Every investor knows that there’s a ‘trick’ to succeeding in the stock market. The first step toward a winning strategy is to find stocks that are priced low but still boast solid assets that bode well for future gains. In short, the key is finding stocks that are undervalued relative to their potential, and to buy in now while the shares, along with the broader markets, are down in the doldrums.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Wall Street’s analysts are seeing plenty of, in their words, undervalued stocks that are primed for gains despite the challenging market environment. We’ve used the TipRanks database to pull up the details on two such stocks. According to the analysts, both share high upside potential – upwards of 50% – for the next 12 months. Let’s take a closer look.

Shyft Group, Inc. (SHYF)

We’ll start in the automotive industry, where Shyft Group, based in Novi, Michigan, works on automobile designs in several niche markets. Shyft designs, engineers, and manufactures truck bodies, specialty vehicles, and specialty chassis, as well as aftermarket parts, for marketing and delivery to the RV market, government agencies, and the delivery and service markets. Shyft’s vehicles are widely used in the ‘last mile’ segment of the delivery business.

In the third quarter of this year, which Shyft reported on in October, the company showed a top line of $286 million. This was up 5%, or $13.5 million, year-over-year. While sales were up, earnings were down, from $21 million in 3Q21 to $17.3 million in 3Q22. These totals break down to 58 cents per share in the year-ago quarter and 49 cents in the current report, a drop of 15%.

On a positive note for Shyft’s future performance, however, the company reported a massive work backlog, totaling $1 billion, as of September 30. This figure was up by $191.3 million year-over-year, or 22.4%, and showed that the company is seeing strong demand across the full range of its business units.

Investors should note that Shyft shares have fallen 52% this year. At least one analyst, however, believes that now is the time to buy the dip.

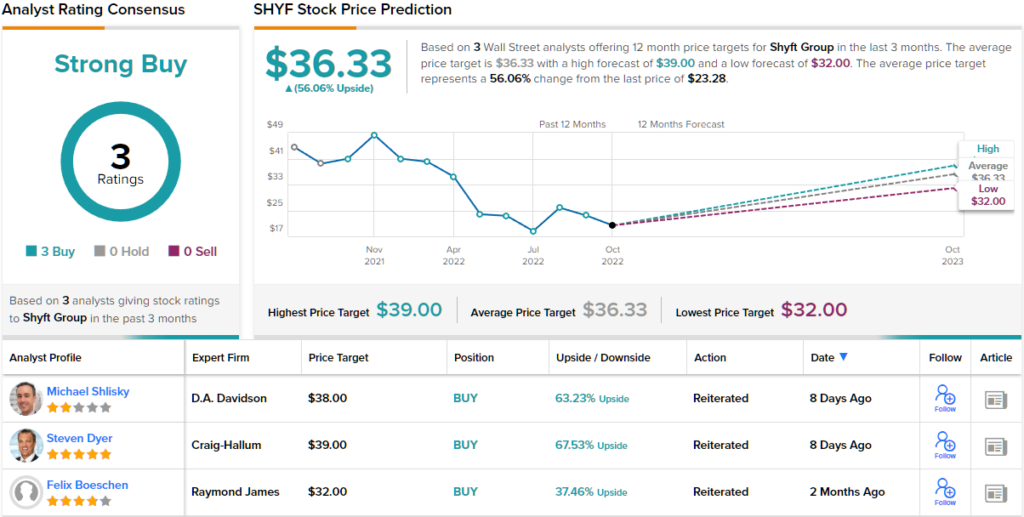

In his coverage of Shyft Group for Craig-Hallum, 5-star analyst Steve Dyer describes the stock as undervalued in light of easing supply chain challenges and strong near-term EV opportunities.

Getting into details, Dyer writes: “We think SHYF’s stock can outperform from here given an improving supply chain (and margins), much improved operating leverage on EV initiatives going forward and a year-plus of backlog. The company has positioned itself as the only supplier of Class 2-7 final mile vehicles offering both ICE and EV powertrains beginning mid-23. We believe that, combined with its national footprint and blue-chip customer list, this positions them as the supplier of choice for final-mile vehicles going forward.”

“After a year-plus of supply-chain challenges and heavy EV investment spend, we expect significant profitability improvement next year and believe investors will be rewarded,” the top analyst summed up.

Dyer’s comments back up the Buy rating he puts on the stock, and his price target, set at $39, suggests that SHYF has an upside of 67% on the one-year horizon. (To watch Dyer’s track record, click here)

Overall, Shyft has acquired 3 recent analyst reviews, unanimously positive for a Strong Buy consensus from the Street. The $23.28 trading price and $36.33 average price target give the stock a 56% upside potential going forward into next year. (See SHYF stock analysis on TipRanks)

KemPharm (KMPH)

Next up is KemPharm, a commercial and clinical stage biopharmaceutical company engaged in the discovery, development, and commercialization/marketing of new medications and treatments for rare diseases of the central nervous system (CNS). Specifically, the company is working on treatments for neurodegenerative and lysosomal storage diseases. KemPharm boasts a diverse portfolio, with new drug programs ranging from preclinical stages, to late-stage human clinical trials, to new drug applications (NDA) filed with the FDA, to approved drugs going on the market.

For the moment, KemPharm reported several important updates, which will determine the company’s course going forward. First, KemPharm completed its acquisition of arimoclomol, a treatment for Neimann-Pick disease type C (NPC), as part of its purchase of Orphazyme. The total purchase cost KemPharm $12.8 million; the most immediate gain for the company will be the 1Q23 resubmission of the arimoclomol NDA.

Next, the company completed its investigational new drug (IND) application for KP1077, a treatment for idiopathic hypersomnia (IH). The company is in process of initiating a Phase 2 trial for KP1077 on this indication, and expects to begin the study before the end of this year. A Phase 3 trail for KP1077 in the treatment of narcolepsy is also being planned, to take place after the Phase 2 IH study.

And finally, KemPharm has continued on the path for commercialization of its two approved drugs, Azstarys and Apadaz. Azstarys, a treatment for ADHD in children ages 6 and up as well as adults, was approved for US use in March of last year. This is a crowded market, but KemPharm has begun receiving royalties on the drug, and reported $1.3 million in revenue for Q2.

For the year so far, shares in KMPH are down 37%. But this may provide the needed opening for investors, at least in the view of Canaccord’s Sumant Kulkarni.

“Our thesis is that KMPH is significantly undervalued as: 1) a deepened focus on CNS rare diseases is under-appreciated by the market; 2) the arimoclomol deal is strategically/financially prudent and helps generate cash flows relatively quickly; 3) KP1077 could be a differentiated product for IH (competition is limited); and 4) Azstarys royalties could pleasantly surprise. We also like KMPH’s cash runway that extends beyond 2025E, which affords it the flexibility to build its rare CNS pipeline,” Kulkarni wrote.

Looking forward based on this stance, Kulkarni gives KMPH shares a Buy rating with a $20 price target to indicate room for a robust 262% upside in the year ahead. (To watch Kulkarni’s track record, click here)

Like Shyft above, this small-cap biopharma firm has picked up 3 analyst reviews in recent weeks – and they are all positive, to support a unanimous Strong Buy consensus rating. The stock is currently trading for $5.52 and its $19.33 average price target implies a one-year upside potential of 250%. (See KMPH stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.