According to the latest CPI (consumer-price index) report, U.S. inflation cooled down slightly from July but not enough to appease the markets.

Overall prices rose by 8.3% from the same period a year ago, slowing down from July’s 8.5% uptick and further down from June’s 40-year high showing of 9.1%. On a monthly basis, after plateauing in July, consumer prices rose by 0.1%.

As the expectation was for a rise of 8.1% over last year and a drop of 0.1% compared to last month, the markets did what they are wont to do in such a situation – they fell big time.

The latest setback is not what embattled investors had hoped for, having thought the worst of the bear market was already behind us. That said, according to Lori Calvasina, the Head of U.S. Equity Strategy at RBC, the bottom could indeed already be in but that still doesn’t mean it’s plain sailing from now on.

“In terms of stock market direction, we think it’s more likely than not that US equities saw their lows in mid June, but have expected conditions to turn choppy again in the months ahead with risk that the S&P 500 will retest its YTD low again in late 3Q,” Calvasina opined.

Given that situation, investors would do well to make defensive plays, and RBC analysts are pointing out some big dividend stocks for just that. These are div players offering yields of 8% or better, and according to TipRanks database, they both have a ‘Strong Buy’ consensus rating from the wider analyst community. Let’s take a closer look.

Blackstone Secured Lending Fund (BXSL)

The name ‘Blackstone’ is readily recognized; it is one of the largest asset management firms in the world today. Blackstone Secured Lending Fund, the first stock we’ll look at, is managed by the eponymous firm, and has operated since 2018 as a business development company with a portfolio of first lien senior secured debt in US private companies.

Getting into detail, the company’s portfolio investments are worth $10.1 billion at fair value, and are focused mainly on software and healthcare providers, which together make up 27.5% of the whole. The remaining investments include professional services, commercial services, and insurance, which make up another 22.5%. Most of the portfolio investments are in the US, although some 5.23% are in Canadian companies.

BXSL saw $105 million in net investment income during Q2, its third reported quarter since going public in October of last year. This income came to 62 cents per share, and was enough to cover the 60-cent per common share dividend declared last week for payment in November. The dividend is currently yielding 10%, well over 4x the average dividend yield among peer companies.

RBC 5-star analyst Kenneth Lee has been following BXSL, and is impressed by this company’s performance – and by its potential to gain in an environment of rising interest rates. This will have the added advantage, for investors, of potentially translating into higher dividends – a key point, when the current yield is already beating inflation.

“We continue to favor BXSL’s conservative risk profile, especially in the current macro backdrop; potential for expanding dividend coverage in n-t as NII increases from rising rates… Management indicated had BXSL received the benefit of increased rates at the end of the quarter, for the full quarter, NII would have been 11c higher. Looking forward, rate sensitivity is such that every 100bps increase in rates from June 30 would translate into roughly 9c/sh increase in quarterly NII. Consequently, management believes dividend coverage could grow,” Lee wrote.

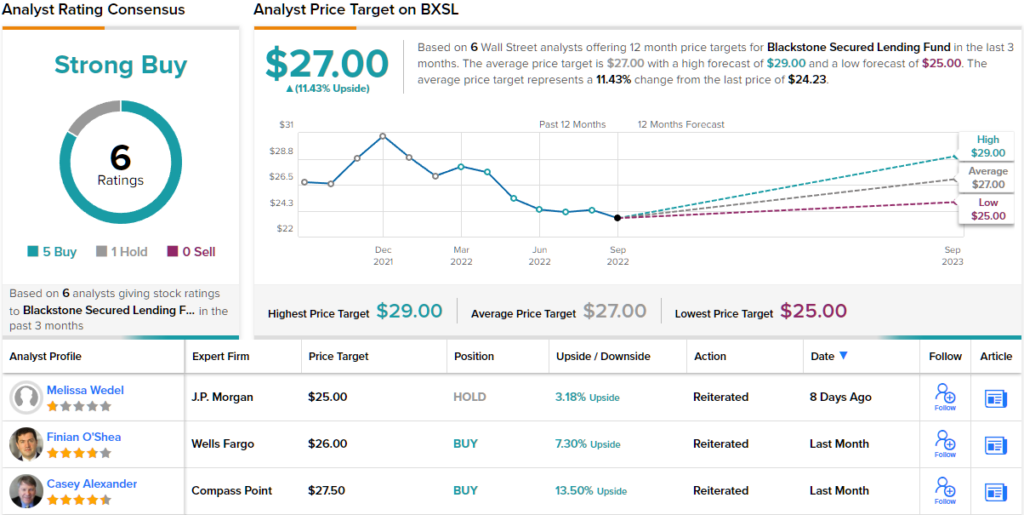

All of this firmly backs up Lee’s Outperform (i.e. Buy) rating on the shares. His price target, set at $29, suggests that BXSL will gain ~20% in the year ahead. Based on the current dividend yield and the expected price appreciation, the stock has ~30% potential total return profile. (To watch Lee’s track record, click here)

BXSL has been public for less than a year, and has 6 Wall Street reviews on file. These include 5 to Buy against 1 Hold, for a Strong Buy consensus view. The shares are trading for $24.23 and the $27 average price target implies ~11% upside from that level. (See BXSL stock forecast on TipRanks)

Sunoco (SUN)

The next dividend stock we’ll look at is Sunoco, a master limited partnership (MLP) and the U.S.’s largest independent distributor of motor fuels. Sunoco’s fuel products are bought from refiners and sold wholesale to roughly 10,000 convenience stores, independent dealers, commercial customers and distributors – the bulk of which are third party-owned and operated. To get an idea of the size we’re talking about here, in 2Q22, the partnership sold roughly 2 billion gallons of fuel, a 3% increase compared to Q2 2021.

The results were released early last month and showed that revenue increased by 78.1% year-over-year to $7.82 billion, handily beating the Street’s call for $5.63 billion. There was a beat on the bottom-line too with EPS of $1.20 outpacing the analysts’ prediction of $1.06. The company also stuck to its full-year 2022 Adjusted EBITDA guidance of $795 to $835 million.

As far as the dividend is concerned, the quarterly payout stands at $0.82, yielding a handsome 8.34% – some distance above the sector average of 1.64%.

Sunoco’s business is based on the transportation of fossil fuels, and with climate change on the agenda, and the auto industry expected to pivot heavily toward EVs over the coming years, there could be long-term repercussions for its segment.

However, it could be a while before the full transition takes place and in covering this stock for RBC, Elvira Scotto applauds a model which “continues to work.”

“SUN reported solid 2Q22 results that slightly exceeded expectations and maintained its full year 2022 outlook,” the 5-star analyst wrote. “Second quarter results once again highlight the resiliency of SUN’s model. We believe SUN shows investors sizable current income with an improved balance sheet. We expect SUN to maintain its distribution and expect distribution coverage to improve over time.”

These comments underpin Scotto’s Outperform (i.e., Buy) rating, while her $48 price target makes room for one-year gains of 21%. (To watch Scotto’s track record, click here)

The rest of the Street is thinking along the same lines. All 4 other recent analyst reviews are positive, coalescing to a Strong Buy consensus rating. Given the average target clocks in at $47, the shares are expected to yield returns of ~19% over the coming months. (See Sunoco stock forecast on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.