The April CPI Consumer Price Index (CPI) report is in and the data showed that headline inflation increased by 0.4% compared to last month and by 4.9% over last April. That represents the slowest annual rate increase since April 2021.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

While inflation remains high, the deceleration shows the Fed’s aggressive attempts to tame it are working. That is the opinion of John Stoltzfus, Chief Investment Strategist at Oppenheimer, who says the Fed’s efforts “seem to have been the right course of action.”

In fact, in contrast to those seeing doom and gloom ahead when considering the state of the economy and its impact on the markets, Stoltzfus keeps an upbeat outlook.

“We remain highly constructive on equities as the economy continues to show signs of slowing while not falling off the proverbial cliff,” Stoltzfus opined. “Q1 S&P 500 earnings season has shown the ability of many companies to navigate challenging waters of the significant transition taking place stateside and around the world in moving from post pandemic to what we expect will be a ‘next new normal’ replete with a rate of sustainable economic growth if at a moderate pace.”

With Stoltzfus’ take in mind, we checked out two stocks that have scored rave reviews from Oppenheimer. Impressing the firm’s analysts, they believe that each could deliver double-digit returns for investors. Using TipRanks’ platform, we wanted to see if other Wall Street analysts agree with Oppenheimer’s calls. Here’s what we found out.

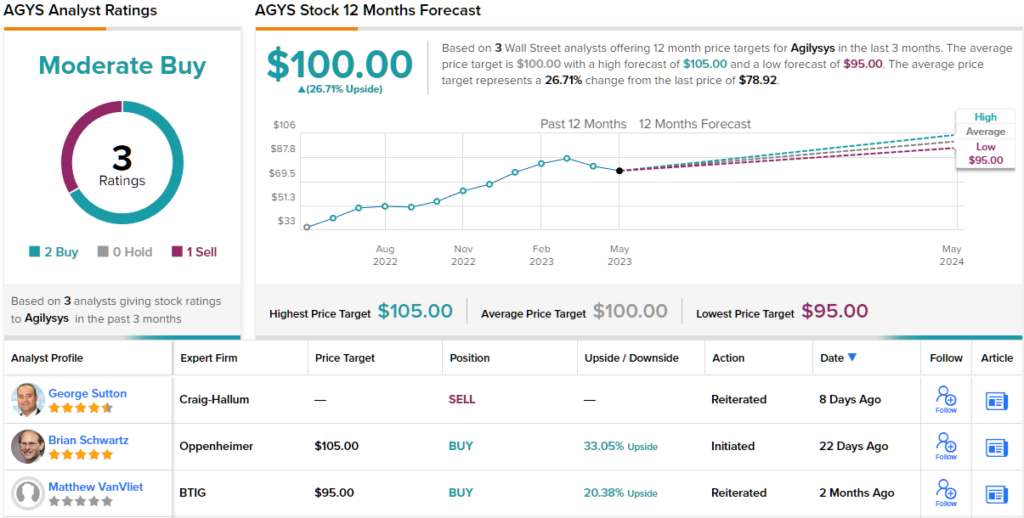

Agilysys, Inc. (AGYS)

For the first Oppenheimer pick, we’ll turn to the area of great Atlanta, in Georgia. Agilysys, based in the suburb of Alpharetta, has been in the software business for over 40 years, and today delivers cloud-based solutions in the hospitality industry. Agilysys’ software packages offer a range of value-added uses for hotels, resorts, cruise operators, gaming providers, corporate foodservice, restaurants, and sports & entertainment venues.

The software solutions, available to customers through the popular SaaS subscription model, include applications for point-of-sale, property management, inventory and procurement, payments, and loyalty programs, among others. The packages are designed to both manage and streamline the guest experience. Agilysys has a history of making strong investments in R&D, to keep its platform products up to date and relevant. The company has a global footprint, with operations in every major travel destination.

The past year and a half – the post-COVID period, in which the economy opened up and travel resumed – has been good for Agilysys. The company has seen mostly rising revenues and generally positive earnings over this time, and in the last reported quarter, fiscal 3Q23 (December quarter), the firm’s financial results beat the forecasts at both the top and bottom lines.

Agilysys notched revenues of $49.9 million, up 26.5% year-over-year and more than $1.78 million higher than expected. On earnings, Agilysys reported a non-GAAP EPS of 26 cents, for a 36% y/y increase – and a beat of 5 cents compared to estimates.

Even better, from an investor’s perspective, Agilysys raised its revenue guidance for fiscal year 2023 from the range of $190 million to $195 million to a new range of $195 million to $198 million – higher than the $194.57 million guidance Wall Street had predicted. The new guidance includes an estimate of 30% y/y growth in subscription revenue.

Assessing Agilysys’ prospects, Oppenheimer 5-star analyst Brian Schwartz describes Agilysys as a ‘nifty profitable growth business.’

