Markets are in a state of flux right now, with heavy changes on the near horizon. The collapse of Silicon Valley Bank – and the Fed’s takeovers of it and the crypto-heavy Silvergate and Signature banks – have sparked fears of a new banking or financial crisis, as well as calls for the Federal Reserve to pare back on its policy of interest rate hikes and monetary tightening.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The inflation numbers for February were in-line with expectations, with a monthly gain of 0.4% and an annualized rate of 6%. While this means that prices remain high, the rate of increase is moderating. For some context, the January annualized rate of inflation was reported at 6.4%.

Today’s inflation data has failed to clarify the picture, given crisis atmosphere in the bank sector. The news should give the Federal Reserve the impetus it needs to pare back on monetary tightening in a move that may support banks – without worry that inflation will run rampant. This runs against the central bank’s ‘prime directive’ of fighting inflation, but there’s deep uncertainty as to what comes next.

In the words of Mohamed El-Erian, “This roller coaster… is a reflection of economic, financial and policy volatility which, looking forward, will need time to settle down.”

For investors, the key point now is finding portfolio choices that can deliver results even as inflation remains high. The natural move will be a turn toward dividend stocks, the classic defensive play. We’ve used the TipRanks platform to pull up recent data on two high-yielding dividend payers, that combine Strong Buy analyst ratings with real rates of return.

Enterprise Products Partners (EPD)

The first dividend stock we’ll look, Enterprise, is a major player in the North America’s midstream energy segment. Enterprise boasts an extensive hydrocarbon transport network, centered on the Texas-Louisiana Gulf Coast and branching out to the Southeast, the Midwest, the Plains, and the Rocky Mountains. The company’s assets include pipelines, river barges, rail and road tankers, all leading to processing plants, refineries, tank farms, and terminals.

Enterprise reported strong income numbers in the fourth quarter of 2022. It’s financial results showed an operating income of $1.76 billion, up 25% year-over-year, and a net income of $1.45 billion, for a 36% y/y gain. Per share, the diluted EPS came to 65 cents, compared to 47 cents in the year-ago period. The 4Q22 EPS was also 3 cents better than forecast.

The company managed these impressive earnings results even as revenues slipped. The top line, of $13.65 billion for the quarter, marked the second consecutive quarter-over-quarter drop in revenue, and it came in more than $1 billion below expectations. On a positive note, year-over-year, revenue was still up 19%.

Of interest to dividend investors, the firm’s distributable cash flow came to $2.03 billion for the quarter, and $7.75 billion for the full year. These represented y/y gains of 22% and 17% respectively. The gains in distributable cash flow allowed Enterprise to support a generous dividend, and in its most recent declaration, on January 5, the company raised its 4Q22 dividend payment by 2 cents, to 49 cents per common share. At the annualized rate of $1.96, the dividend yields 7.7%.

With a dividend like that, investors should rest calmly. It’s a full 1.7 points higher than inflation, guaranteeing both a steady income stream and a real rate of return.

EPD shares have caught the attention of Scotiabank analyst Tristan Richardson, who sees this year and next as a growth period for the company.

“We see FY2023 as a year with several earnings catalysts, with several large projects coming online during the year that could offset the difficult comps around the commodity and sets up FY2024 for free cash flow (FCF) expansion. With scheduled downtime in FY2022 for the propane dehydrogenation facility (PDH) and planned commissioning of PDH2, we expect some baseline for petchem growth in FY2023 against slowly reopening global downstream demand,” Richardson opined.

“We also expect the United States to remain extremely competitive from an export standpoint as production growth necessitates that NGLs price to clear EPD docks. Separately, balance sheet flexibility suggests greater opportunity for return of capital to shareholders,” the analyst added.

