Shares of Alphabet (NASDAQ: GOOGL) continued to be on a downslide in pre-market trading on Friday as the tech giant’s Q4 results were a miss both on the top line and bottom line.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

More worryingly, for investors, advertising revenues declined 3.6% year-over-year to $59 billion in Q4. Overall, GOOGL’s Services revenue which includes advertising, Search, and others were down 2% year-over-year to $67.8 billion.

The company’s management stated on its Q4 earnings call that a major reason for a drop in advertising revenues was a major pullback in advertising spending by advertisers as the macroeconomic environment remained challenging.

While even YouTube’s advertising revenue of $7.96 billion fell short of analyst expectations of $8.25 billion, the company remained confident about YouTube’s growth trajectory over the long term. GOOGL intends to focus on YouTube’s growth through a multi-point strategy.

This includes increasing user engagement through YouTube Shorts which currently has daily views exceeding 50 billion and ramping up investment in its subscription offerings. The company is also looking at improving YouTube’s reach through connected TV and making YouTube “more shoppable” over the long-term.

When it comes to Artificial Intelligence (AI), Alphabet CEO Sundar Pichai stated that he believes that the company is in a “great position as AI reaches an inflection point” and that it “has been preparing for this moment since early last year.”

The company remains optimistic about its Google Cloud business which saw its revenues jump 32% year-over-year to $7.3 billion in Q4.

When it comes to its outlook, the company expects to take a hit in the range of $1.9 billion to $2.3 billion in terms of severance costs, mostly in Q1 as it announced layoffs of around 12,000 of its employees. In addition, GOOGL anticipates incurring costs of another $500 million “related to exiting leases to align our office space with our adjusted global headcount look. This will be reflected in corporate costs.”

Following the results, MKM Partners’ top-rated analyst Rohit Kulkarni expects the stock “to remain under pressure over the near term as we don’t foresee a positive catalyst over the next few months. Incremental cost-cutting initiatives might help the shares break out above our current PT. All else being equal, we’d be aggressive buyers on weakness below “low $90s.”

The analyst is currently upbeat about the stock with a Buy rating and a price target of $120, indicating an upside potential of 11.4% at current levels.

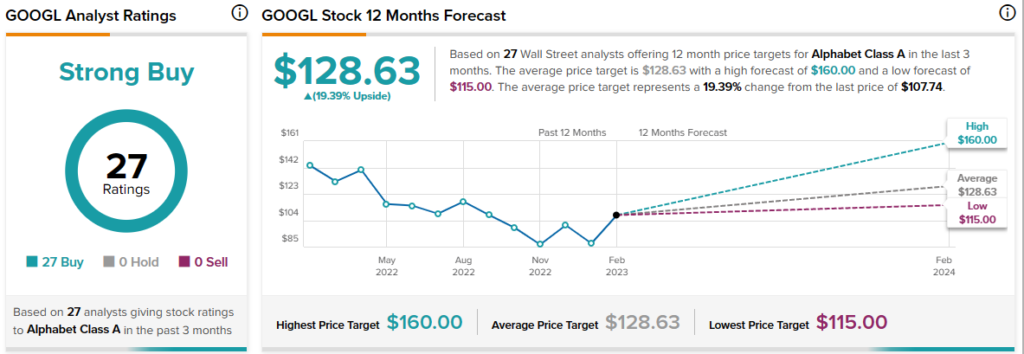

Overall, Wall Street analysts remain bullish about GOOGL stock with a Strong Buy consensus rating based on a unanimous 27 Buys.