“We are unaware of any pure play software supplier in hospitality comparable with Agilysys in subscription growth and EBITDA margin (i.e, Rule of 45), breadth of platform technologies, scale, and customer satisfaction. Additionally, there are structural industry and consumer demand changes driven by the COVID-19 pandemic compelling a long-tail refresh and new product cycles, and thus lower cyclical risks for Agilysys relative to other software industries,” Schwartz explained.

“We expect Agilysys’s profitable growth opportunity to demonstrate sustainability because of its leading technology vision, low product penetration, high referenceability, bad legacy competition, and strong management team,” the analyst added.

Looking ahead, Schwartz rates AGYS stock an Outperform (i.e. Buy), and his $105 price target implies a one-year upside potential of 33%. (To watch Schwartz’s track record, click here)

According to TipRanks, this stock gets a Moderate Buy consensus rating from the Street, based on 3 recent reviews, which include 2 Buys and 1 Hold. The shares are trading for $78.92, and their $100 average price target suggests a gain of ~27% over the coming 12 months. (See AGYS stock forecast)

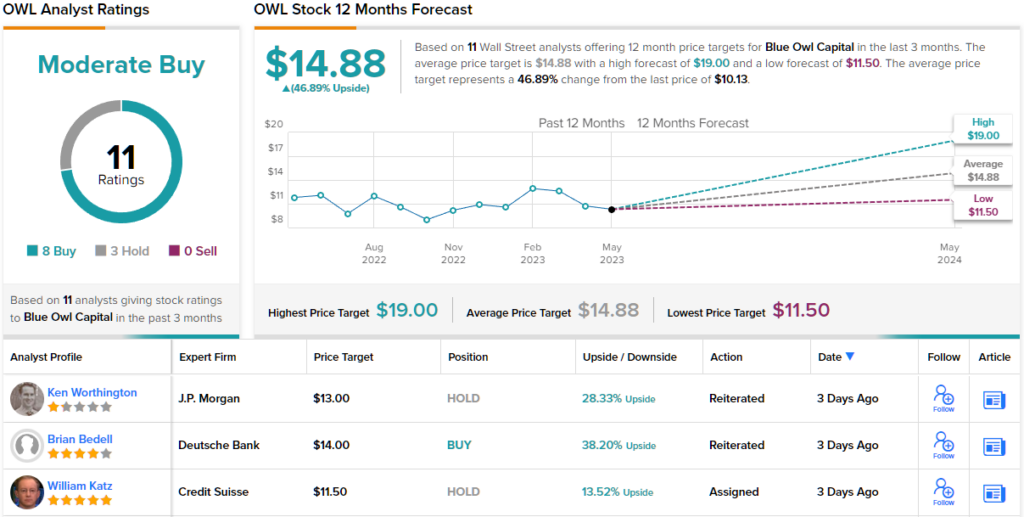

Blue Owl Capital (OWL)

Now we’ll switch gears and move over to the financial industry, where Blue Owl Capital operates as an asset management firm focused on alternative investments. The company works through several subsidiaries, including Dyal Capital, a private capital provider for institutional private equity and hedge managers; Owl Rock, a provider of customized private credit and financing solutions; and Oak Tree, a leader in real estate and tailored leaseback solutions. Blue Owl as a whole focuses on maintaining risk-adjusted, attractive, returns for shareholders.

The company was formed through a SPAC transaction in the spring of 2021, merging Owl Rock and Dyal with Altimar Acquisition. Since the transaction completed, Owl Rock has closed over 730 deals and opened 10 offices in North America, Europe, and Asia. The company has more than $144 billion in total assets under management, a total that at the end of 1Q23 was up 42% from the same period a year ago.

Revenues were also up in the quarter. The company showed a top-line of $390.99 million. This beat the forecast by $5.9 million, and was up more than 41% y/y. On the bottom-line, non-GAAP EPS of 15 cents met expectations, and was up 36 cents from the prior year.

While Blue Owl has only been public for two years, it has provided investors with a steadily growing dividend over that time period. The company’s current dividend, of 14 cents per share and scheduled for a May 31 payout, is more than triple the original 4-cent div paid out in August 2021. The current payment annualizes to 56 cents and yields an above-average 4.5%.

The Oppenheimer view on this stock is decidedly upbeat. 5-star analyst Chris Kotowski, who covers OWL, writes: “We view OWL as one of the premier alternative asset management platforms integrating multiple experienced management teams with proven track records overseeing investment strategies well posed against the current backdrop. Though historically trading at a premium against our fair value methodology, OWL has now retreated to an attractive valuation following dislocation in the financial sector while company fundamentals and our outlook remain largely intact.”

Kotowski goes on to rate OWL shares as Outperform (i.e. Buy), and to set a $13 price target indicating room for 28.5% share appreciation in the coming year. Based on the current dividend yield and the expected price appreciation, the stock has ~33% potential total return profile. (To watch Kotowski’s track record, click here)

Overall, there are 11 recent analyst reviews on OWL, with a breakdown of 8 to 3 in favor of Buys over Holds, all combining for a Moderate Buy consensus rating. The stock’s $14.88 average price target and $10.13 trading price combine to suggest ~47% one-year upside potential. (See OWL stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.