Investors rushed to Coinbase (NASDAQ:COIN), a cryptocurrency exchange, to trade Bitcoin (BTC-USD) in the past as they were afraid of missing out on its brisk rally. This benefited the company and its financials. However, Coinbase has lost its FOMO (Fear of Missing Out) appeal among retail investors, emphasized Mizuho Securities analyst Dan Dolev. The analyst is bearish about COIN stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

In a note to investors dated September 12, Dolev wrote that FOMO no longer tempts investors to “trade Bitcoin when prices rise the way it did in prior years.” He believes this could hurt COIN’s prospects as most of its transaction revenue (about 95%) is generated through retail trades. Further, on August 29, Dolev said crypto volumes remain very low, implying little retail interest.

In addition, the analyst believes that the launch of a Bitcoin ETF (Exchange Traded Fund) will increase competition for COIN and “put pricing pressure on retail take rates.” Given these headwinds, Dolev sees the rally in COIN stock as “unsustainable.” Moreover, his price target of $27 implies a significant downside potential of 64.78% from current levels.

While Dolev has a bearish outlook on COIN stock, let’s look at what the analysts’ consensus estimate indicates.

Is Coinbase a Buy or Hold?

Coinbase stock has gained nearly 117% year-to-date. Investors cheered COIN’s efforts to reduce costs significantly, which was one of the reasons for the year-to-date rally in its share price. Further, the company posted positive adjusted EBITDA in two consecutive quarters of 2023.

However, the significant price appreciation and lower trading volume keep analysts sidelined on COIN stock.

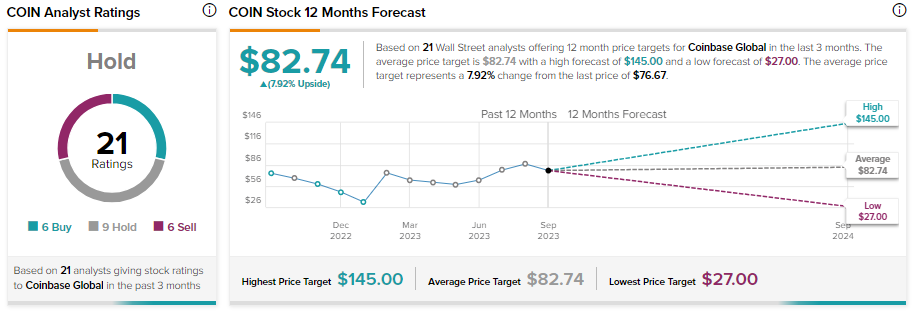

With six Buy, nine Hold, and six Sell recommendations, COIN stock has a Hold consensus rating on TipRanks. Moreover, analysts’ average price target of $82.74 implies a limited upside potential of 7.92% from current levels.

Bottom Line

Coinbase’s heightened focus on cost and efficiency and improving adjusted EBITDA augur well for its growth. However, lower volumes and concerns over transaction revenue could pose challenges and limit the upside potential.