Trying to navigate the ups and downs of the stock market and predict its future direction can seem like a complicated and daunting task. But as with almost anything, keeping it simple is often the key. And one of the most straight forward strategies is to keep an eye out for the insiders’ moves.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

After all, these corporate officers are privy to their companies’ inner workings. So, when an insider is seen picking up shares of the company they work for, especially in bulk, it sends a clear signal that they believe the time is right for loading up.

To keep the playing field level, those in the know are required to make their purchases public and TipRanks’ Insiders’ Hot Stocks tool offers a way to follow all the latest insider transactions.

Against this backdrop, we’ve delved into the platform to get the lowdown on a pair of stocks that insiders have been investing heavily in recently. They have poured millions into these names, and to add to the appeal, both stocks are rated as Strong Buys by the analyst consensus, and offer significant upside potential. Now, let’s take a closer look.

Morphic Holding (MORF)

For our first insider-backed name, let’s head to the healthcare sector. Morphic is a biotech firm that focuses on developing transformative therapies for patients with serious diseases. The company’s MInT technology platform uses “integrin biology” to develop drug candidates that target integrins, which are proteins found on the surface of cells that play a key role in many disease processes.

Integrin-based drugs have the potential to treat a wide range of diseases, including fibrosis, autoimmune disorders, and cancer. Spearheading this research, the company’s lead candidate is MORF-057, an α4β7-inhibitor that has recently been making waves.

Morphic recently released topline results from the main cohort of the open-label Phase 2a EMERALD-1 study, which investigated MORF-057 in adult patients with moderate to severe ulcerative colitis (UC). The drug met its primary endpoint: following 12 weeks of treatment, the oral therapy showed a statistically significant drop from the baseline in the Robarts Histopathology Index (RHI), a clinical measure that assesses the disease’s actions.

The drug’s potential has been behind the stock’s year-to-date outperformance, with the shares having already gained 106% since the onset of 2023.

Nevertheless, Morphic’s founder, Timothy Springer, must believe the shares are still undervalued. He just loaded up on 1,050,000 of them at a price of $45 each. These are now worth $57.8 million. In all, his total MORF holdings stand at 2,768,464 ($152.4 million).

Mirroring that confident take, BMO analyst Evan Seigerman highlights MORF-057’s potential, especially when pitted against a rival offering.

“Given the strength of the data, MORF-057 presents a competitive alternative to Entyvio,” Seigerman opined. “Notably, Takeda guides peak Entyvio revenues to $7.5-$9B, which includes previous projection of $5.5-$6.5B for IV-only + $2B-$2.5B for subQ, if approved after 1H24 filing… We now assume a 70% probability of success for MORF-057 (previously 50%) in ulcerative colitis… We are also increasing PoS for Crohn’s disease to 30% (20% previously), given precedent set by Entyvio across IBD.”

