It looks like Intel (NASDAQ:INTC) investors will be heading off to the weekend in a good mood. The shares are pushing higher ahead of Friday’s session with the market applauding the chipmaker’s turnaround efforts following the release of its third-quarter results.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The company beat expectations on both the top and bottom line. Indicating a rebound in demand for its core x86 PC processors, revenue rose by 3.2% year-over-year to $13.7 billion, surpassing consensus by $560 million. Within that total, Data Center and AI revenue reached $4.12 billion, down 1% from the prior year but ahead of the $3.97 billion analysts had anticipated.

Adj. gross margin came in at 40%, topping the Street’s 36% forecast. The margin improvement was driven by higher revenue, a more favorable product mix, and reduced inventory reserves – helped by sales of previously written-down stock – partly offset by increased Lunar Lake volumes and the initial ramp-up of Intel 18A. The end result was adj. EPS of $0.23, $0.22 above Street expectations.

Looking ahead, Intel expects Q4 revenue of about $13.3 billion at the midpoint and adj. EPS of $0.08, roughly matching analysts’ expectations of $13.37 billion in revenue and $0.08 in EPS. The company noted that this outlook does not include the impact of its recent sale of the Altera subsidiary.

Scanning the results, Needham’s Quinn Bolton, an analyst ranked among the top 1% of stock experts on Wall Street, highlights several key takeaways. Product mix is expected to be the largest “swing factor” in future gross margin changes, as the company manages demand for its Lunar Lake and Arrow Lake products while reallocating older-node capacity to data center customers to better support its PC partners. Meanwhile, the absence of Altera is expected to create roughly a 1% headwind in 2026. Capacity is likely to remain tight, particularly in the Data Center and AI segment, where wafer supply will be prioritized but still fall short of overall demand. Additionally, the analyst points out the company has formed a new Central Engineering Group to spearhead its upcoming ASIC initiatives.

So, investors are evidently happy with the print, but Bolton’s overall conclusion in not quite as enthusiastic. “We continue to believe Intel’s turnaround will take time as the company is losing share in DC and is not yet competitive in AI. As valuation is rich, we remain Hold rated,” the 5-star analyst summed up. Bolton has no fixed price target in mind. (To watch Bolton’s track record, click here)

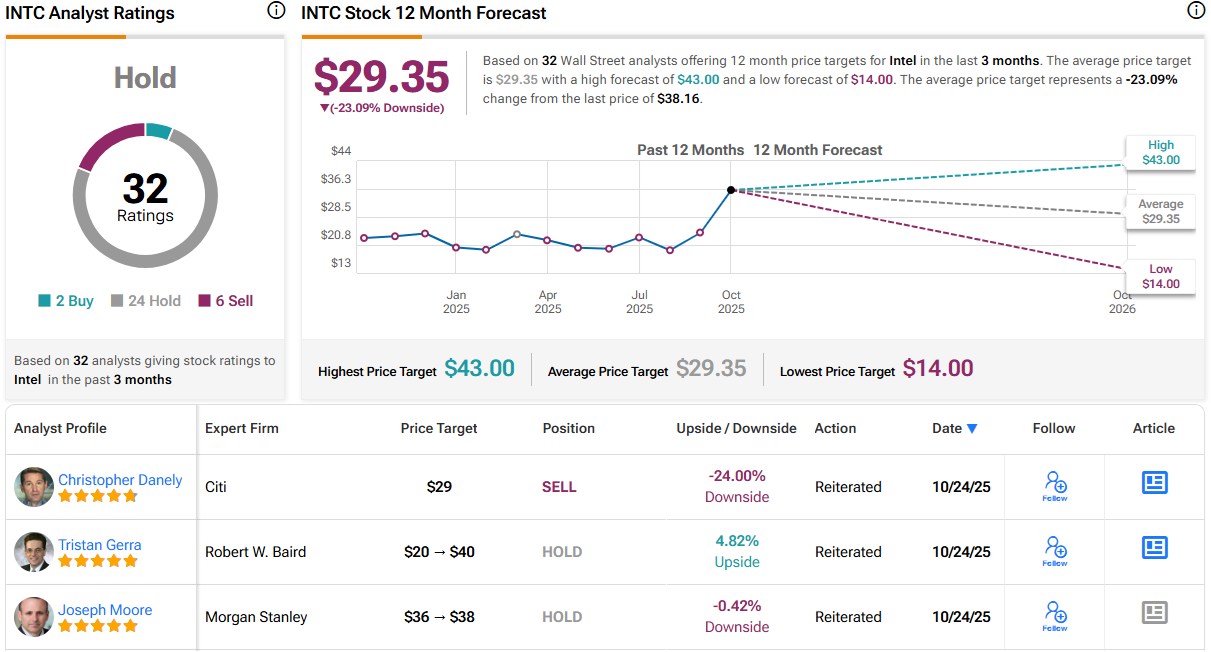

The Street, as a whole, does have one, and it concludes the shares are overvalued; at $29.35, the figure sits 23% below the current share price. Most analysts are also sitting this one out for now; the stock’s Hold consensus rating is based on 24 Holds, 6 Sells and 2 Buys. (See Intel stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.