It’s been 20 years since the famous dot-com bubble burst, and during that time, the internet economy has matured. Dot-coms are still with us, but in a more stable form. Some of the early online pioneers have grown into today’s corporate giants.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Wedbush analysts, in a report earlier this week, examined the recent history of internet stocks, highlighting their typical patterns and how they fit into recent events. According to the analysts, the usual cycle for internet stocks spans a decade, alternating between 2 low years for every 8 positive years. Noting that we’ve moved a year forward from the COVID pandemic era and the 2 down years prompted by lockdown policies, the analysts predict that there are between 5 and 7 upbeat years remaining in the current cycle.

The analysts also point out that e-commerce and advertising are currently experiencing their lowest growth rates in the post-COVID period. Nevertheless, there is an anticipation that the underlying secular growth trends supporting the industry will re-emerge in the forthcoming quarters.

“We anticipate global e-commerce growth to return to levels of around ~10% or more, and digital advertising to achieve a similar 10% to 12% range in the upcoming year. Furthermore, we expect AI to become a growth stimulant for consumer technology over the next 2 to 5 years,” the Wedbush team opined.

Against this backdrop, Wedbush’s Scott Devitt and Michael Pachter have labeled three internet giants as ‘buy’ recommendations. And they are not alone in showing confidence in these names. According to TipRanks, the world’s biggest database of analysts and research, these stocks are also rated as ‘Strong Buys’ by the analyst consensus. Let’s take a closer look.

Amazon (AMZN)

We’ll start with Amazon, the 800 pound gorilla in the world of eCommerce, and the world’s fourth largest publicly traded stock. Amazon has proved itself a lasting presence in the online world, having survived the original dot.com boom and evolving into today’s leader in online retail, with major forays into cloud computing and AI. The company is a leader in global retail, outside of China, and saw approximately $690 billion in gross merchandise volume last year.

Amazon’s operations include far more than just its core online retail business. The company has used its combination of deep pockets and tech expertise to develop new products based on generative AI, including an AI chatbot, an image building platform, and a software code development tool. The company’s cloud software services, AWS, realizes over $22 billion in annual revenues. And its brick-and-mortar fulfillment infrastructure, which supports the retail division, totals over 541 million square feet. In short, Amazon is too big and diverse be defined in one word, or even a short phrase.

But one figure can showcase Amazon’s size: $1.39 trillion, the company’s market cap, making it one of just five firms on Wall Street valued at more than $1 trillion.

Checking in with Amazon’s last quarterly results, from 2Q23, we find that the company beat the forecasts by wide margins. The top line figure, $134.4 billion in revenue, was up almost 11% year-over-year and beat the forecast by over $3 billion. The company’s North American segment, with $82.5 billion in revenue, was up 11% y/y, and its AWS segment grew 12% y/y to reach $22.1 billion.

At the bottom line, Amazon reported $6.7 billion in net income for the quarter, or 65 cents per diluted share. This was a strong turnaround from the 20-cent EPS loss reported in 2Q22 – and it was 31 cents per share better than expected.

Amazon’s strong overall position, its solid prospects for continued growth, form the core of the Wedbush view. The bank placed Amazon stock on its Best Ideas List, and analyst Michael Pachter wrote, “Amazon’s core business is now well positioned with an industry-leading fulfillment infrastructure… we believe Amazon is similarly well positioned over the next 18 months as AWS growth has stabilized and is poised to reaccelerate in 2H23 and into 2024, in addition to a strengthening digital advertising backdrop that should support continued growth in the company’s high-margin advertising business…. We view Amazon as our top pick across our coverage group…”

