In this piece, we’ll weigh in on hotel chain Hilton (NYSE: HLT) and short-term homestay leader Airbnb (NASDAQ:ABNB) with help from TipRanks’ Comparison Tool.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Over the past few years, Wall Street analysts have been busy downgrading stocks from across the board. In some cases, they’ve had to downgrade after already sizeable downside moves. When it comes to stays plays, Wall Street stands firm, with upbeat estimates, even given daunting macro headwinds ahead.

Undoubtedly, the COVID-19 pandemic is still ongoing and could act as an overhang on the stays stocks for longer. Though restrictions are off and things have mostly returned back to normal, seasonal outbreaks could continue to have an effect on the demand for stays. Even if the pandemic is nearing its end, the winds of recession are up ahead. Travel and stays are discretionary (nice-to-have) experiences that are among the first things to be cut from one’s budget.

Indeed, trips and experiences tend to be postponed due to economic circumstances. At this juncture, it’s unclear how long such travels can be delayed. In the case of a severe recession, consumers could delay previously-planned experiences indefinitely. And that poses a major risk for the stays stocks, as they look to discount and endure a hit straight on the margin.

In the meantime, the travel recovery still seems to be on stable footing. Hotel chains like Hilton have been holding their own better than most other firms.

Hilton (HLT)

Hilton is an asset-heavy hospitality kingpin with a deep portfolio of hotel properties. For traditionalists, Hilton is a preferred way to play a rebound in travel and leisure demand. At writing, the stock is down more than 20% from its all-time high. That’s in line with losses endured by the S&P 500.

Though demand could fade as we enter a recession in 2023, the company’s wealth of hotel assets isn’t going anywhere. It’s Hilton’s upscale property portfolio that’s the greatest source of its economic moat, and it’s unlikely to crumble, even if a coming economic downturn is more painful than expected.

At writing, shares of HLT trade at 33.7 times trailing earnings and 4.3 times sales. Hilton still seems priced with growth in mind. Indeed, investors are feeling upbeat following the company’s recent profit forecast hike. Hilton’s hotel peers are also feeling confident amid the ongoing travel recovery from the dark days of COVID-19.

Whether the travel and leisure recovery can continue moving forward in a recession year remains to be seen. Regardless, Hilton’s brand strength should help it outdo rivals and capture market share as it powers through recession headwinds.

In any case, many analysts are as optimistic as Hilton’s managers.

What is the Price Target for HLT Stock?

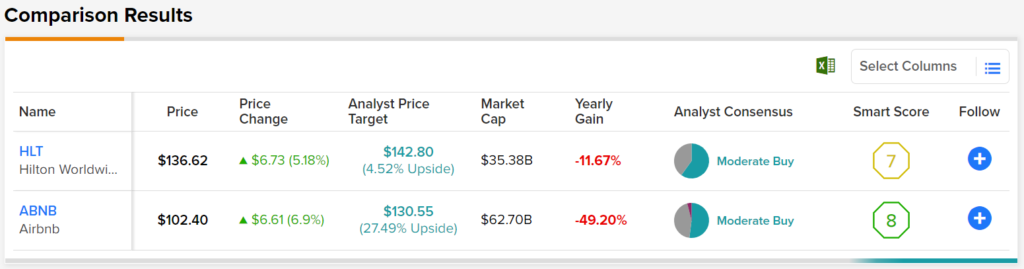

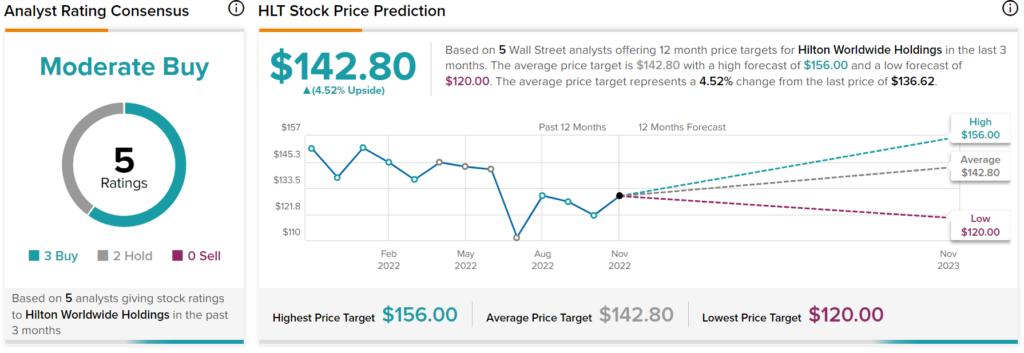

Wall Street remains a fan of Hilton in the face of a recession, with a “Moderate Buy” consensus rating among the analyst community. This is based on three Buys and two Holds assigned in the past three months. The average HLT stock price target of $142.80 implies 4.52% upside.

Airbnb (ABNB)

Airbnb is a disruptive company that’s used technology to disrupt the stays industry. Alternative accommodations have been a hit among millennials looking for genuinely unique experiences. The novel concept has brought forth many competitors hungry for a slice of the market. Despite this, Airbnb has used its extensive network to its advantage.

Airbnb’s strength and moat come from its network effects. Still, Airbnb doesn’t “own” the properties it helps hosts rent out to guests. In that regard, Airbnb’s asset-light model may be less compelling to the likes of an asset-heavy hotel chain.

Since going live on the Nasdaq in 2020, it’s been a painful ride, with most investors sitting on sizeable losses. Airbnb stock peaked during the euphoric early days of 2021, plunging around 55% to its trough of around $95 per share.

Indeed, investors may have overvalued ABNB stock last year, perhaps overemphasizing the firm’s ability to disrupt the stays market. While Airbnb will always be a force to be reckoned with, hotel stays aren’t going anywhere, given the magnitude of their amenities and consistency of service across properties.

Despite Airbnb’s shortcomings versus traditional hotel plays, a recession could bode well for alternative accommodations on the lower end of the price range. Hosts have the flexibility to really lower prices to levels that hotels may not be able to keep up with.

In any case, stays demand could remain robust going into a (potentially mild) recession year, but don’t expect ABNB stock to recover in a hurry. The valuation multiple (40 times trailing earnings and 7.8 times sales) remains hot, and competition remains fierce. A growth multiple is warranted versus a traditional hotel play, but just how much a premium is a question mark with rising rates.

What is the Price Target for ABNB Stock?

Wall Street loves ABNB stock, with a “Moderate Buy” consensus rating based on 13 Buys, 11 Holds, and one Sell assigned in the past three months. The average ABNB stock price target is $130.55, implying 27.49% upside potential from here.

Conclusion: Analysts Expect More Upside from ABNB Stock

Hilton and Airbnb are travel plays that’ll continue duking it out as travel looks to keep recovering in a recession year. I view Hilton as a less risky play at this juncture. Analysts disagree. They prefer ABNB stock by a wide margin.