Richardson’s view of Enterprise’s prospects going forward backs up his Overweight (i.e. Buy) rating on the shares, and his $31 price target indicates his confidence in a 21% one-year upside. Based on the current dividend yield and the expected price appreciation, the stock has ~28% potential total return profile. (To watch Richardson’s track record, click here)

Overall, the 11 recent analyst reviews on EPD break down to 10 Buys and 1 Hold, for a Strong Buy consensus rating. The stock is currently trading for $25.72 and its $31.91 average price target implies an increase of 24% in the year ahead. (See EPD sock forecast)

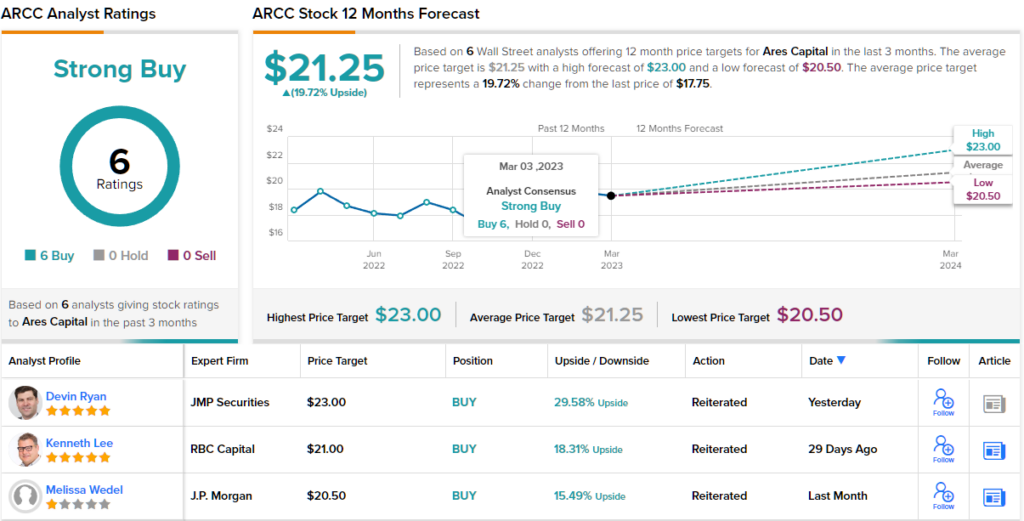

Ares Capital Corporation (ARCC)

From energy stocks we’ll shift our gaze to business development. Ares Capital is a business development company, or BDC, making available new sources of capital to small and medium sized businesses that wouldn’t necessarily get access through the more traditional banks. Ares provides funding, credit facilities, and other financial instruments to the companies in its target niche.

Ares’ investment portfolio, as of the end of 2022, contained 466 companies with backing from 222 private equity sponsors. The portfolio had a fair value of $21.8 billion, and was made of mainly (over 61%) of first lien and second lien senior secured loans. Of the remainder, nearly half was in various equity securities.

This portfolio brought the company some solid numbers in 4Q22. Total investment income came to $640 million, up 21% year-over-year – and nearly $56 million better than had been forecast. Drilling down, the core EPS of 63 cents was up 8.6% y/y, and beat expectations by 7 cents. The company finished the year with $303 million in liquid assets on hand.

With that in the background, we can see why Ares kept its dividend payment at 48 cents per common share in its recent declaration. The payment, to go out at the end of this month, marks the second month in a row with the common dividend at this level; the company has been raising the payment since the middle of 2021, and has also been paying out frequent special dividends. The common share div annualizes to $1.92, and gives a yield of 10.8%. That’s a solid return, that beats inflation by 4.8 points.

5-star analyst Devin Ryan covers this stock for JMP, and is pleased with its prospects for 2023. Ryan writes of Ares, “Given elevated concerns around credit, we are optimistic that ARCC is well positioned to outperform given its track record of superior credit underwriting, an experienced and long-tenured management team, a best-in-class origination platform, and the benefit of a multi-cycle-tested business model. In short, we continue to view Ares Capital as one of the best-positioned BDCs to outperform in a challenging and uncertain macro environment in 2023 given the competitive advantages of the Ares platform.”

These comments back up Ryan’s Outperform (i.e. Buy) rating on the stock, while his price target of $23 implies a gain of 29% on the one-year time horizon. (To watch Ryan’s track record, click here)

Overall, this stock has 6 recent analyst reviews on file, and they are all positive – for a unanimous Strong Buy consensus rating. The shares are priced at $17.74 and the average price target of $21.25 suggests an upside potential of ~20% for the next 12 months. (See ARCC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.