Not long ago considered a trailblazing investing guru, sentiment has entirely shifted around Cathie Wood over the past year and a half. Her ARK Invest fund’s ARK Innovation ETF is loaded with growth-oriented pandemic-era winners but as anyone following the stock market’s trajectory will know, the tables have turned on stocks of that ilk. And the result is that the ARKK ETF is now down by a huge 65% in 2022.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Does that mean Wood is ready to desert her strategy of backing innovative yet risky and often unprofitable names in search of safer havens? No, is the short answer.

Wood not only points out that ARKK stocks have been growing at a faster pace than those of the Nasdaq 100 – ~31% revenue growth year-over-year vs. ~16% growth in the trailing four quarters as of the end of Q2 – and so have the “added wherewithal to accommodate investments in the future.”

“Nonetheless,” says Wood, “the market is paying little for what we believe is superior growth potential.”

And against a backdrop of rising interest rates that have reduced the current value of future cash flows, the value of “pure-play innovation strategies” has declined by 50-90% over the past 18 months, a turn of events in which the “equity markets seem to have bowed to GAAP EBITDA and shifted toward defensive low-growth strategies.”

But Wood thinks that’s the wrong way to go about investing and that the tides will turn again.

“We believe GAAP EBITDA falls short when measuring the longer-term growth and profitability profile of early stage, rapidly growing, innovative companies,” she said. “In our view, the long-term profitability and equity performance of so-called ‘profitless tech’ companies will dwarf those of companies that have catered to short-term oriented shareholders with share repurchases and dividends, at the expense of investing in the future.”

Is Wood right? Only time will tell. In the meantime, we’ve decided to take a look at the fund’s top two holdings to see why she’s so confident they are long-term winners. We’ve also opened up the TipRanks database to find out whether the Street’s experts are in agreement. Let’s check the results.

Zoom Video Communications (ZM)

Taking the first spot and accounting for 9.36% of the ARKK ETF with a value of more than $605 million is that most pandemic-era of stocks, Zoom Video Communications.

You don’t have to be an avid follower of the stock market to know the Zoom story. A niche video conferencing product at the onset of the Covid-19 pandemic, with the advent of global lockdowns, it quickly turned into a ubiquitous tool used by millions worldwide – from businesses to families to education bodies. As a result, the stock soared to incredible heights during 2020, but as has happened to so many, the comedown has been vicious. Shares sit 90% below the highs of October 2020 and have shed 64% this year.

That said, the company’s most recent report for the third fiscal quarter (October quarter) was a decent one. Revenue came in at $1.1 billion, representing a 4.8% year-over-year increase and meeting Street expectations. On the bottom-line, adj. EPS of $1.07 beat the analysts’ forecast of $0.83.

The number of customers contributing over $100,000 in the trailing 12 months revenue – an important metric signifying the product’s popularity with big businesses – increased by 31% from the same period a year ago. However, the outlook fell short of expectations and the shares drifted south following the print as has been the case throughout most of 2022.

Nevertheless, while MKM analyst Catharine Trebnick believes the company will need to prove its credentials in the current climate, she remains upbeat around its long-term potential.

“In the difficult near-term macro environment, management will need to show strong execution on new solutions and go-to-market initiatives to compete effectively and stabilize the Online business. Longer term, we continue to believe that the company’s positioning in a large and underpenetrated market opportunity can drive sustainable growth in a normalized environment,” Trebnick opined.