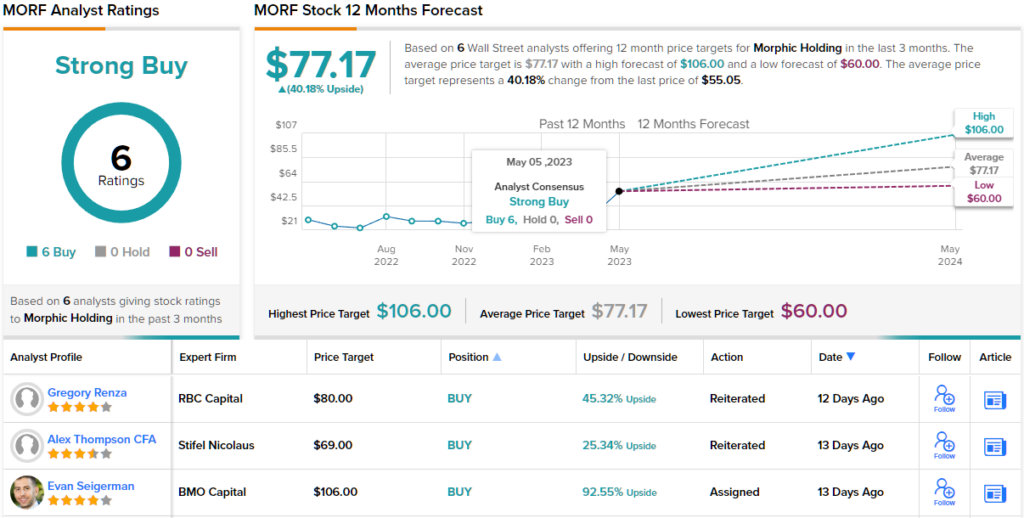

These comments form the basis for Seigerman’s Outperform (i.e., Buy) rating while his $106 price target makes room for additional gains of a handsome 92%. (To watch Seigerman’s track record, click here)

There’s no argument with that take amongst Seigerman’s colleagues; all recent reviews – 6, in total – are positive, naturally providing the stock with a Strong Buy consensus rating. At $77.17, the average target suggests shares will climb 40% higher in the months ahead. (See MORF stock forecast)

Impinj, Inc. (PI)

Next on our insider-backed list is Impinj, a leading provider of RAIN RFID (Radio Frequency Identification) solutions. These enable businesses to track, identify, and locate items in real-time. Impinj’s RAIN RFID products are used in a wide range of industries such as retail, healthcare, manufacturing, and logistics, amongst others.

Essentially, using IMPINJ’s platform, customers can create wireless connectivity between everyday items, what is called the Internet of Things (IoT). Via Impinj’s RAIN RFID tech, businesses can gain visibility into their operations and the supply chain, leading to improved efficiency, reduced costs, and a better customer experience.

Companies obviously find the solutions compelling in the modern world, given Impinj has been showing consistent sequential growth for the past 7 quarters, including in the recently reported quarter – for Q1. Revenue rose by 61.6% year-over-year to $85.9 million, while beating the Street’s call by $2.31 million. However, adj. EPS of $0.30 fell short of the $0.33 expected by the analysts.

While the company expects growth to continue in Q2, the anticipated revenue haul missed Street expectations, coming in the range between $84 million and $87 million, compared to consensus at $88.29 million. Likewise, adj. EPS is expected to hit the $0.28 to $0.33 range, below the $0.41 Street forecast.

The shares fell badly in the wake of the results’ announcement, crashing by 39% in the subsequent session.

Obviously one insider thinks the time is right to pounce. Director Steve Sanghi recently purchased 23,500 PI shares, currently worth over $2 million. His total holdings now stand at 40,200, worth $3.51 million.

The disappointing Q2 outlook has done little to dampen Canaccord analyst Michael Walkley’s bullish take.

“Despite weaker than anticipated Q2 guidance, we remain confident in our long-term thesis for growth opportunities for RAIN RFID adoption with strong growth potential across retail, supply chain and logistics, auto, aviation, healthcare and other large markets. While supply constraints could limit upside in the near term, we anticipate supply improving followed by sustained strong long-term growth trends,” the 5-star analyst opined.

“Given the strong pipeline and backlog, the pace of improving supply could result in upside to our reduced 2023 estimates. With Impinj’s product leadership, end-to-end solutions, and strong growth opportunities, the company is investing during these uncertain times to increase market share and drive profitable long-term revenue growth,” Walkley went on to add.

Quantifying this bullish stance, Walkley rates PI shares a Buy along with a $140 price target. There’s plenty of upside – 60% to be exact – should the target be met over the next 12 months (To watch Walkley’s track record, click here)

Overall, 7 analysts have chimed in with PI reviews over the past 3 months and all are positive, providing the stock with a Strong Buy consensus rating. The forecast calls for 12-month returns of 53%, considering the average target stands at $134. (See PI stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.