Investment banking giant Goldman Sachs (NYSE:GS) reported one of its biggest earnings misses last month. The company is shifting gears between its several businesses and trying to bring down mounting losses (in certain segments) and costs. With the possible impact of an impending recession further pulling down the profitability of the bank, I would rather stay on the sidelines. I am neutral on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Goldman Reported Its Biggest Earnings Miss in a Decade

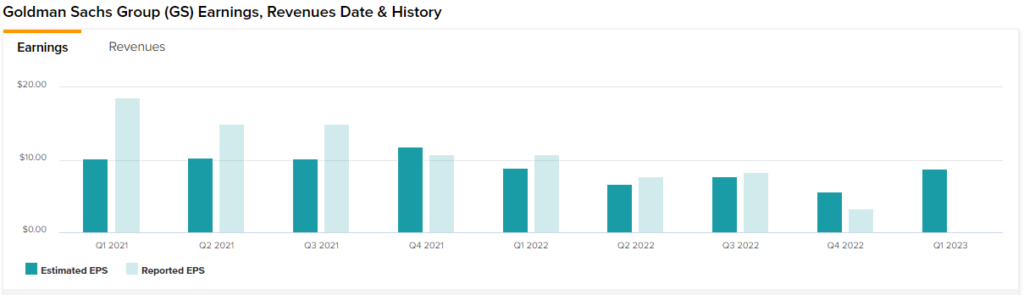

On January 17, Goldman Sachs reported disappointing Q4 results. Both the top and bottom lines failed to meet the Street’s expectations amid a slump in deals and weak consumer business results. Earnings of $3.32 per share declined 69.3% year-over-year due to higher costs and came in much lower than the consensus estimate of $5.56, marking the biggest miss over the past 10 years.

Revenues also slid 16% to $10.59 billion, lagging expectations by $320 million due to significantly lower net revenues in Asset & Wealth Management (down 27% year-over-year) and Global Banking & Markets (down 27% year-over-year).

Goldman is Shifting Gears, Reorganizing, and Cutting Costs

Goldman is in the process of revamping its business model, shifting its focus back to its core businesses. The bank’s businesses have always been capital-intensive. The company is making a shift from a “balance sheet intensive asset management business to a client-oriented fee-based business,” as highlighted by management during the Q4 earnings call. This implies that there will be a greater focus on fees from asset and wealth management, as well as platform solutions, going forward.

According to a recent Wall Street Journal report, the Federal Reserve has been actively investigating GS’ Retail & Consumer Banking business — Marcus. The probe includes an assessment of whether proper monitoring and control systems were utilized before scaling up the business that reported mounting losses. GS reported that the unit had $3 billion in accumulated losses since 2020. Likewise, the company is now planning to significantly reduce its focus on Marcus which was launched in 2016.

In addition, Goldman Sachs’ asset management unit is significantly lowering its alternative investments worth $59 billion over the next few years. The said investments had a significant negative impact on FY22 earnings.

The company has even changed its reporting of business segments. Asset and Wealth Management have been combined into one segment, with Investment Banking and Markets becoming the second segment. The third new segment – Platform Solutions, will include its fintech platforms, including transaction banking, cards platform, consumer partnerships, and its point-of-sale lending business GreenSky.

Its Platform Solutions business registered 135% year-over-year growth in net revenues in FY2022. However, it was loss-making, with a net loss of $1.7 billion reported in FY2022.

Earlier this month, the company announced thousands of layoffs to be executed in January — the biggest job cuts the company has seen since the subprime crisis.

Hinting more struggle for the company, last week, it was revealed that CEO David Solomon’s pay was cut by almost 30% to $25 million for 2022. While the company cited a challenging operating environment as the reason, the move left doubts in the minds of investors. Perhaps, they will get more details of what’s coming next during Goldman Sachs’ investor day scheduled on February 28.

GS is Building Its Reserves in Anticipation of a Recession

In lieu of an impending recession, banks are slowly building their loan loss reserves. During Q4, GS increased its provision for credit losses by 89% sequentially and 183% year-over-year to $972 million. On a full-year basis, its provision for credit losses was $2.72 billion, up a huge 661%. The bank attributed the jump to a growing credit card portfolio, macroeconomic and geopolitical concerns, and net charge-offs.

During the Q4 earnings call, CFO Denis Coleman commented that the reserve builds “initiated over the balance of this past year and will continue through the following year.” Higher-than-normal loan loss reserves, in case of a more severe recession, could be a bigger drag on profitability in the coming quarters.

Is GS Stock a Buy, Sell, or Hold, According to Analysts?

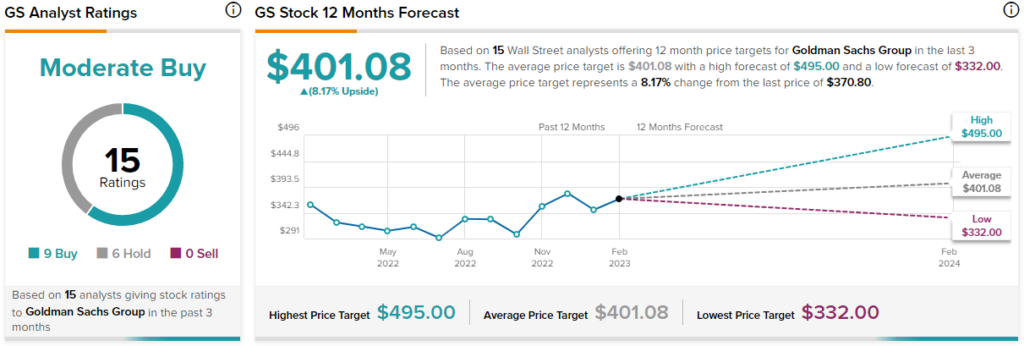

Turning to Wall Street, analysts are cautiously optimistic about Goldman Sachs stock and have a Moderate Buy consensus rating, which is based on nine Buys and six Holds. GS stock’s average price forecast of $401.08 implies 8.17% upside potential.

In terms of its valuation, GS stock looks relatively cheap at a price-to-book of around 1.2x compared to peers like Morgan Stanley (NYSE:MS), which is trading at higher levels of 1.8x.

On the negative side, Goldman’s return on tangible equity (ROTE) fell to 4.8% during the recently reported fourth quarter compared to 16.4% in the prior-year period. For FY2022, ROTE fell to 11% compared to the 24.3% reported in FY2021. These numbers clearly indicate declining profitability at Goldman Sachs over the past year.

Concluding Thoughts: Stay Away Until Positive Signs Emerge

The company is clearly in the middle of strategic realignment and trying to fix several issues simultaneously. Successful implementation of its business reorganization may take several quarters, if not more.

Therefore, I will remain on the sideline and may consider buying the stock if the restructuring begins to translate to better earnings and profitability metrics.