Medical devices company InMode (NASDAQ:INMD) has fallen out of favor with investors in the past two years for various reasons, which we’ll explain below. However, now that it’s down 76% from highs, the stock looks poised for upside. In our opinion, InMode has two major catalysts that could send shares notably higher in the blink of an eye. These two catalysts include the potential for an activist investor to take a stake in the company and push for buybacks or for InMode to finally make an acquisition.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

These sound like generic catalysts that can apply to any company, but we’ll illustrate why they’re important for INMD specifically. Nonetheless, even if these catalysts don’t materialize, InMode is still trading at a low valuation and can rise eventually. Therefore, we’re bullish on the stock.

What Does InMode Do?

InMode describes itself as a “leading global provider of innovative, minimally-invasive aesthetic and wellness solutions, with strong brand recognition.” In simpler words, INMD sells high-tech devices for beauty and health treatments, including procedures like skin tightening. Its clientele primarily includes professionals in the healthcare sector, such as plastic surgeons, dermatologists, gynecologists, and other medical specialists. The company is headquartered in Israel.

As many people are obsessed with how they look (especially due to social media), this is a money-making industry. In fact, the company’s net income in the trailing 12 months sits at $180.5 million.

Before Explaining the Catalysts, Here’s What You Need to Know

Before diving into what can send INMD stock higher, it’s important to learn about why it has been underperforming the market. On top of this, it’s key to look at its flawless balance sheet, as that’s what makes the two aforementioned catalysts possible.

Why Has INMD Stock Been Falling?

InMode was loved by the market up until late 2021, as you can see in the chart below. So what happened? Well, the first things that sent INMD lower were rising interest rates and the overall market falling in 2022. But many stocks have recovered since then, while InMode stock hasn’t. So, what gives?

First, the company has lowered its guidance in recent months. Prior to October 2023, InMode expected FY2023 to come in at $530-$540 million. This expectation then got lowered to $500-510 million in mid-October, and it got lowered again in December to $485-495 million before getting revised slightly higher to $495-505 million on January 16. EPS guidance was revised lower as well in the past few months. These revisions hurt investors’ confidence in management’s projections.

On top of this, the Israel-Hamas war added more uncertainty to the stock, as it’s headquartered in Israel. Nonetheless, INMD released a statement in October saying that it doesn’t expect to be affected by the war. Specifically, InMode stated, “We don’t anticipate any interruption to production. Our inventory levels globally and in Israel are sufficient and include components and subassemblies for the next three quarters.” Therefore, we’re not too worried about this risk.

Next, here’s one of the more important points. Investors are frustrated with the company’s deliberate decision to not buy back its own shares (you can find this frustration on social media), especially since the stock trades at a low forward P/E ratio of 9.2x based on 2023 estimates (with more earnings growth ahead), and the company has plenty of cash on hand. This brings us to our next point — InMode’s strong balance sheet.

InMode’s Balance Sheet is Flawless

InMode has a $675.85 million cash position as of the most recent quarter. This includes cash and cash equivalents, marketable securities, and short-term bank deposits. It also has $0 in debt. InMode’s cash pile has been growing over the years as the firm rakes in profits, but management has decided to save this money for a potential acquisition instead of buying back shares.

Now that you know this key information, let’s look at the two catalysts that can send InMode higher.

Catalyst #1: Potential Activist Investor Involvement, Share Buybacks

To be clear, we don’t know or haven’t heard of any activist investors who want to take a large stake in InMode. So, it’s not as if the market is expecting activists to get involved. However, given its large cash position and low valuation, it’s very possible that INMD stock will catch a large investor’s attention.

If this happens and the investor convinces (or forces) the company to buy back its stock, shares will likely spike, as buybacks are what many shareholders are hoping for. For context, InMode’s cash position makes up 35% of the company’s market cap, meaning that plenty of shares can be repurchased without using debt. This would lower the share count, driving earnings per share (EPS) higher.

Catalyst #2: InMode Finally Makes an Acquisition

As mentioned above, InMode isn’t keen on spending its cash unless it finds a company that’s good enough to acquire. Acquisitions carry risks, as management teams may overestimate how good the other company is. However, InMode’s management is very conservative, so if they do make a purchase eventually, it would likely be a great company that’s highly profitable like InMode.

In fact, in May 2023, InMode’s CEO stated, “Any company that we will acquire should not dilute the shareholders. It should be accretive and not dilutive. And it’s not easy. It’s not easy because of the profitability structure of InMode. So we’re very careful in the analysis that we’re doing on companies that we would like or that we’re exploring a possibility to do M&A.”

If the company makes an acquisition that’s big enough to excite investors, the stock can spike.

Is INMD Stock a Buy, According to Analysts?

On TipRanks, INMD comes in as a Moderate Buy based on three Buys and three Sells assigned in the past three months. The average INMD stock price target of $30.50 implies 31.2% upside potential.

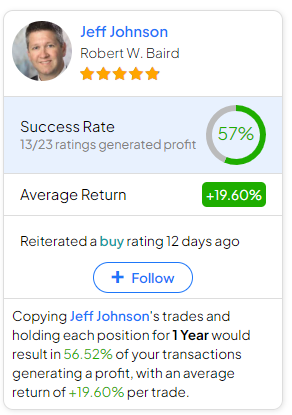

If you’re wondering which analyst you should follow if you want to buy and sell INMD stock, the most profitable analyst covering the stock (on a one-year timeframe) is Jeff Johnson of Robert W. Baird, with an average return of 19.6% per rating and a 57% success rate. Click on the image below to learn more.

The Takeaway

InMode is a profitable company trading at a low valuation. Apart from external factors that sent shares lower, investors have simply become frustrated with the company’s cash balance, as it keeps growing without being put to use. However, this leaves investors with upside potential, as it’s likely that sooner or later, the cash can be used for buybacks or an acquisition. Nevertheless, the stock can rise even if the company’s cash balance keeps growing, as its 9.2x forward P/E multiple implies a 10.9% earnings yield.