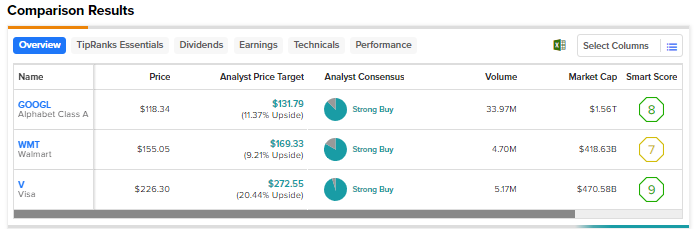

The ongoing macro uncertainty and stock market volatility could make it difficult for retail investors to choose the right stocks for their portfolios. During these times, it could be a good idea to consider mega-caps, stocks with a market capitalization of over $200 billion, as they are generally associated with large, well-established companies with strong potential for long-term growth. Using TipRanks’ Stock Comparison Tool, we placed Alphabet (NASDAQ:GOOGL, GOOG), Walmart (NYSE:WMT), and Visa (NYSE:V) against each other to pick Wall Street’s most attractive mega-cap stock.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Alphabet (NASDAQ:GOOGL, GOOG)

While Alphabet shares have risen 34% year-to-date, they lag the impressive rally seen in stocks of tech giants like Amazon (NASDAQ:AMZN) and Meta Platforms (NASDAQ:META), which have rallied more than 51% and 131%, respectively. Heightened regulatory scrutiny, higher competition due to the rapid adoption of generative artificial intelligence (AI) tools like OpenAI’s ChatGPT, and the impact of macro pressures on digital ad spending are weighing on Alphabet.

Recently, Bank of America conducted a user survey on conversational AI tools, involving over 1,100 U.S. internet users aged 18-55, to measure user AI chatbot activity and intentions. On Monday, the firm’s analyst Justin Post noted that the survey, which focused on heavy internet users, indicated that 59%, 51%, and 34% use ChatGPT, Microsoft’s (NASDAQ:MSFT) Bing, and Google’s Bard, respectively. If only allowed to use one AI chatbot, 49% said that they prefer ChatGPT, 29% chose Bing, and 21% Bard.

Overall, the survey confirmed the usage concerns pertaining to Google, given the strong adoption of ChatGPT. While 19% of the overall users indicated they would use Google Search less due to ChatGPT and Bing, 45% said that they would use Google Search more with the addition of conversational AI. Despite concerns over competition, Post reiterated a Buy rating on GOOGL with a price target of $128, noting that large language model (LLM) usage can benefit core search.

Is Alphabet a Good Stock to Buy?

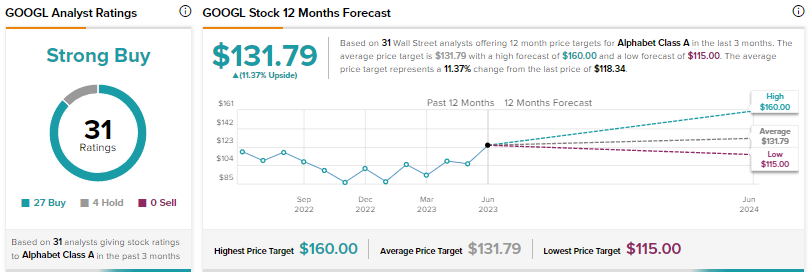

Despite the concerns discussed above, Wall Street remains bullish on Alphabet, thanks to its dominance in the search market and solid fundamentals.

Wall Street’s Strong Buy consensus rating on Alphabet is based on 27 Buys and four Holds. The average price target of $131.79 implies 11.4% upside.

Walmart (NYSE:WMT)

Walmart’s value deals continue to attract customers, especially amid high inflation. Last month, the big-box retailer raised its full-year guidance after posting better-than-anticipated fiscal first-quarter results. Walmart’s adjusted EPS grew 13% to $1.47 in Q1 FY24, driven by a 7.6% growth in revenue and a higher operating margin that gained from the retailer’s cost management efforts. However, gross margin contracted as consumers spent more on groceries and less on higher-margin general merchandise.

Meanwhile, Walmart’s omnichannel strategy, which leverages the company’s extensive physical presence and digital channels, continues to attract customers. In Q1 FY24, Walmart’s global e-commerce revenue grew 26%. In particular, the U.S. e-commerce revenue increased 27%, supported by the company’s pickup and delivery services. Additionally, the scope for Walmart’s advertising business appears lucrative, given the company’s vast reach.

On Monday, Morgan Stanley analyst Simeon Gutman reiterated a Buy rating on Walmart with a price target of $160. Gutman highlighted that his firm’s latest survey revealed a record nearly 21.5 million Walmart+ members, which reflects more than 3 million inflection compared to the prior survey.

In addition, the overlap with Amazon Prime declined compared to prior surveys, indicating the growing awareness and appeal of Walmart+.

What is the Target Price for WMT Stock?

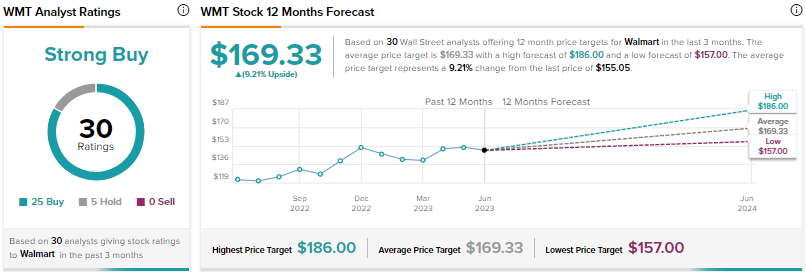

With 25 Buys and five Holds, Walmart scores a Strong Buy consensus rating. The average price target of $169.33 implies 9.2% upside. Shares have advanced 9.4% year-to-date.

Visa (NYSE:V)

Payments behemoth Visa impressed investors with upbeat fiscal second-quarter results despite the ongoing uncertainty. The rebound in international travel spending boosted Q2 FY23 results, with travel in and out of Asia reaching 2019 levels.

Adjusted EPS increased 17% to $2.09, with revenue rising 11% to $8 billion. The top line gained from a 24% increase in cross-border volume (in constant dollars), a 10% rise in payments volume, and a 12% growth in processed transactions to 50.1 billion. The company expects its international growth trajectory to remain largely unchanged in the fiscal third quarter.

On May 30, Visa provided a business update, according to which the company’s May U.S. payments volume increased 5%, cross-border volume increased 17%, while processed transactions were up 9%.

Reacting to the mid-quarter update, Bank of America analyst Jason Kupferberg said that he views the company’s update as modestly positive for shares in the wake of the worries around consumer spending and month-to-date underperformance of the stock.

Kupferberg noted that travel-related cross-border volume growth, excluding intra-Europe transaction, accelerated to 139% of 2019 levels in May compared to 131% in April. Overall, the analyst remains optimistic about the quality of Visa’s business model, “recession-resistance, secular tailwinds, and reasonable valuation.”

Is Visa Stock a Buy, Sell, or Hold?

Wall Street has a Strong Buy rating on Visa stock based on 19 Buys and one Hold. The average price target of $272.55 implies 20.4% upside. Shares have risen 9% year-to-date.

Conclusion

While Wall Street is bullish on the potential of all the three mega-cap stocks discussed here, they see higher upside in Visa. As per TipRanks’ Smart Score System, Visa has a better smart score of nine compared to Alphabet and Walmart, which have scores of eight and seven, respectively. Visa’s dominant position in the payments industry and the rapid shift to digital transactions bode well for the company’s future growth.