Markets have been sending mixed signals lately. A combination of factors – from heightened geopolitical tensions and renewed friction in U.S.–China trade relations to a surge in gold prices – has set off caution lights for investors.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Even so, the main stock indexes remain near record highs. Tech stocks, led by the so-called ‘Magnificent 7,’ have continued to power market gains, fueled by enthusiasm around AI. Over the past year, the tech-heavy NASDAQ has advanced by 23.5%.

The strength of this rally and the market’s AI fixation have raised concerns about a potential bubble. However, Goldman Sachs’ chief global equity strategist Peter Oppenheimer argues that we’re not there yet. While acknowledging the risks, he believes investors still have room to benefit from current trends before valuations reach truly excessive levels.

“Bubbles tend to develop when there is a combined surge in stock prices and valuations to an extent that the aggregate value of companies associated with the innovation exceed the future potential cash flows that it is likely to generate. Valuations of the technology sector are becoming stretched but not yet at levels consistent with historical bubbles. While it appears we are not in a bubble yet, high levels of market concentration and increased competition in the AI space suggest investors should continue to focus on diversification,” Oppenheimer noted.

Against this backdrop, Goldman Sachs analysts are drawing attention to two lesser-known stocks with sound upside potential of at least 40% in the months ahead. While the broader markets hover near record highs, these picks are actually trading at depressed levels, but the Goldman analysts think that is about to change. Here’s a closer look at them, using data drawn from the TipRanks platform.

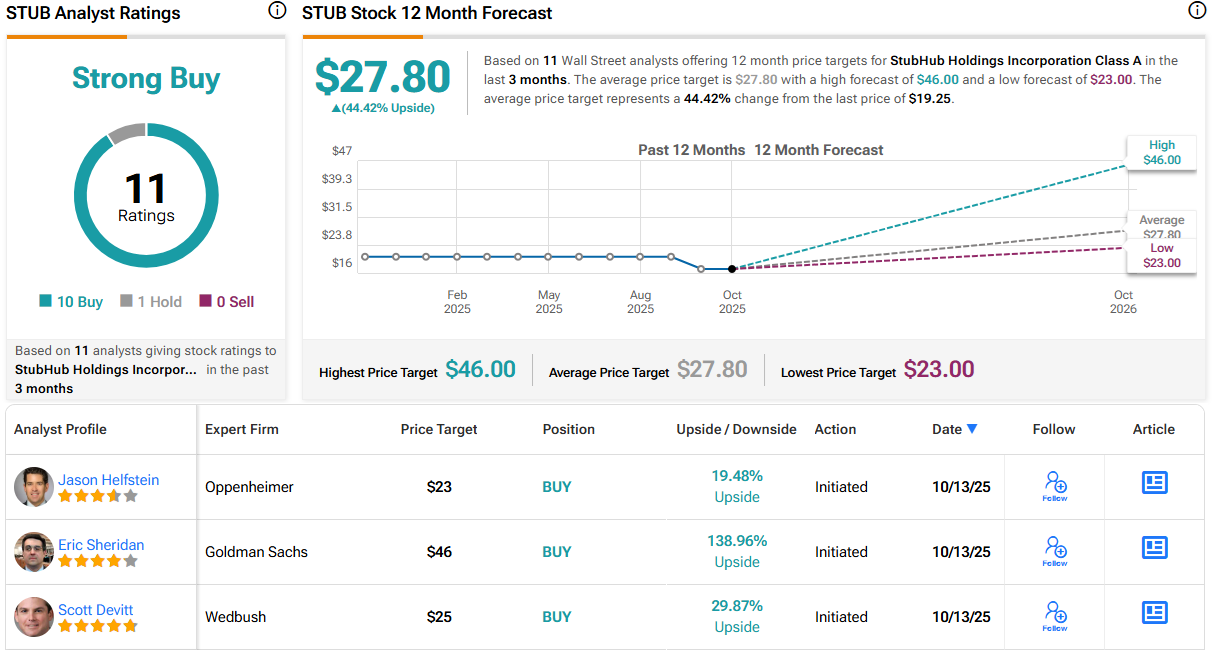

StubHub Holdings (STUB)

Ticketed venues – concerts, plays, sports events, festivals, and the like – are increasingly popular entertainment attractions. StubHub, which was founded in 2000, offers users a comprehensive platform to access live event tickets. Eventgoers can use the online system or the mobile app to peruse events of all kinds and to order tickets in advance. StubHub operates under two brand names – its eponymous activities are in the North American market, while internationally the company goes by the name of Viagogo.

