Most people following auto industry trends agree that the future resides with electric vehicles. However, the road to EV domination looks to be far from a smooth one.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

That has been evident this year as the fledgling industry has faced a big challenge. Namely, too much supply vs. waning demand, and that in turn has caused investors to turn their backs on this secular trend.

This is acknowledged by Needham analyst Chris Pierce, who still has high hopes for the EV industry although he makes the case it might be a while until sentiment turns positive again.

“We are bullish over the longer term on EV adoption,” Pierce recently said, “but we concede that investor enthusiasm has faded, with shorter term demand issues winning out and minimal catalysts to shift investor views until inventory starts to clear at a faster rate.”

The malaise has been broad-based, and as such, legacy OEMs have stepped on the brakes to slow the speed of transition to an EV only world. You could make the argument that would be good news for EV-only OEMs, but generally speaking, that has not been the case as has been evident from the recent developments at segment leader Tesla (NASDAQ:TSLA).

To counter waning demand, the EV leader has brought about several rounds of price cuts. While that has boosted volume, it has also eaten into the margin profile. The problem, says Pierce, is that things are unlikely to improve to a meaningful extent over the course of the next year. “We agree with the prevailing thesis that automotive gross margins ex regulatory credits have bottomed,” he explained, “but we model minimal gross margin improvement in ’24 given TSLA’s willingness to use price as a weapon consistently in ’23, vs a 150bps y/y improvement in the consensus estimate.”

Therefore, Pierce says it’s hard to “get comfortable with TSLA’s margin profile.” Furthermore, the analyst sees the other parts of the business that are supposed to provide “upside levers,” such as FSD, Bots and AI, with a “higher degree of skepticism vs the valuation currently reflected in the stock.”

To this end, Pierce reiterated a Hold (i.e., Neutral) rating on TSLA shares without offering a fixed price target. (To watch Pierce’s track record, click here)

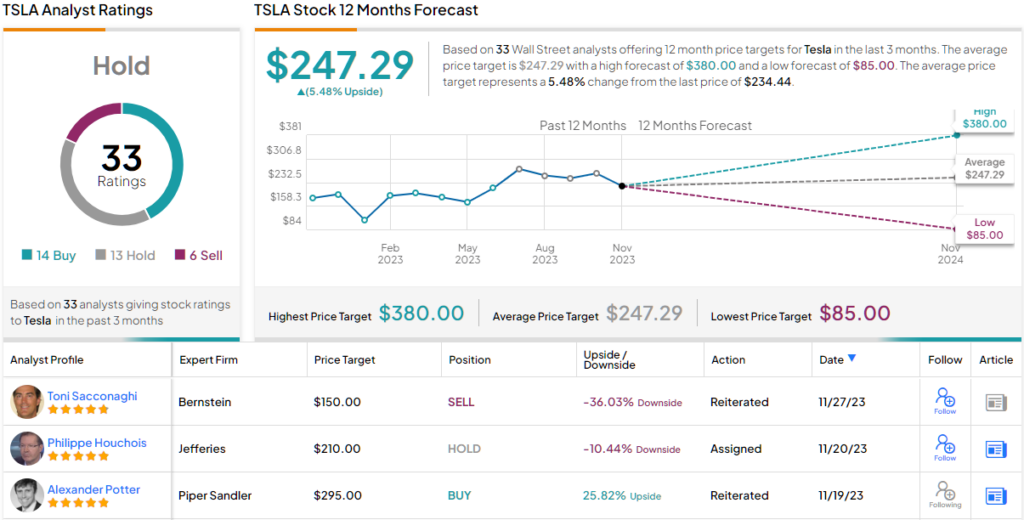

Other analysts do have a price target in mind and the average on the Street currently stands at $247.29, suggesting shares have room for only modest growth of 5.5% in the year ahead. Rating wise, based on a combination of 14 Buys, 13 Holds and 6 Sells, the stock claims a Hold consensus rating. (See Tesla stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.