For investors seeking a clear path in the markets, a signal that cuts through all the noise and identifies stocks likely to gain, corporate insiders cannot be ignored.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

We’re referring to corporate officers who hold high posts of responsibility within their firms: CEOs, COOs, CFOs, Exec VPs, and members of the Board. These positions provide them with two undeniable attributes: a macro-view of the company and its prospects, and a need to answer to shareholders and directors for company performance.

In essence, corporate insiders do not take stock trades in their own companies lightly. Their actions undergo scrutiny from within the organization, as well as from federal regulators who require public reporting of their trades.

Investors can look to these moves, using TipRanks’ Insiders Hot Stocks tool. We’ve used that tool to do just that, find two stocks that have seen recent insiders buys – into the millions of dollars. When insiders make buys of that magnitude, it’s best to pay attention.

In fact, it’s not just the insiders who believe that now is the opportune time to load up on these equities. According to the analyst consensus, both stocks are rated as ‘Strong Buys’ and offer solid upside potential for the upcoming year. Let’s take a closer look.

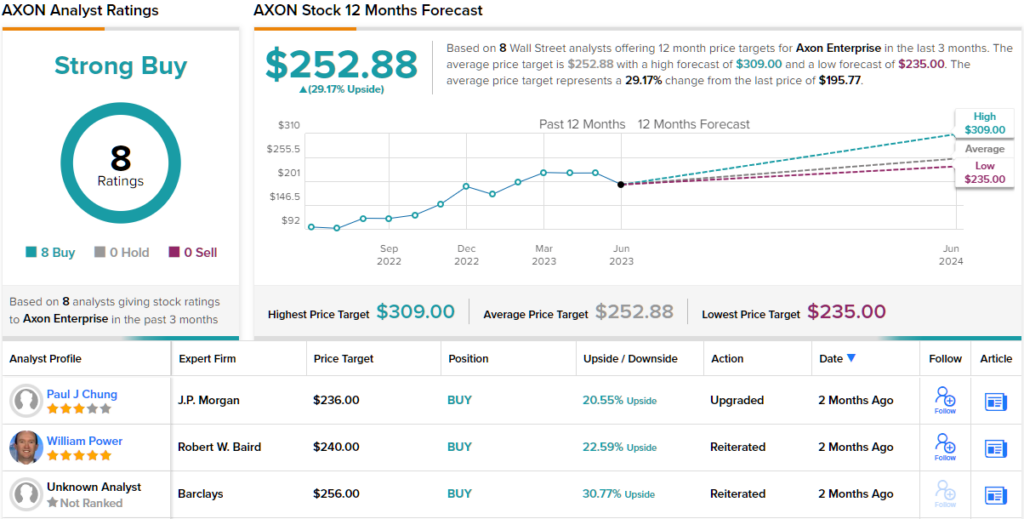

AXON Enterprise (AXON)

First up is a company that many of us would recognize by its original name, Taser. AXON Enterprise, based in Arizona, is a technology company geared toward the law enforcement and military markets. The company’s first product was the less-than-lethal Taser stunning weapon. In 2017, the company changed its name from Taser to AXON to reflect its wider product line, and today AXON’s catalogue features a variety of devices, from body and car cameras to drones and remote signals, plus a full range of control and monitoring software, in addition to its line of Taser energy weapons.

While law enforcement has faced serious social and political pressures in recent years, AXON aims to improve that image. Among the company’s goal for the next 10 years is to reduce gun-related deaths between the police and the public by 50%. This is a lofty ambition – but less-lethal weapons, the key line among AXON’s products, offer alternatives to firearms, and body and dash cameras are honest tools for keeping police accountable.

AXON has followed that path to a strong financial performance. In Q1 of this year, the company reported several solid metrics: cloud revenue in the software segment of $116 million, up 51% year-over-year; annual recurring revenue of $520 million, up 49%; and a full-year revenue outlook for 2023 predicting 22% growth. Total revenue in Q1 was $343 million, a company quarterly record. That figure was up 34% y/y and beat the forecasts by $23.3 million. At the bottom line, AXON reported a non-GAAP earnings per share of 88 cents, 34 cents better than had been expected.

Looking at insider activity, we discover a notable buy made by Hadi Partovi, a member of the Board of Directors, earlier this week. He acquired 25,000 shares of AXON, investing $4.77 million in the purchase. Notably, this purchase adds to Partovi’s previous transaction in May when he acquired 10,000 AXON shares for $1.9 million.