Using StubHub’s service is easy. The system starts by showing ticketed events near the user’s location; search options allow for expanded searches or searches narrowed to specific events or dates. Users will need an account and login to purchase tickets. For now, StubHub operates as a secondary ticket issuer but is working to become a direct ticket issuer. In early September, as an example, the company announced a multi-year agreement with Major League Baseball (MLB) for direct issuance. The partnership is set to begin for the 2026 baseball season and makes StubHub’s direct issuance technology available to MLB.

Also in September of this year, StubHub went public through an IPO. The company had tried several times over the past few years to hold an IPO; public launches in 2024 and earlier in 2025 were canceled due to ‘choppy’ market conditions or increased volatility. In the offering last month, however, StubHub successfully put 34,042,553 shares on the market at a price of $23.50 each, raising gross proceeds of approximately $800 million. We should note that STUB shares have fallen since the IPO and are now trading 18% below the IPO price.

However, Goldman analyst Eric Sheridan likes what he sees in StubHub, particularly the company’s potential to enter the direct issuer market.

“We view StubHub to be positively levered to the large and growing ticketing market – which will continue to scale as consumers continue to prioritize experiences over products (a multi-decade secular trend),” the analyst said. “Today, StubHub is a share leader in the global secondary ticketing market and we expect the company will be able to take additional share (both in North America and Internationally), while also scaling into the $132bn original issuance market opportunity (through direct issuance business) and growing its advertising revenues in the years ahead.”

Sheridan goes on to give STUB a Buy rating, along with a price target of $46 that suggests a robust one-year upside of 139%. (To watch Sheridan’s track record, click here)

Overall, STUB’s Strong Buy consensus rating is based on 11 reviews, including 10 Buys and just 1 Hold. The stock’s $27.80 average price target suggests a 44% upside from the $19.25 trading price. (See STUB stock forecast)

Kaspi.kz (KSPI)

Kaspi.kz is hardly a household name in the West – but it is a major player in the Central Asian fintech world. Kaspi.kz is the top online financial services platform in Kazakhstan, a large nation of 20 million people, which, like Russia, straddles the boundary between Europe and Asia. Kaspi.kz trades on Wall Street and boasts a market cap of ~$15 billion.

The company’s business revolves around its three mobile app platforms, which offer payment, marketplace, and fintech services to its customers. In the second quarter of this year, the payments platform boasted over 14 million active customers and handled transactions worth a total of 10.7 trillion Kazakh tenge (approximately $20 billion in US currency). That figure was up 21% year over year. The company’s online marketplace platform, which allows customers to shop online for a wide range of products from diverse merchants, boasted 8.4 million active customers in 2Q25, making 74.5 million purchases with a gross merchandise value (GMV) of 1.587 trillion tenge (just under US$3 billion). On the marketplace, the customer total was up 10% year over year, the purchases were up 35%, and the GMV was up 15%.

Kaspi.kz’s fintech platform puts financial and banking services at the customer’s fingertips. The company allows customers to make deposits and take out loans and currently has approximately 6 million customers with active deposit accounts and 6.4 million with active loans.

In January of this year, the company made a move to expand when it purchased a controlling interest in the Turkish e-commerce platform Hepsiburada. Kaspi.kz acquired a 65.4% stake in the Turkish firm for an agreed price of US$1.127 billion. Kaspi.kz paid US$600 million cash up front and made the final payment of US$526.9 million, also cash, in July of this year.

