There are few market signals that are clearer than those given by insiders’ stock purchases. To correctly interpret these signals, we need only understand two things. First, that insiders are simply top-flight corporate officers, CEOs, CFOs, COOs, Board members, and the like; and second, that the only reason they have for buying shares in their own companies is that they believe the shares will gain in value sooner rather than later.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

And when the insiders start pouring millions of their own money into these stocks, that just magnifies the signal.

Because these corporate officers have access to the deeper workings of their companies, along with advanced knowledge of company issues that will impact stock values – earnings reports, sales performance, personnel turnovers, regulatory matters, and the like – federal watchdogs require that they keep the playing field level by publishing their stock trades. For the retail investor, those published trades provide a solid marker pointing out interesting stock buys.

We can follow them using the Insiders’ Hot Stocks tool at TipRanks. This data tool gathers up-to-date info on insider action and makes it available to the public, where it can inform our own trades.

In fact, we’ve used that tool to pinpoint two stocks with recent insider buying activity totaling over $13 million. Adding to the good news, each has a ‘Strong Buy’ consensus rating from the Street’s analysts. Let’s take a closer look.

Shift4 Payments (FOUR)

We’ll start in the world of payment processing, an important niche in today’s digital economy. Shift4 Payments is a Pennsylvania-based tech firm that offers payment solutions for online commerce. Processing is part of this, but Shift4’s services also include online security, mobile and contactless tech applications, point-of-sale interfaces and solutions, and business intelligence and analytics. The company tailors its services to match the customer’s needs across a wide range of industries: retail, non-profits, sports & entertainment, travel & hospitality.

With 25 years of experience behind it, Shift4 Payments has learned that the key point is simplicity, and it aims to make its solutions easy and intuitive for the end user. The company has over 200,000 customers on the books and processes over 5 billion transactions annually worth more than $260 billion. The company operates in the US and Canada, much of Europe, and in Japan.

When we look at Shift4’s recent financial performance, we find that reported revenues have been on an upward trajectory for the past several quarters. That said, while in the last reported quarter, 1Q24, the top line came to $707.4 million, for a 29% year-over-year gain, the figure missed the forecast by $43.6 million. At the bottom line, the company reported a 31-cent EPS, also falling shy of the consensus estimate – by 5 cents.

In total, FOUR shares have lost ground this year, slipping about 10% in 2024. Meanwhile, there appears to have been some significant insider buying of these shares recently. Those transactions come from Jared Isaacman, the company CEO. Isaacman, in the last couple of weeks, made two ‘informative buys’ of FOUR stock, totaling 125,051 shares, for which he paid nearly $8.3 million. Isaacman’s current stake in Shift4 Payments is worth almost $42.5 million.

Despite the recent misses Evercore analyst David Togut remains upbeat on Shift4’s prospects, seeing the company in a solid position to continue generating growth.

“We remain constructive on FOUR given multiple opportunities to drive superior net revenue growth and margin expansion led by rising adoption of Skytab; competitive pricing; increasing presence across core verticals like restaurants, gaming, sports & entertainment; international expansion; and cost measures,” Togut said. “Trimming our 2024E adjusted EBITDA by $20 million to $660 million on a slightly lower revenue forecast and 2025E Adjusted EBITDA by $10 million to $840 million on modestly reduced margin expectations. Keeping 2026E Adjusted EBITDA estimate unchanged at $1.02 billion… Sticking with Outperform Rating and #4 Top Pick.”

Togut complements his Outperform (i.e. Buy) rating with a price target of $100, implying a robust one-year upside potential of 49%. (To watch Togut’s track record, click here)

Overall, Shift4’s Strong Buy consensus rating is based on 17 recent analyst recommendations, including 14 to Buy and 3 to Hold. The shares are priced at $67.01, and their $84.56 average price target suggests a gain of 26% on the 12-month horizon. (See Shift4 stock forecast)

Allogene Therapeutics (ALLO)

From payment tech we’ll move over to biotech. Allogene is working to shake up the biotherapeutic industry, specifically in the CAR T realm, by changing the way that commercial-quality genetically engineered allogenic T cell therapies are developed for oncological uses. The company aims to create a new line of ‘off the shelf’ CAR T therapeutic candidates, to make effective, reliable cell therapies more readily available for delivery to patients.

To this end, the company’s lead candidate, cemacabtagene ansegedleucel, known as cema-cel (formerly called ALLO-501A), is the subject of several human clinical trials, with initial data from the ongoing Phase 1 R/R CLL (chronic lymphocytic leukemia) trial expected for release by the end of this year.

Importantly, Allogene recently expanded its CD19 oncology rights (the program target toward which it is investigating cema-cel) to the UK and all member states of the EU. This expansion of the territory rights brings a substantial increase in the target market opportunity for the cema-cel program, to more than $9.5 billion in the combined US, EU, and UK. The consolidation of rights also provides increased flexibility for the company to develop an expanded commercial footprint through future cema-cel partnerships.

