Intuitive Surgical (NASDAQ:ISRG) beat Wall Street’s Q4 top- and bottom-line estimates recently, igniting further momentum in the stock’s upward trajectory. The robotic surgery leader ended Fiscal 2023 on a high note, showcasing high revenue growth and expanding margins. Despite Intuitive hitting new all-time highs post-earnings, I believe the stock may have more room to run, moving forward. With the company’s market-leading position providing an ample runway for continued success, I remain bullish on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Growth Acceleration Fuels Investor Confidence

It’s quite impressive how Intuitive Surgical has managed to maintain such strong investor confidence in its stock. Its most recent results underscored why, showcasing an impressive acceleration in growth. In the fourth quarter, revenues soared by 17%, reaching $1.93 billion. Noteworthy is not only the company’s surpassing of Wall Street estimates by $30 million but also the strong acceleration in growth, outpacing both Q3-2023’s 12% and the previous year’s 6.7%.

Intuitive Surgical’s sustained leadership in robotic surgery for over two decades is genuinely intriguing. How they’ve managed to keep growing, even as the industry matures, boils down to a simple factor, in my view: they’ve been riding the rising wave of global adoption in robotic surgery. The robotic surgery industry is still in its early phases, holding immense potential for expansion.

Taking a closer look at the industry landscape reveals a clear trend toward the rising popularity of minimally-invasive procedures. Following years of rigorous R&D and continuous improvements, robotic surgery has become quite cost-effective.

It makes sense for hospitals to adopt this technology, as they see the potential for boosted surgical revenues and reduced expenses attributed to lower complication rates and shorter hospital stays. At the same time, the demand for more comfortable procedures is growing. Thus, you can see why Intuitive’s performance currently benefits from a strong secular growth tailwind.

To add some context to this argument through numbers, in Q4, Intuitive installed 415 da Vinci surgical systems in hospitals compared to 369 last year. This clearly shows the gradually growing demand from hospitals to start offering robotic surgery or expand their capabilities.

In fact, Intuitive’s da Vinci surgical system installed base reached 8,606 systems at the end of the quarter, up 14% versus 7,544 at the end of 2022. The combination of a higher installed base and growing patient demand for invasive procedures resulted in worldwide da Vinci procedures growing by about 21% year-over-year, fueling Intuitive’s revenue growth acceleration.

Snowballing Profits Challenge Valuation Concerns

With revenue growth accelerating and Intuitive achieving improving unit economies, its profits have started to snowball. I believe that this trend challenges the elevated concerns of some investors, who argue that Intuitive stock could be overvalued. Let’s examine.

Intuitive achieved a net income margin of 31.4% in Q4. This is one of the highest reported margins in the medical devices industry I have encountered in my research. It’s also notably higher than the prior quarter’s net income margin of 23.8% and 19.6%, which the company posted in the previous quarter and last year, respectively. It clearly underscores Intuitive’s ongoing margin expansion, which, along with its strong revenue growth, enabled an extraordinary net income increase of 86.5% to $606.2 million.

This was Intuitive’s most profitable quarter since its inception, boosting its Fiscal 2023 net income to a new all-time high of $1.8 billion. Interestingly, about $192.1 million of this amount can be attributed to Intuitive’s massive net cash position of $7.34 billion, generating solid interest income due to rising interest rates. This comes bundled with Intuitive essentially having no debt on its balance sheet, highlighting its financial soundness even further.

The significance of this lies in its contribution to investors’ willingness to pay a premium for the stock. Intuitive’s remarkable earnings growth, coupled with its clean, cash-rich balance sheet, has prompted many to pursue the stock, pushing its valuation to seemingly hefty levels. Currently trading at about 16x and 59x Fiscal 2024’s projected sales and earnings per share, respectively, it’s evident why some investors view the stock as overvalued.

However, I believe that Intuitive’s dominant market position, ongoing acceleration in growth, and the compounding effect on earnings explain these multiples. Even in the scenario of a considerable deceleration in earnings growth, the stock should gradually grow into its valuation. While high expectations imply a thinner margin of safety, Intuitive has historically delivered to high standards.

Is ISRG Stock a Buy, According to Analysts?

Looking at Wall Street’s sentiment on the stock, Intuitive Surgical features a Moderate Buy consensus rating based on 14 Buys and six Holds assigned in the past three months. At $409.56, the average ISRG stock price target suggests 5.8% upside potential.

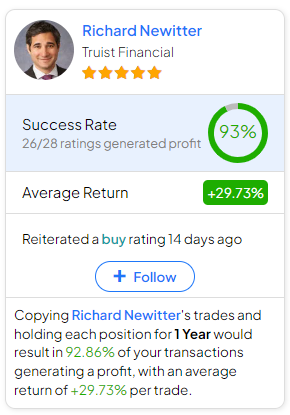

If you’re not sure which analyst you should follow if you want to buy and sell ISRG stock, the most accurate analyst covering the stock (on a one-year timeframe) is Richard Newitter from Truist Financial, with an average return of 29.73% per rating and a 93% success rate. Click on the image below to learn more.

The Takeaway

In conclusion, Intuitive Surgical’s stellar Q4 performance reflects its sustained leadership in the rapidly growing field of robotic surgery. With impressive revenue growth, expanding margins, and a solid global adoption trend, the company continues to ride a strong secular growth tailwind.

Despite concerns about its high valuation, Intuitive’s snowballing profits and financial soundness present a compelling investment case. As the industry evolves, the company’s dominant market position and ongoing growth acceleration suggest that there might be more room for the stock to flourish in the future.