Intel (NASDAQ:INTC) might still be a chipmaking giant, but its drastic dividend cut spells trouble for the company and its shareholders. I am bearish on Intel stock, even if it looks like a bargain, because the company’s reaffirmed earnings outlook is dismal, and Intel’s credibility appears to be compromised.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

California-based semiconductor manufacturer Intel is a textbook example of an iconic American business in decline. By this point, it’s no secret that Advanced Micro Devices (NASDAQ:AMD) is “eating Intel’s lunch,” meaning AMD is stealing crucial microprocessor market share from Intel.

This loss of market share, along with persistent softness in PC demand, weighed heavily on Intel’s dismal fourth-quarter 2022 financial results. Still, at least Intel’s loyal shareholders could count on the 5% annual dividend yield as a consolation prize – right? Unfortunately, that consolation prize just got slashed, and any perceived value in INTC stock might only be a value trap.

After Massive Dividend Cut, Intel’s Credibility is at Stake

Intel stock got clobbered in 2022, but the company’s investors could take comfort in the thought that Intel paid a 5%-ish annual dividend yield. That’s a generous yield for a technology mega-cap company, and Intel’s consistent dividend payout history may have provided a false sense of security.

Besides, in late January, Intel CEO Pat Gelsinger assured anxious income-focused investors, “We are committed to the dividend and to a very healthy and competitive dividend.” Just to drive the point home, Gelsinger reiterated that Intel remains “committed to rewarding our shareholders with the dividend.”

Frankly, Gelsinger shouldn’t have made those assurances, as Intel can’t afford to maintain a 5% dividend while the PC market is weak. Just to provide a not-so-refreshing refresher, in Q4 2022, Intel’s GAAP-measured revenue declined 32% year-over-year. Also, Intel’s gross margin dropped by 14.5%, and the company swung from $4.6 billion in net income to a $0.7 net loss.

It’s fair to say that a dividend cut was inevitable. Is it possible that everyone except Gelsinger saw the writing on the wall? More likely, Gelsinger knew full well what was coming but wasn’t willing to hint at a dividend reduction. If that’s the case, then the chief executive should have just stayed mum on the topic instead of gushing about Intel’s “competitive dividend.”

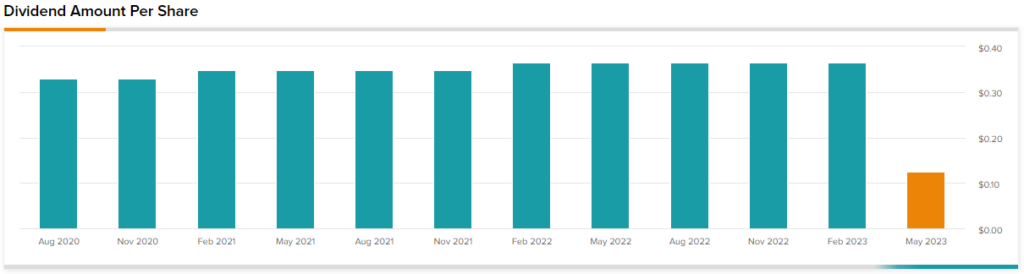

So, it was particularly disappointing to learn that Intel officially “reset its dividend policy” just a few weeks after Gelsinger’s seemingly enthusiastic declarations. Stunningly, Intel chopped its quarterly dividend payment from $0.365 to just $0.125 per share, representing a 66% reduction.

Intel Reaffirmed Its Dismal Outlook

As if to add insult to injury, Intel’s press release also included an announcement that the company is reaffirming its first-quarter 2023 financial outlook. Suffice it to say, the outlook wasn’t optimistic the first time around and isn’t any more comforting now.

Here are the essential figures. For Q1 2023, Intel expects to generate revenue of $10.5 billion to $11.5 billion, which is below the $14 billion that Wall Street had modeled when Intel released its fourth-quarter 2022 results. In addition, Intel envisions a non-GAAP gross margin of 39% for 2023’s first quarter, whereas analysts envisioned that Intel’s quarterly margin would exceed 45.5%.

Perhaps worst of all, Intel restated its forecast that the company would post an $0.80 per-share loss for the current quarter. If the company continues to report losses, Intel might not even have a 12-month trailing P/E ratio anymore – because, after all, there’s no “P/E” without the “E” (earnings).

Granted, it’s possible to take a glass-half-full view of Intel’s situation. Bernstein analyst Stacy Rasgon pointed out the positive side of Intel’s drastic dividend cut, stating, “They have now gotten the cut out of the way, potentially removing at least one of their many overhangs.”

Fair enough, and as INTC stock slips to the $25 area, this might entice some eager contrarians. Yet, financial traders should bear in mind that some investors will bail on Intel because of the yield drop, and this could put negative pressure on the share price. As Ragson put it, Intel’s dividend chop job “removes one of the last reasons for long-suffering investors to own the stock.”

Is INTC Stock a Buy, According to Analysts?

Turning to Wall Street, INTC stock is a Hold based on three Buys, 18 Holds, and seven Sell ratings. The average Intel stock price target is $27.20, implying 7.4% upside potential.

Conclusion: Should You Consider Intel Stock?

It would have been easier to tolerate Intel’s steep dividend cut if Gelsinger hadn’t declared Intel’s commitment to “a very healthy and competitive dividend” just a few weeks earlier. It’s a shame, really, that both Intel’s yield and credibility are compromised now.

What’s left now is a struggling chipmaker with poor prospects and a lackluster outlook amid a soft PC market. Sadly, the mighty Intel has fallen fast, and unless conditions improve, investors shouldn’t consider INTC stock for “competitive” yield, share-price appreciation, or anything else that would make a long position worthwhile.