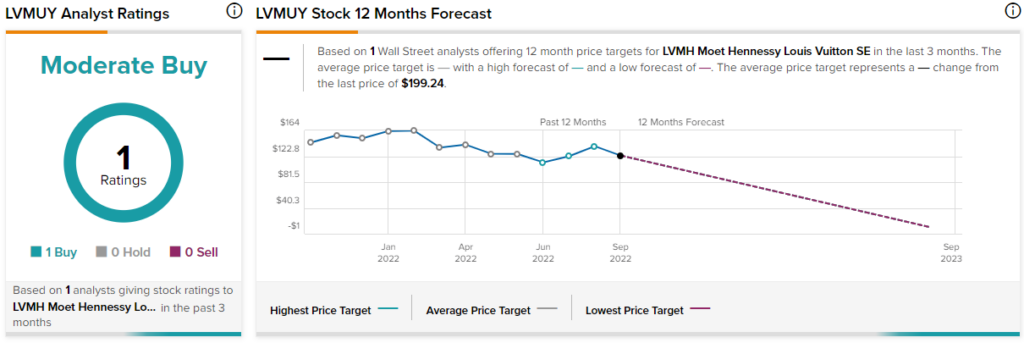

Is LVMUY Stock a Buy, According to Analysts?

At writing, LVMUY stock only has one rating. It’s a Buy, but there’s no price target.

Canada Goose (NYSE:GOOS)

Canada Goose is a Canadian luxury outerwear company that’s built a good amount of brand affinity for itself over the years. Despite the glorious rise of the Canada Goose brand, its stock has been stuck in a rut for a few years now. Shares are down more than 73% off their 2018 highs and have been fluctuating in a channel between $15-$25 per share.

Even if Canada Goose can’t catch a break as some of its high-end peers zig while the economy zags, I remain bullish on GOOS stock for its longer-term growth prospects. Today’s depressed multiples are also enticing for those who believe in the brand and its ability to fly higher on the other side of a downturn.

Evercore recently slashed its Canada Goose rating to Hold, raising concerns about the firm’s ambitious path to growth. For context, Canada Goose CEO Dani Reiss highlighted the company’s plan to triple its revenue by 2028, noting of the opportunity to expand into new product categories beyond outerwear.

Reiss has a vision and the know-how to meet such an ambitious goal. That said, analysts remain skeptical. Evercore notes that Canada Goose faces stiff competition as it ventures into new categories. While I partially agree with the skeptics, I do think many may be discounting the power of the Canada Goose brand.

Sure, it’s not at the level of Dior, but it could still benefit greatly from an increased appetite for high-end goods after a recession fades.

What is the Price Target for GOOS Stock?

Canada Goose boasts a Hold rating, with three Buys, five Holds, and one Sell assigned in the past three months. The average GOOS stock price target of $20.81 implies a modest 8.7% in upside potential.

Conclusion

LVMH and Canada Goose represent a stark contrast in the world of high-end retail. Currently, I’m a bigger fan of LVMH because it has compelling brands that are nearly impossible for up-and-comers to replicate.