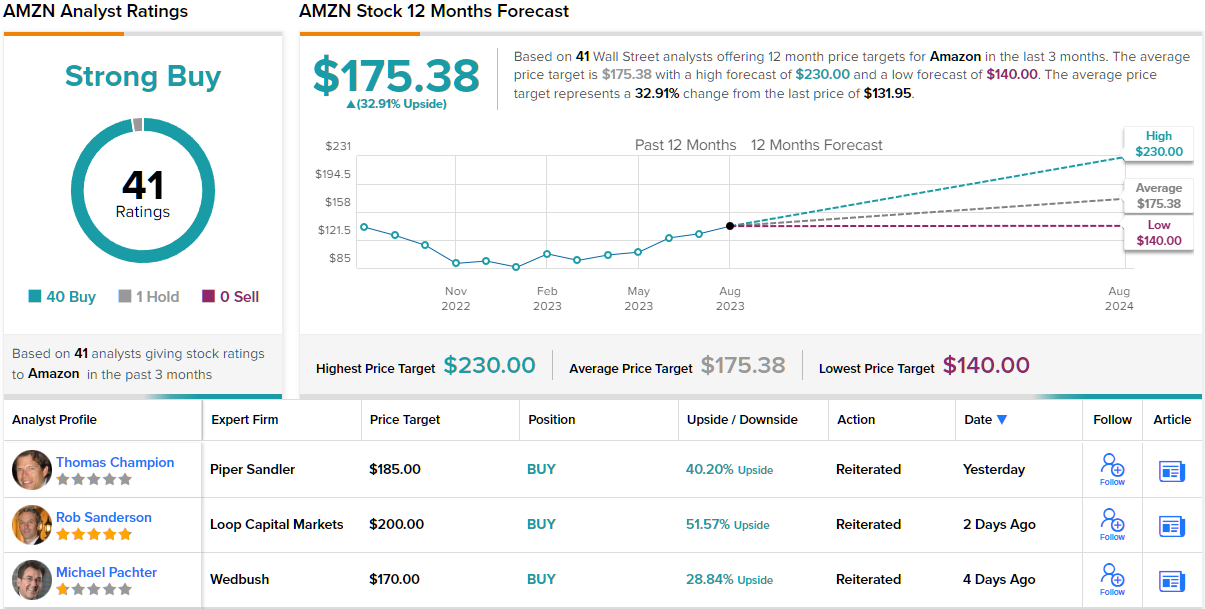

Pachter goes on to rate AMZN shares as Outperform (a Buy), and he sets his price target at $180 to imply a one-year upside potential of 34%. (To watch Pachter’s track record, click here.)

The Strong Buy consensus rating on AMZN is backed up by 41 recent analysts reviews – that feature a lopsided 40 to 1 split favoring Buy over Hold. The stock is selling for $132.12 and its $175.38 average price target indicates room for ~33% share appreciation in the year ahead. (See Amazon stock forecast)

Meta Platforms (META)

Next up is Meta, the parent company of Facebook. Meta is known for its suite of subsidiaries, including the flagship Facebook platform as well as WhatsApp, Messenger, and Instagram. The company revolutionized social media and online interpersonal interactions when it was founded back in 2004, but has been struggling in recent years, facing headwinds in the form of an aging core audience and a younger demographic that sees Facebook as ‘old.’

Meta has been working on various fronts to counter this effect. On the business side, the company dubbed these past 12 months as a ‘year of efficiency,’ in which it streamlined operations and cut more than 20,000 employees. At the same time, Meta launched Threads, a direct competitor to Twitter, and more recently has launched an AI translation model, an ‘all-in-one multimodal and multilingual’ AI called SeamlessM4T. The AI platform can reportedly handle speech-to-text, speech-to-speech, text-to-speech, and text-to-text translations for up to 100 languages, an important feature for a company with a wide global reach – and with social media platforms in scores of languages.

The company’s streamlining efforts and new products have been bearing fruit, as its share price and bottom line have both been rising in the past several quarters. Year-to-date, shares in META are up approximately 130%, far outpacing the NASDAQ’s 30% increase. And, in the last quarterly report, giving results for 2Q23, Meta reported earnings of $2.98 per diluted share, up 21% y/y and 9 cents per share ahead of the estimates.

