The end of earnings season always offers an opportunity to figure out what lies in store for the following months. With the Q2 results for companies in the energy sector now available, it’s time to look toward the key investment themes ahead in the space.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

That’s exactly what Goldman Sachs analysts have been doing. While the energy team remains “constructive” on Energy Service companies as a whole, moving forward, they see the “importance of idiosyncratic self-help drivers” as a key theme that will drive outperformance.

“We believe there are a number of attractive buy-rated stocks that can drive sequential growth, margin expansion and multiple expansion even in a range bound commodity environment with Brent near $80/bbl,” the team explained in a recent note.

Against this backdrop, the Goldman Sachs experts have pinpointed two specific names that offer such “idiosyncratic opportunities.” In fact, they are not alone in their endorsement of these stocks. According to the TipRanks platform – they are both rated as Strong Buys by the Street’s analysts. Let’s take a closer look.

Weatherford International (WFRD)

For investors with a keen interest in the energy sector, oilfield services unfold as a lucrative realm. These companies offer vital services that major producers rely upon to finalize well projects, implement specialized equipment, extract oil and gas from beneath the earth’s surface, and proficiently store the resulting products. While exploration and production outfits often claim the spotlight, a substantial capability gap exists between the discovery of subterranean oil reserves and the operational management of the wells responsible for extraction. This is precisely the niche where companies like Weatherford come into play, adeptly bridging the critical gap and ensuring the smooth continuity of operations.

Weatherford can trace its business roots back more than 80 years, and has a built-up wealth of experience. Today, the company operates in 75 countries on six continents, and brings digital-age, high-end automation technology into the traditional heavy industry of the oil field. Among Weatherford’s unique tech advantages is its single-trip offshore completion system, that allows both upper and lower installations to be completed in the same venture for greater efficiency and faster startups of offshore oil projects. The company also makes extensive use of RFID-enabled technology in its installations – again, an innovation that improves efficiency.

The company’s ability to deliver results has led to strong financial performance over the past several quarters – which in turn has pushed up the firm’s share price. The stock has risen 70% so far this year, riding on the company’s solid results.

Looking at those results, we find that Weatherford reported $1.27 billion at the top line in 2Q23. This was up 7% year-over-year and beat the forecast by $38.5 million. The company’s cash generation has been improving over the past year too. In Q2, Weatherford generated $201 million in cash from operations, and an adjusted free cash flow of $172 million. These figures were up y/y from $60 million and $59 million respectively. In the company’s bottom line, EPS, at $1.14 per share, was 4 cents below expectations.

Looking ahead, Weatherford bumped up its expectations for the full-year 2023. The company is now projecting mid-to-high teens revenue growth for this calendar year, along with more than $400 million in adjusted free cash flow.

Evidently, investors were willing to forgive the earnings miss and focus on the plethora of other positive metrics. This is a stance shared by Goldman Sachs analyst Ati Modak, who sees Weatherford’s increasing full-year guidance and ability to deliver offshore efficiencies as key points.

“WFRD was among the only companies that revised guidance this earnings season, which we believe is a reflection of company specific drivers and increasing visibility around the strength of the business. We also believe that the additional deleveraging of the remaining secured notes and the potential initiation of a dividend are positive catalysts for the stock,” Modak opined.

“WFRD is one of the few high international exposure service stock ideas that allow investors to gain exposure to secular themes of spare capacity expansion and momentum in offshore. As such, we believe that with continued execution and strength in earnings revisions, the stock should ultimately re-rate higher,” Modak went on to say.