This stock has caught the eye of Mikhail Butkov, who notes that the shares are down significantly (currently 31%) in the past 12 months – but still offer plenty of opportunities for investors. In his coverage for Goldman, Butkov writes, “We believe short-term risks are already factored into the stock price while its medium-term growth trajectory and potential positive catalysts for 2026-27 are underappreciated by the market. Our valuation models and peer analysis suggest Kaspi warrants a higher valuation given our forecasted 2026-27E EPS growth of around 23% and Return on Equity (ROE) of approximately 50%. Key catalysts anticipated for 2026-27 include GMV acceleration; policy rate cuts supporting Net Interest Margin (NIM) and cost of risk recovery; and a resumption of dividends following the strategic pause in dividend payments for 2025 to fund growth initiatives, particularly its Turkey expansion, as well as the potential for a share buyback.”

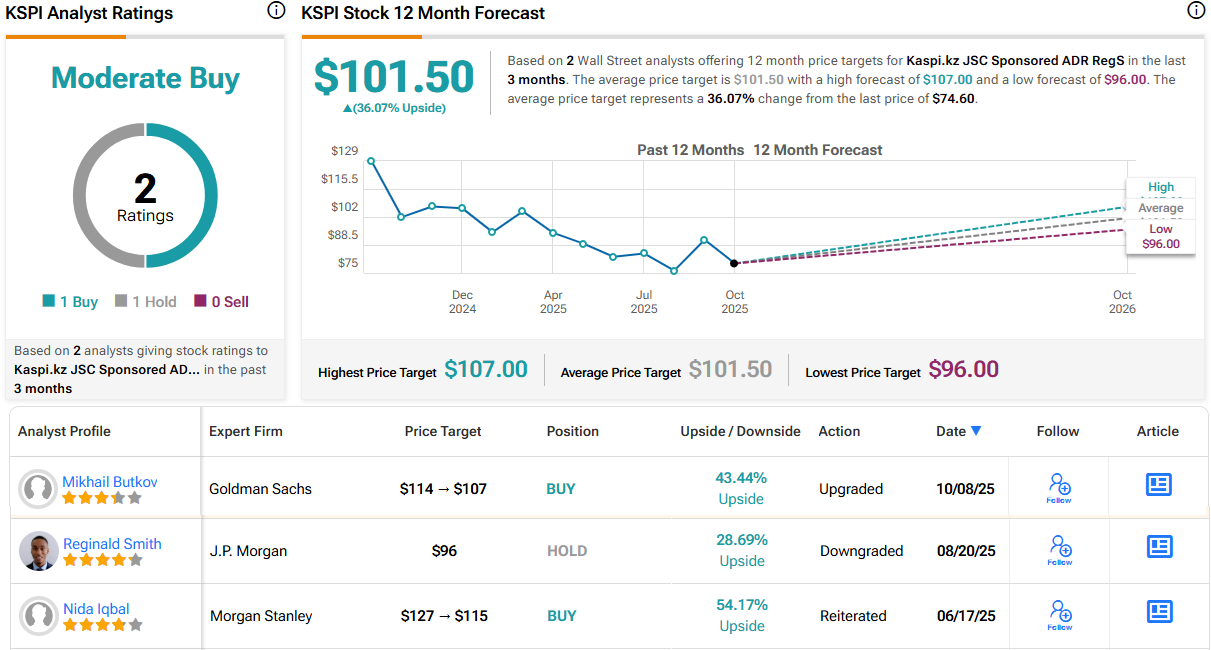

Quantifying his stance, Butkov puts a Buy rating on these shares and backs that with a $107 price target that points toward a 43.5% upside for the coming year. (To watch Butkov’s track record, click here)

There are only two recent analyst reviews on file for Kaspi.kz, and the even split (1 Buy and 1 Hold) gives the stock a Moderate Buy consensus rating. The shares are currently priced at $74.60, and the $101.50 average target price implies a 12-month gain of 36%. (See KSPI stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.