These results were supported by top line revenues of $32 billion, a figure that was up 11% from the year-ago quarter. The company’s Q2 revenue was $969 million better than had been anticipated.

Meta leverages its audience to generate revenues, so the daily and monthly active user numbers are informative. On the daily metrics, the company saw 3.07 million daily active people (DAP) across all of its apps in June of this year, up 7% y/y. The monthly number was 3.88 billion, for a 6% y/y increase. Drilling down to the Facebook numbers, the company’s largest social media segment, we find the June 2023 daily active user number at 2.06 billion, up 5% annualized, and the monthly active users at 3.03 billion, for a 3% y/y increase. These numbers make Meta by far the world’s largest social media platform provider.

The combination of scale and results, combined with solid efforts at improving the latter, caught the eye of Wedbush’s Scott Devitt, who writes, “Meta has a proven history of driving user engagement across a variety of digital mediums and has consistently improved monetization despite temporary industry headwinds related to user privacy and data transparency…. Further, the company’s year of efficiency has seen significant cost reductions and a headcount reduction of over 20,000 employees in the last twelve months, creating a clear path to continued margin expansion as revenue growth resumes in earnest in 3Q…”

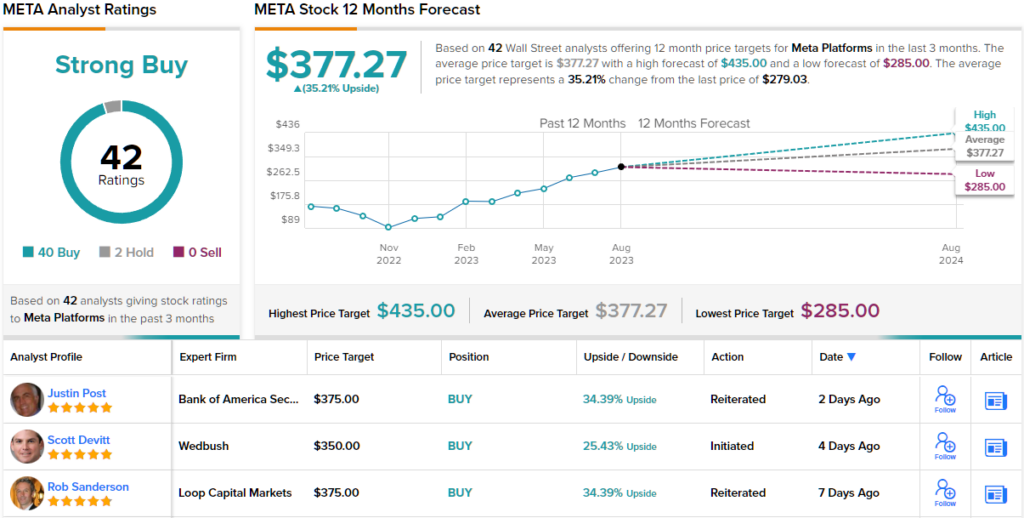

Devitt doesn’t stop with outlining upbeat prospects, he also gives the stock an Outperform (Buy) rating, and sets for it a $350 price target that indicates room for a 21% upside heading into next year. (To watch Devitt’s track record, click here.)

There’s no shortage of analyst reviews on the headline-generating tech giants, and META has picked up 42 such reviews from Wall Street. These include 40 Buys against 2 Holds, for a Strong Buy consensus rating. Shares are priced at $279.67, while the $377.27 average price target, slightly more bullish than Devitt’s, suggests that META will gain 35% on the one-year horizon. (See Meta stock forecast)

Alphabet, Inc. (GOOGL)

Last up on today’s list is Alphabet, another tech holding company – this one of the industry-leading Google search platform. Alphabet’s family of companies also includes such names as YouTube, the web’s largest video search and playback platform, and DeepMind, an AI research venture. Waymo is focused on autonomous vehicles, while Wing is developing a drone-based local air-freight delivery services. The new Bard platform, designed to directly challenge ChatGPT, is an AI-powered chatbot.