That’s certainly a display of confidence, but it’s not the only one. Barclays analyst Manoj Shivdasani notes the company’s successful product line as the main narrative for his bullish stance

“AXON has demonstrated strong innovation capabilities in the public safety solutions market… AXON’s TASER (45% of FY22 revenue), along with the expanding Software and Sensors segment (55%), contributes to Axon’s robust revenue (28.2% 5Y CAGR) stream. With the installed base for both TASER and cameras continuing to grow, along with expanding software solutions, and International expansion opportunities, AXON has a flywheel of opportunities ($50bn TAM) across the business,” Shivdasani opined.

Put into simple terms, this adds up to an Overweight (i.e. Buy) rating from the analyst, whose price target of $256 implies a one-year upside potential of ~31%.

Overall, the view from the Street is unanimously positive on this stock, with 8 recommendations giving AXON a Strong Buy consensus rating. The shares are priced at $195.77, and their $252.88 average price target suggests an upside of 29% out to the one-year horizon. (See AXON stock forecast)

Clene, Inc. (CLNN)

Next on our list is Clene, a unique biotech firm researching new treatments for neurodegenerative diseases, conditions such as amyotrophic lateral sclerosis (ALS), multiple sclerosis (MS), and Parkinson’s disease (PD). While these names are all well-known to the public, that is not due to ease of treatment. Clene is targeting disease conditions that are severe, chronic, and have high unmet medical needs.

The company is working to meet those needs through an innovative approach, in its own words, ‘utilizing a patented electro-crystal-chemistry process that results in highly-faceted, clean-surfaced nanocrystals of pure transition elements.’ These nanotherapeutics are catalytically active, and once inside the patient’s cells, will support thousands of energy-supportive electrons per second per nanocrystal. The company’s leading drug candidate, the gold nanocrystal suspension CNM-Au8, is the subject of three separate clinical research tracks, in the treatment of ALS, MS, and PD.

Clene has several additional nanotherapeutics under development, based on zinc-silver and gold-platinum combinations, but only CNM-Au8 is in the clinic. In recent weeks, Clene has released several updates on the progress of those clinical trials.

During Q1, the company announced data showing a 60% survival benefit due to CNM-Au8 in the RESCUE-ALS trial with patients in early-to-mid stage ALS. The drug candidate also showed a survival benefit higher than 90% for patients with mid-to-late stage ALS in the HEALEY ALS platform trial. Earlier this month, Clene published data from the RESCUE-ALS trial in the Lancet, a peer-reviewed medical journal.

On the MS track, Clene’s CNM-Au8 shown several important results in clinical testing, including a positive safety and toleration profile but also axonal integrity and white matter integrity; white matter integrity particularly is associated with reductions in cognitive and functional decline in MS.

In terms of catalysts, coming up, Clene will be meeting with FDA regulators for end-of-Phase-2 meetings regarding the CNM-Au8 clinical research in the treatment of both ALS and MS. In particular, the company’s meetings will focus on regulatory paths forward for the drug candidate. The discussions will include a detailed look at the full data set from the CNM-Au8 trials, and will include the full NfL biomarker data, in addition to survival rates in the ALS trials.

When we look at the insider trades on CLNN, two pop out right away. Each was made by a company director, and each was well over $1 million. David Matlin bought 1.5 million shares for $1.2 million last week, while Alison Mosca spent $1.915 million to pick up more than 2.394 million shares.

Weighing in from Canaccord Genuity, analyst Sumant Kulkarni describes plenty of room for optimism on this company’s pipeline, despite its highly speculative nature. He draws specific attention to the upcoming regulatory meeting and its likely focus on biomarker data, writing, “CLNN plans to meet with the FDA in 3Q23 in an end-of-Phase 2 meeting. We now eagerly await the outcome of this meeting and note CLNN is even exploring the possibility of filing a new drug application (NDA) on the strength of the data it already has in hand. We also note that the unmet need in ALS remains very high, and the FDA’s interactions with sponsors of other products (BIIB/IONS, AMLX and BCLI) take this variable into consideration. On the stock, with the company now better capitalized, our thesis remains the same in that, at the current price, we believe outcomes of interactions with the FDA and additional biomarker/survival data have the potential to drive more absolute upside on the stock vs. downside.”

For Kulkarni, this makes for a stock with substantial upside. He rates CLNN shares a Buy, and his $5 price target indicates his confidence in a 538% gain over the next 12 months. (To watch Kulkarni’s track record, click here)

This is another stock with a unanimous Strong Buy consensus, this one based on 5 recent positive reviews from the Street’s analysts. The stock’s average price target of $5.4, even more bullish than Kulkarni’s, suggests a robust upside potential of ~589% from the current share price of $0.78. (See CLNN stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.