Also of note to investors, Allogene recently engaged in an important fundraising move, putting a large tranche of shares on the public market. The company offered over 37.9 million shares at $2.90 each, expecting to raise approximately $110 million in gross proceeds from the sale.

We should note that, prior to the stock offering, Allogene reported having $397.3 million worth of cash and other liquid assets on hand. That was considered enough to fund operations into 2026. In light of the firm’s strong cash holdings, and its recent successful sale of stock, we should also note that Allogene retains rights for further expansion of the CD19 oncology program, the cema-cel trials. These rights include expansion into Japan and China at no additional cost to Allogene, provided the company can demonstrate that it has the resources to pursue those markets.

Those are all key points in the background behind Board member Arie Belldegrun’s purchase of 1,724,137 shares for almost exactly $5 million earlier this month. This insider trade is marked as an ‘informative buy,’ meaning investors should pay it close attention. Belldegrun currently holds over $25 million worth of Allogene shares.

This cash-rich biotech has caught the eye of Truist analyst Asthika Goonewardene, who is careful to note both the cema-cel rights expansion and the stock sale: “Two key positives from 1Q24 should make the stock more attractive, in our view: (1) Gaining EU/UK rights to lead asset Cema-cel puts ALLO more firmly in the driver’s seat and positions the company to retain more of the profit, and (2) We think the $110M financing means ALLO’s total cash (~$500M) will comfortably see it past more potential value inflection points, alleviating cash runway concerns and making the stock more investable.”

The analyst goes to further explain his upbeat stance on the company, saying, “While ALLO has work to do in redefining the treatment paradigm for aggressive lymphoma, and making community practices handle their product, history gives us confidence in the team’s ability to execute.”

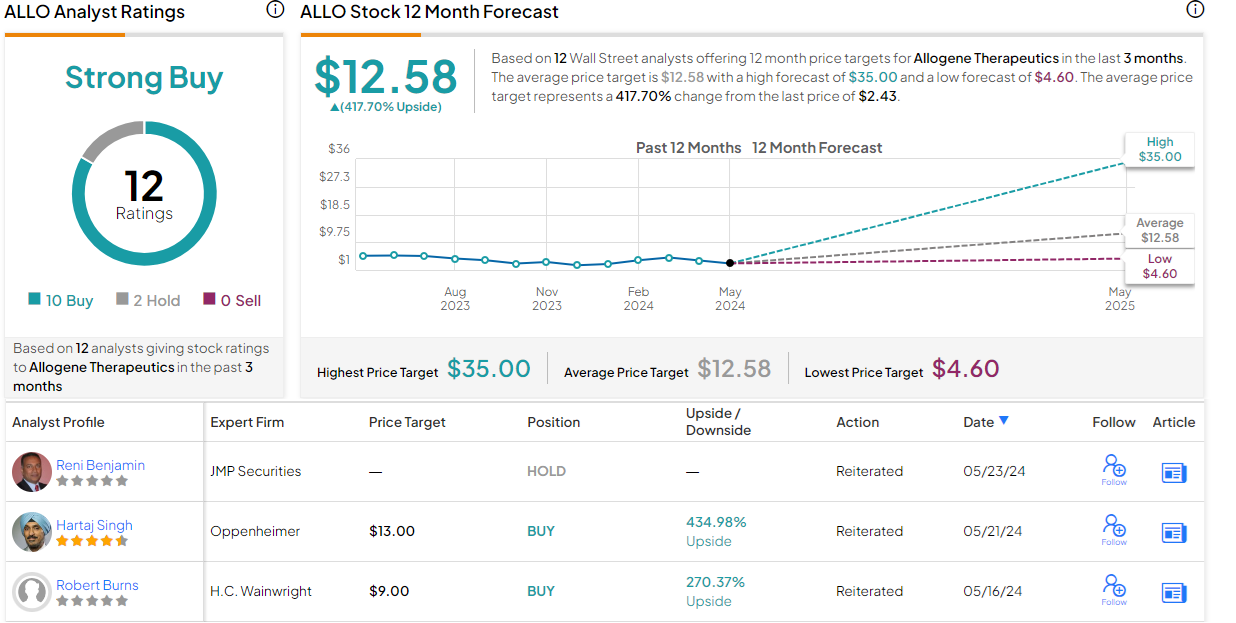

Goonewardene rates these shares as a Buy, and his price target, $17, indicates a huge upside potential of ~600% in the coming year. (To watch Goonewardene’s track record, click here)

That’s bullish, but not that out of line. The overall Street view also suggests high potential here, and the Strong Buy consensus is based on 10 Buy and 2 Hold recommendations. The stock is selling for just $2.43 and has an average price target of $12.58, pointing toward a 418% upside by this time next year. (See ALLO stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.