Google, however, is by far the company’s largest segment. The search engine dominates both the online search and advertising niches, and has even spawned a whole industry – search engine optimization – that has formalized the fierce competition to achieve high ‘google rankings.’ Google Services, taken together, generate some 89% of Alphabet’s total revenues; Google Search, alone, is responsible for 57% of the parent company’s bottom line.

The company’s total top line hit $74.6 billion for the second quarter of this year, the last quarter reported, beating the forecast by a solid $1.84 billion and increasing 7% over the previous year’s Q2. The company’s EPS number, $1.44 per share, was 10 cents ahead of expectations and up 19% y/y.

Alphabet’s sound financial results have pushed the stock price up this year, by about 44%. While this growth has not come near Meta’s, it has still overperformed when compared to the NASDAQ index. Alphabet is another of the market’s trillion-dollar companies, boasting a market cap of more than $1.6 trillion.

Checking in again with top analyst Devitt, we find him initiating Wedbush’s coverage of GOOGL with a positive view of the company’s potential to hold on to its industry-leading position for the long haul. Devitt says of the company and its stock, “We believe Google is a long -term winner within the digital advertising industry with broad exposure and durable market share of overall media spending. After reducing headcount earlier this year (~12,000 employees impacted) Google is well positioned to realize margin leverage in 2024 as revenue growth accelerates against an improving industry backdrop. Longer-term, there is significant optionality for Google across Cloud & AI, as the company experiments with AI experiences…”

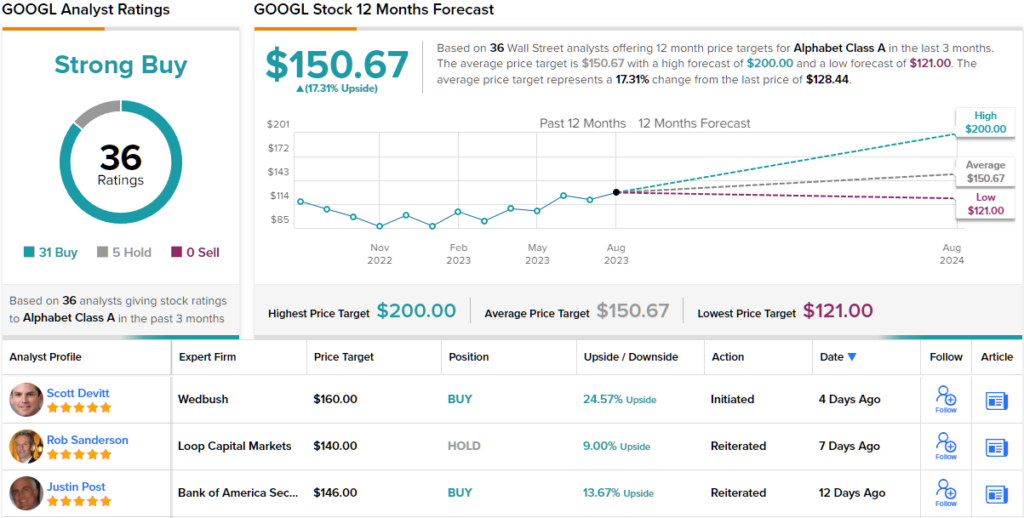

These comments support Devitt’s Outperform (Buy) rating, and his $160 price target points toward a one-year gain of 24.5% waiting for the stock in the next 12 months. (To watch Devitt’s track record, click here)

Of the 36 recent analyst reviews of GOOGL shares, 31 are to Buy and 5 to Hold – setting up the stock for a Strong Buy consensus rating. With a current trading price of $128.64 and an average price target of $150.67, Alphabet has a one-year upside potential of ~17%. (See Alphabet stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.