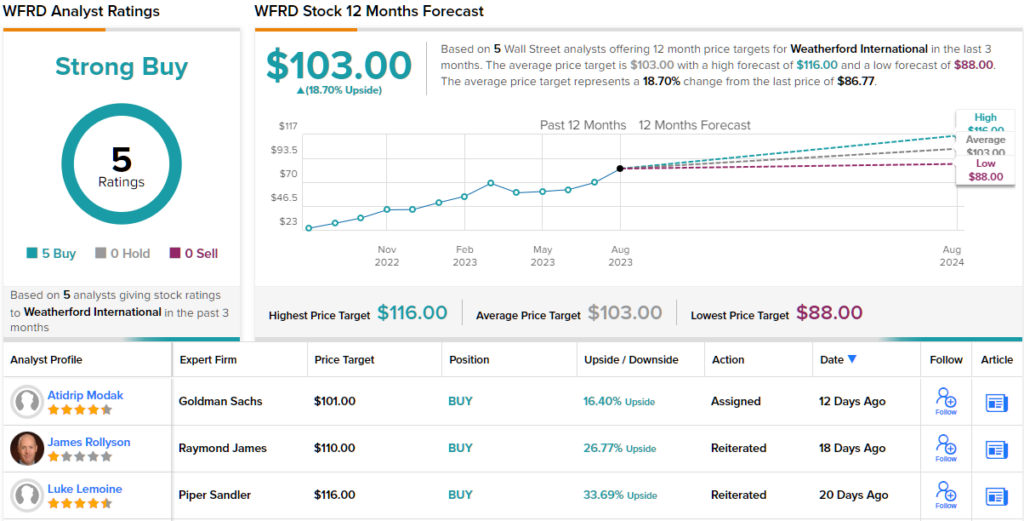

Accordingly, Modak rates WFRD shares a Buy, and his price target of $101 implies a 16% upside for the coming 12 months. (To watch Modak’s track record, click here)

Overall, Weatherford has a Strong Buy consensus rating based on 5 unanimously positive recent analyst reviews. The stock is selling for $86.77 and its average price target, at $103, is slightly more bullish than the Goldman view, suggesting ~19% gain on the one-year horizon. (See Weatherford stock forecast)

Baker Hughes Company (BKR)

Next up is Baker Hughes, another leader in oil field services. This company works with advanced industrial tech, developing and deploying the latest advances to smooth the path for industrial firms looking to streamline clean and reliable energy solutions. Baker Hughes provides services directly at the oil patch, in petroleum and natural gas production, as well as in supporting areas such as natural gas liquefaction and gas turbines.

Baker Hughes has a global reach, with some 55,000 workers on the job in over 120 countries. Oil fields are known as dangerous workplaces, but Baker Hughes was able to report 217 ‘perfect HSE’ days last year – that is, days without accidents causing harm to people, equipment, or the environment.

In July, Baker Hughes reported its 2Q23 results, and showed beats across the board. The revenue total came to $6.3 billion at the top line, beating the forecast by almost $49 million and growing 25% year-over-year. The bottom line, a non-GAAP EPS reported at 39 cents, was 6 cents better than the estimates.

Solid financial results also brought solid cash flows. Baker Hughes generated $858 million in cash from operations during Q2, for an 86% y/y gain. This included $623 million in free cash flows, which was up from just $147 million in the prior year Q2.

The company also maintained its dividend, declaring on July 27 a 20-cent per common share payment. This was up 5% from the previous quarter, and up 11% y/y. The 80-cent annualized common share dividend gives a yield of 2.25%.

This stock has caught the attention of Goldman Sachs’ 5-star analyst, Neil Mehta, who notes its strengths as a cash cow and as a defensive move.

“The company’s operational turnaround takes shape, driving improvement potential in EBITDA margins and free cash flow conversion, in addition to a strong macro in both its segments… We continue to see BKR as an attractive defensive stock with elements of a turnaround story and exposure to strong macro that should drive estimate change potential over time,” Mehta opined.

Quantifying his stance, Mehta puts a Buy rating on BKR shares, and he sets his price target at $42. That target indicates room for ~19% one-year upside potential from current levels. (To watch Mehta’s track record, click here)

Overall, there are no fewer than 18 recent analyst reviews of Baker Hughes shares, and they break down 16 to 2 in favor of Buys over Holds – for a Strong Buy consensus rating. The stock is currently priced at $35.33 and holds a $40 average price target, suggesting it will gain 13% in the year ahead. (See BKR stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.