Legendary investor Peter Lynch has a straightforward perspective on corporate insiders and their actions in the stock market. He put it simply: insiders may sell shares for a range of reasons, but they only buy shares when they believe the price is going to rise.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Keeping a close watch on insiders’ stock purchases can prove to be a profitable investment strategy. Corporate insiders, which include company officers and board members, possess valuable knowledge about company policies and performance that can influence stock prices. They can utilize this information to make informed decisions when purchasing stocks, but they are required by law to publicly disclose their own stock holdings. This transparency allows the general public to gain insights from these purchases.

Bearing this in mind, we used the Insiders’ Hot Stocks tool from TipRanks to point us in the direction of two stocks flashing signs of strong insider buying that warrant a closer look. From an investor’s perspective, each of these stocks has an important feature in common: high dividends, which make them desirable as sources of income. We’re talking about at least 8% dividend yield here. Let’s dive in, and check out the details.

Plains GP Holdings (PAGP)

We’ll start in the oil industry, where Plains GP Holdings owns a controlling general interest, as well as an indirect limited partner interest, in Plains All American (PAA). PAA is a major midstream firm that transports crude oil and natural gas within the US hydrocarbon transport network. Through its ownership stakes in the company, Plains GP offers investors an alternative means of accessing the revenue stream generated by this network.

The underlying asset network behind Plains GP extends across North America, from the Northern Great Plains of the Dakotas, Montana, and Saskatchewan to the Rockies of Alberta down through Wyoming and Colorado, and into the plains and Gulf Coast of Kansas, Oklahoma, Texas, and Louisiana. The network has extensions into New Mexico and into the Mississippi River Valley, and additional facilities are located in the Great Lakes region, California, Arizona, Florida, and the Chesapeake Bay. In short, Plains can handle more than 6 million barrels per day of crude oil and natural gas products in its transportation network, making the $30 billion-plus company one of the largest midstream operators on the North American continent.

Shifting our focus to the financial figures, we discover that PAGP posted $12.34 billion in revenue for 1Q23. This marks a nearly 10% decline compared to the previous year and falls short of the Street’s forecast by $500 million. On a positive note, the company’s bottom line earnings, reported as a GAAP EPS of 35 cents per common share, more than tripled year-over-year and exceeded the forecast by 8 cents. The company’s free cash flow, which stood at $200 million in the year-ago quarter, experienced a significant boost, reaching $823 million. Even after distributions, PAGP still retains $581 million in free cash.

The distribution, or dividend, here is substantial. In April, the company declared its Q1 payment as 26.75 cents per common share, or $1.07 annualized. At that rate, the dividend yields 8%, a solid return. Investors should also note that PAGP has been keeping up reliable dividend payments going back to 2014.

PAGP shares have shown a steady upward trajectory, with a 10% increase year-to-date. Bolstering investor confidence, a prominent company insider, Willie Chiang, who holds the positions of Chairman and CEO, has made a noteworthy purchase of PAGP shares. Earlier this week, Chiang spent more than $993K picking up 75,000 shares of the stock.

From the Street’s analysts, we can check in with 5-star analyst Justin Jenkins, of Raymond James, who writes of PAGP: [We] think sentiment has finally started to turn positive on Plains — propelling it to be one of only a few of our names in the green YTD. We expect this to continue as the risk/reward from here still seems quite favorable…. With OPEC+’s surprise cut in effect, we think oil is nearer a floor, especially as demand concerns screen as overblown. Management expects Permian production to increase by +/- 500 kbpd in 2023, and we’d agree. Although slower than prior cycle growth, this still equates to solid operating leverage, especially as [Plains] increasingly captures more Permian takeaway volume.”

Taking those comments forward, Jenkins rates the shares as a Strong Buy, and his $17 price target implies a one-year upside potential of 29%. Based on the current dividend yield and the expected price appreciation, the stock has 37% potential total return profile. (To watch Jenkins’ track record, click here)

Overall, Wall Street has given a Moderate Buy consensus rating to this stock, based on 5 recent analyst reviews that include 3 Buys and 2 Holds. The shares are selling for $13.17, and their $16.80 average price target suggests a gain of ~28% over the next 12 months. (See PAGP stock forecast)

Black Stone Minerals (BSM)

Another dividend stock backed by insiders is Black Stone, a limited partnership that specializes in mineral rights. Black Stone generates income through royalties from its valuable land holdings in lucrative oil and gas production basins. The company owns over 20 million acres across more than 40 states and boasts a portfolio of approximately 60 production regions. Black Stone’s presence is particularly prominent in the states of North and South Dakota, Mississippi, Alabama, Texas, and Arkansas.

