I am bearish on Ideanomics (IDEX) due to its excessively lofty valuation and very poor performance on the TipRanks Smart Score rating system, which combine to pose significant downside risk.

Ideanomics is a multinational EV company committed to driving the adoption of commercial EVs, and related sustainable energy consumption. With its cutting-edge technology, Ideanomics has been reducing the cost of fleet ownership for operators and reducing greenhouse gas emissions. (See Insiders’ Hot Stocks on TipRanks)

Strengths

Ideanomics has announced a versatile range of business initiatives across its mobility subsidiaries, including US Hybrid, WAVE, and Solectrac, which show increased avenues for the company to generate long-term growth.

It has made many strategic acquisitions to make its portfolio strong and — although the company is facing pressure to become profitable — it is still generating higher profitability compared to many of its competitors.

Recent Results

Ideanomics’ second quarter saw a loss of $0.02 per share. This is in comparison to a loss of $0.15 per share in the prior-year quarter, adjusted for non-recurring items.

In the second quarter, analysts expected a loss of $0.03 per share, but the company actually generated break-even earnings, delivering an earnings surprise of 100%.

Over the past four quarters, Ideanomics has only been able to surpass analyst consensus just once.

The company showed a revenue of $33.2 million, which showed the sixth consecutive quarter of growth, indicating the business’ strength. The second quarter also included the very first revenue generated from US Hybrid and Solectrac, which was acquired by Ideanomics in September 2021.

Revenue from the Electric Vehicles segment saw an increase of $6.1 million, up from $0.7 million year-over-year. Meanwhile, revenue from Batteries, Charging, and Powertrains stood at $2.7 million. This segment did not generate any revenue in the prior-year quarter.

The company also showed a gross profit of $9.3 million for the second quarter, which represented a gross margin of 28%. This is in comparison to the $0.3 million gross profit for the second quarter of 2020.

Valuation Metrics

Ideanomics’ stock is very difficult to value right now given that the company is running up large losses at the moment, and is not expected to turn profitable anytime soon.

That said, the company is expected to grow rapidly in the coming years, with revenue forecast to increase by 391% in 2021 and 10.4% in 2022. EBIT margins are also expected to improve from -29.2% in 2021 to -22.6% in 2022, implying that the company is on the path towards profitability.

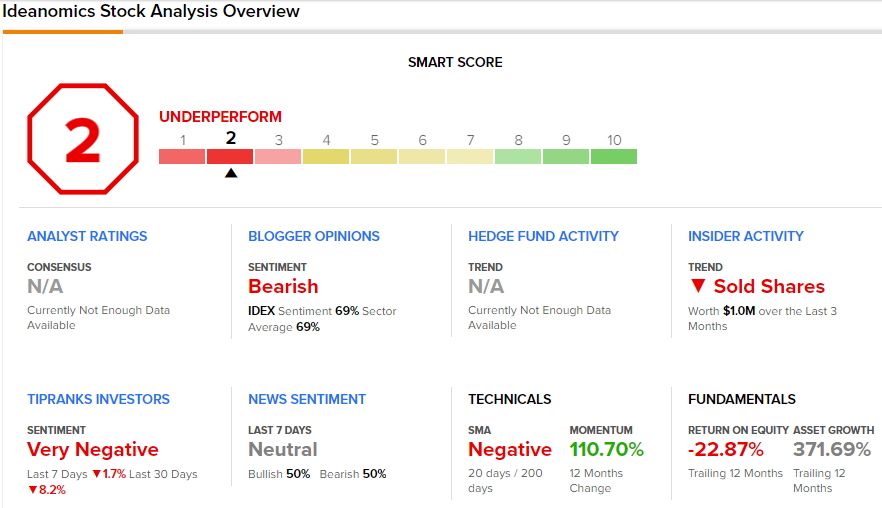

Smart Score Rating

Ideanomics scores a 2 out of 10 from the TipRanks Smart Score rating system, indicating that it is on the lower end of the neutral range. This is based on very negative sentiment from TipRanks investors, negative technicals, bearish blogger opinions, and neutral news sentiment.

Summary and Conclusions

Ideanomics operates in a high growth industry, and has enormous upside potential. However, the company is not yet profitable and all indications point to it being several years at least before the company can become consistently profitable.

Furthermore, there is a lot of competition in the EV space, so there are no guarantees that it will be able to continue scaling towards profitability. Finally, the company scores very poorly on the TipRanks Smart Score rating system, indicating that it might not be an ideal time to purchase shares.

While the stock could yield massive returns to investors if the company can effectively capture market share and scale rapidly towards profitability, investors should keep in mind that the stock is very speculative at this point.

Disclosure: At the time of publication, Samuel Smith did not have a position in any of the securities mentioned in this article.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates, and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices or performance.