Trebnick’s confidence is conveyed by a Buy rating and a $100 price target. As such, the analyst sees shares climbing 53% higher over the coming year. (To watch Trebnick’s track record, click here)

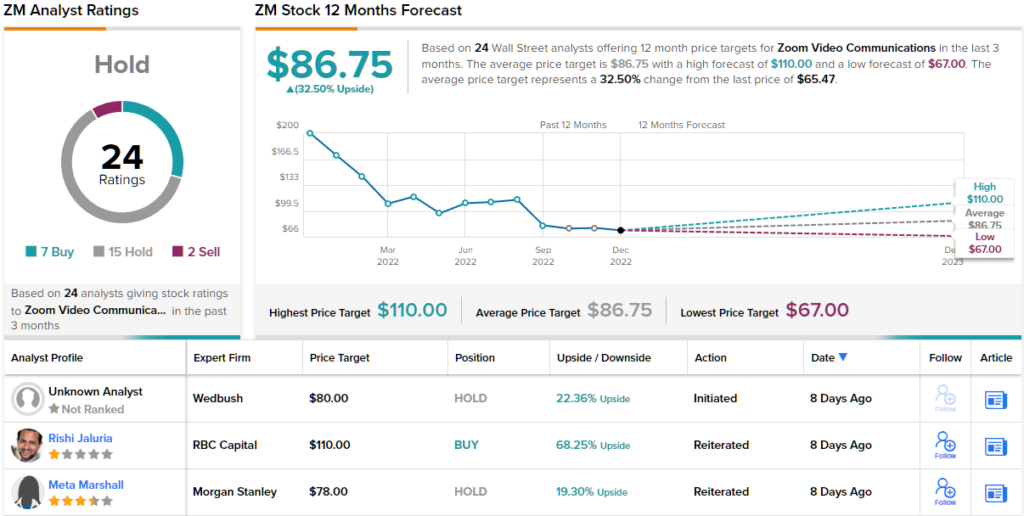

Most on the Street, however, are not quite as confident as Trebnick or Wood. The stock boasts a Hold consensus rating, based on 15 Holds (i.e. Neutrals) vs. 7 Buys and 2 Sells. Still, most believe the shares are now undervalued; the $86.75 average target makes room for 12-month gains of 32.5%. (See Zoom stock forecast on TipRanks)

Exact Sciences Corporation (EXAS)

ARKK’s second biggest holding is a completely different kind of innovator. Taking up 8.68% of space in the ETF and a holding worth more than $561 million, Exact Sciences is a molecular diagnostics specialist focused on detecting early-stage cancers. The company boasts a portfolio of various testing products led by its flagship offering, Cologuard, which as one of the most reliable non-invasive CRC (colorectal cancer) screening tests, boasts a strong market position.

In its most recent financial statement, for Q3, Exact Sciences put in a strong showing. Revenue climbed by 15% from the same period last year to $523.1 million, beating Wall Street’s forecast by $19.95 million. While the company posted a loss of $0.84 per share, the figure still managed to come in ahead of the -$1.07 anticipated by the analysts. Furthermore, the company raised its full-year revenue outlook to between $2.025 billion and $2.042 billion, $33 million higher at the midpoint than the prior forecast.

The market liked the results, sending shares higher in the subsequent session and the stock got another boost more recently. Last week, cancer screening rival Guardant announced top-line data for a blood-based cancer screening test which was a bit of a letdown. As a competitor, that is good news for Exact Sciences.

Among the bulls is Canaccord analyst Kyle Mikson who sees a string of catalysts ahead to boost the stock. He writes, “We believe 2023 will be another important year for data readouts that should remind investors (potentially a ‘wake-up call’) of Exact’s near-, medium- and long-term pipeline growth drivers… While peers are impacted by uncertain reimbursement and other issues, we believe these catalysts and the company’s relative stability should help drive EXAS valuation levels higher in 2023.”

“Additionally,” Mikson further explained, “we believe Guardant Health’s recent readout of the ECLIPSE screening study for the company’s liquid biopsy test lifted an overhang from EXAS shares that should allow the stock to perform well based on the company’s solid fundamentals in 2023.”

All of this prompted Mikson to rate EXAS stock a Buy, while his $70 price target makes room for 12-month gains of ~37%. (To watch Mikson’s track record, click here)

Most of Mikson’s colleagues are thinking along the same lines; based on 9 Buy ratings vs. 3 Holds, the stock garners a Strong Buy consensus rating. (See EXAS stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.