Overall, this company’s royalty position represents the combined efforts of geologists, technical engineers, land and business developers, and investment experts, who provide the know-how to turn land holdings into wealth. Black Stone benefits from the scale of its holdings, both in size and geographical extent, and has remained profitable despite the worsening in current economic conditions.

The difficult economy was visible in the company’s lower rig count. Black Stone had 78 active rigs on its holdings as of March 31, 2023. This was down from the peak of 108 at the end of 2022, and reflected a response to lower natural gas prices.

The firm’s overall profitability has been visible in the recent financial results, however. Last year, Black Stone saw revenues of $663.6 million, representing an impressive 85% year-over-year increase from the $359.3 million reported for 2021. In the most recent quarter, 1Q23, the company had a top line of $174.5 million in total revenues, which included $118.3 million in oil and gas revenue. While the oil and gas revenue was down 22% y/y, the total revenue showed a marked gain; in the year-ago quarter, the top line total came to just $36.4 million.

At the bottom line, the diluted EPS was reported at 60 cents. This was up from a 6-cent loss in 1Q22, and beat the forecast by 15 cents, or 33%.

Of particular interest to dividend investors, Black Stone reported a distributable income of $104.1 million in 1Q23. While down 17% y/y, this was sufficient to maintain the dividend, which was declared in April for a May 19 payout. The dividend, of 47.5 cents per common share, gives an impressive yield of 12.5% based on an annualized payment of $1.90.

The most recent insider buy here has come from Black Stone’s CEO, Thomas Carter. Carter, who is also Chairman of the Board, last week spent $494,000 to buy up 31,800 shares of BSM.

This stock has also caught the attention of Jones Research analyst Eduardo Seda, who writes of the company: “Development activity remained healthy across BSM’s acreage, benefiting from organic growth efforts and new drilling activity. However, weakness in the current commodity price environment has caused some challenges and rig count has declined slightly to 78 rigs across BSM’s acreage from 108 at year-end 2022. Yet permitting activity has remained in-line with 4Q22 with over 400 horizontal permits added to BSM’s acreage. Overall, with continued development activity across its acreage, despite a softening commodity price environment for crude oil and natural gas, BSM produced strong operating results in a very challenging market environment.”

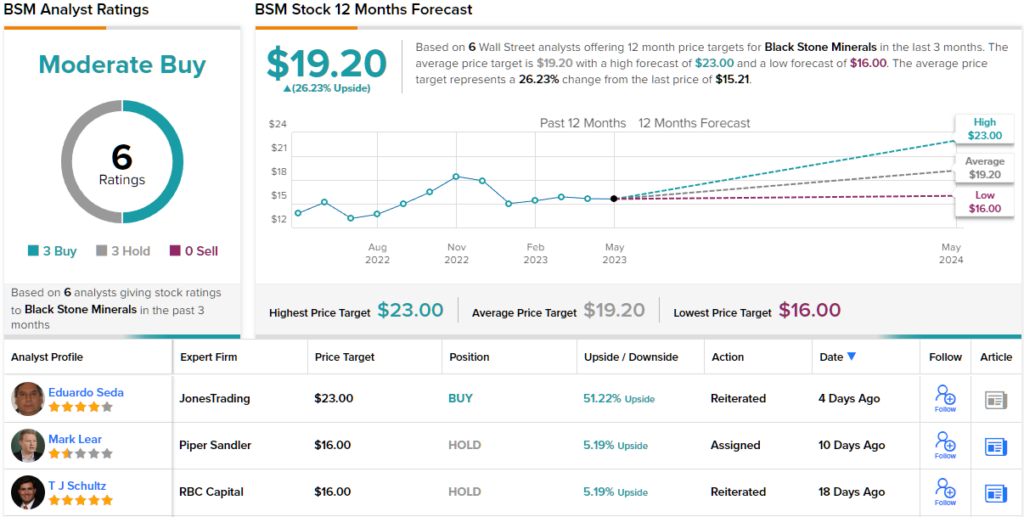

Seda goes on to rate the shares as a Buy, giving them a $23 price target that indicates room for 46% share appreciation on the one-year horizon. (To watch Seda’s track record, click here)

Overall, BSM has a Moderate Buy rating from the analyst consensus, based on an even split of 3 Buys and 3 Holds set in the past 3 months. The company’s stock sells for $15.21, and its $19.20 average price target indicates a possible 26% one-year upside. (See BSM stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.