“Water, water, everywhere, nor any drop to drink.”

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

So wrote Coleridge, in his epic poem The Rime of the Ancient Mariner, and while most of us probably won’t get trapped in the doldrums on the equator, we probably should give more thought to water.

To start with, water shortages are far more common than are usually assumed. As Jim Andrew, chief sustainability officer of PepsiCo, points out, more than 2 billion people worldwide don’t have regular access to safe water for drinking or washing, and another 4 billion people deal with such shortages for at least one month per year. In recent decades, as the global population has increased, so have the pressures on the world’s supply of fresh water. In fact, according to UNICEF, half of the global population could face water scarcity challenges by 2025.

As pressures on water systems and supplies increase, it’s only natural that more companies and innovators will step up to meet the challenge – to develop water handling equipment of greater efficiency, able to maintain and move supplies with less waste.

Against this backdrop, we’ve looked up the details on two interesting stocks that operate in just this field, producing water handling equipment for a wide range of purposes. According to TipRanks database, these are Buy-rated equities with double-digit upside potential – and even better, each has found recent approval from one of the Street’s 5-star analysts.

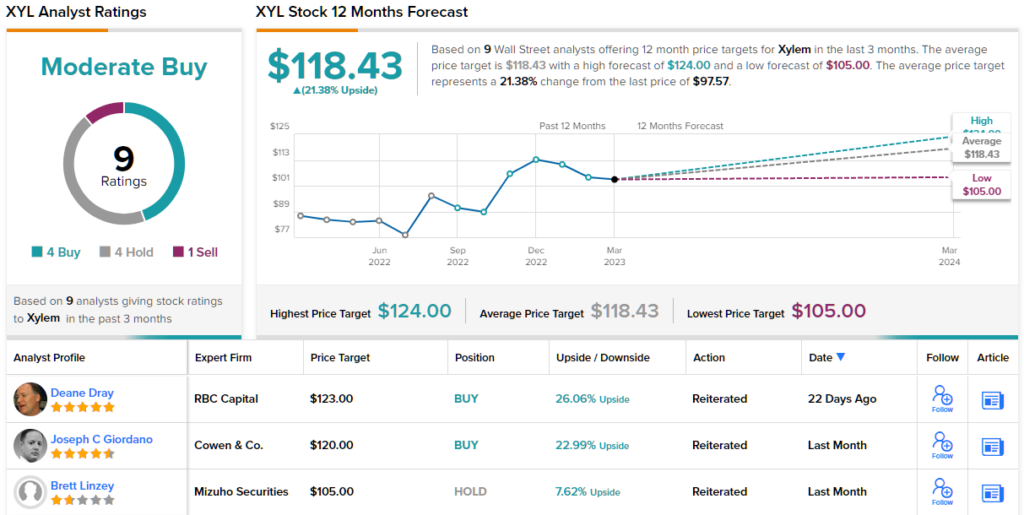

Xylem, Inc. (XYL)

First up is Xylem, a water technology provider based in New York State. The company’s customers include public utilities, industrial firms, and residential, commercial, and agricultural water suppliers, and Xylem does business in over 150 countries. The company works in both water infrastructure and wastewater transport and treatment, and its products include pumps, valves, heat exchangers, dispensing equipment, and treatment and testing equipment.

While Xylem’s stock has been volatile lately, the company has shown positive financial results in recent quarters. The most recent report, from 4Q22, tells the story.

In that recent quarter, Xylem’s top and bottom line both beat expectations. At the top line, the revenue total of $1.5 billion was $90 million higher than the forecasts, while at the bottom line, the non-GAAP EPS of 92 cents beat the forecast by 13 cents, or 16%. On a year-over-year basis, the quarterly revenues were up 13.5%, and the EPS was up 46%.

In January of this year, Xylem announced that it had entered a ‘definitive agreement’ to acquire the water treatment technology firm Evoqua. The transaction will be conducted entirely in stock, and the combined entity will have an estimated enterprise value of $7.5 billion.

Also of note, earlier this month the City of Buffalo announced that the partnership between the Buffalo Sewer Authority and the Xylem had improved the city’s ability to prevent system overflows, and had contributed to $145 million in savings for the municipality.

Covering this stock for Stifel, 5-star analyst Nathan Jones sees the Evoqua deal as a key point, and writes of Xylem’s prospects: “We think Xylem’s clearly laid-out strategy to build the leading global smart water infrastructure company, while significantly improving the operations of the company over the next several years, provides the potential for solid investment returns over the long run in lower-volatility water markets. With the announcement of the acquisition of Evoqua Water Technologies, we believe this is a low risk acquisition and integration with strong opportunity to drive higher growth together than alone coupled with compelling cost synergies opportunities.”

For Jones, this adds up to a Buy rating on the shares, and his $124 price target implies a one-year gain of 27% for Xylem. (To watch Jones’ track record, click here)

Overall, XYL shares have picked up 9 recent analyst reviews, and these include 4 Buys, 4 Holds, and 1 Sell – for a Moderate Buy consensus rating. The stock is selling for $97.57 and its $118.43 average price target suggests an upside potential of 21% on the one-year time frame. (See XYL stock forecast)

Pentair plc (PNR)

The second water treatment stock we’ll check out is Pentair, a company focused on ‘smart, sustainable water solutions.’ The company markets its products to industrial water management companies, residential and commercial water suppliers, and agribusinesses. Pentair’s product line includes water supply and disposal, pool and spa equipment, water softeners and filters, filter housings, supply and disposal pumps, as well as valves, tanks, and accessories.

Pentair has shown a consistent ability to beat its earnings forecasts, and maintained that in its last quarterly report. In the fourth quarter of last year, the company showed a bottom line non-GAAP EPS of 82 cents; while this was down from 87 cents in the prior year quarter, it beat the analyst forecast by 3 cents. At the top line, the company posted quarterly revenues of $1 billion, up a modest 1.45% y/y, and $9.51 million ahead of expectations.

Along with these quarterly beats, Pentair finished the year with $364 million in cash from operations and $283 million in annual free cash flow. In February, the company announced its next quarterly dividend payment, scheduled for May 5 at a rate of 22 cents per common share. While the annualized payment of 88 cents only yields a modest 1.66%, the dividend is highly reliable.

For Bryan Bair, 5-star analyst with Oppenheimer, the bottom line here is that Pentair holds a solid position in its industry and is likely to continue showing gain.

“We view Pentair as well positioned for MSD normalized core growth and margin/returns expansion, with benefits from healthy through-the-cycle market demand (80% resi/non-res water exposure), enhanced focus on innovation/differentiation and digital capabilities, and PIMS cost initiatives supporting above-average EPS growth. We anticipate continued/solid Pool demand (comp-related fears overdone), sustained Water Solutions growth (commercial recovery levered by high-margin Manitowoc Ice), self-help actions, and strategic capital deployment will drive further upside vs. forward earnings and cash flow expectations,” Bair opined.

Against this backdrop, it’s no wonder that Bair rates PNR shares an Outperform (i.e. Buy), and his price target of $67 implies it has a one-year upside potential of ~30%. (To watch Blair’s track record, click here)

All told, Pentair gets a Moderate Buy rating from the analyst consensus, based on 12 recent analyst ratings that break down to 8 Buys, 2 Holds, and 2 Sells. The stock’s average price target of $61.25 implies share appreciation of ~19% from the current trading price of $51.35. (See PNR stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.