The story for most of 2022 has been one of soaring inflation but with 2023 about to enter the frame, the plot appears to be taking a positive turn.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

The October inflation report came in much better than expected and took Wall Street by surprise. The good news, according to Goldman Sachs’ Chief Economist Jan Hatzius, is that the trend is set to continue into next year.

“We expect a significant decline in inflation next year, with the core PCE measure falling from 5.1% currently to 2.9% by December 2023,” said Hatzius. “Our forecast reflects three key factors: 1) the easing in supply chain constraints in the goods sector, 2) a peak in shelter inflation post-reopening, and 3) slower wage growth driven by the ongoing rebalancing of the labor market.”

Despite recent gains, all the major indexes are still down for the year, with the NASDAQ, in particular, still firmly planted in bear territory.

Meanwhile, Hatzius’ analyst colleagues at the banking giant have homed in on two names that are primed to shoot higher over the coming months – by the order of 40% or more. We ran these tickers through the TipRanks database to see what other Wall Street’s analysts have to say about them. Here’s the lowdown.

Twilio Inc. (TWLO)

We’ll start with Twilio, a leading CPaaS (communication platform as a service) company. Twilio provides a cloud communications platform that enables customer engagement via a set of programmable communication tools. The platform lets developers insert voice, messaging, video, and email abilities into their apps. That Twilio is at the forefront of this secular trend is clear to see from its enviable client list; it includes eBay, Shopify, Airbnb, IBM, Reddit, and Uber, amongst many others.

Businesses are increasingly pivoting toward digital channels, a trend which only accelerated during the pandemic. Twilio stock was a major beneficiary and soared to giddy heights, but the tables have turned on former high-flying yet unprofitable growth names. Twilio has suffered badly from the change of sentiment. The shares have been obliterated to the tune of 79% year-to-date and took a proper thrashing just recently following the company’s Q3 report.

In the quarter, revenue climbed by 32.8% year-over-year to $983 million, in-line with Street expectations. The company delivered adj. EPS of -$0.27, beating the analysts’ call for -$0.35. So far, so good, however, investors sent shares tumbling due to a disappointing outlook; the company sees Q4 sales coming in between $995 million and $1.005 billion, while consensus was looking for $1.07 billion.

While the stock has been trending south for most of the year, Goldman Sach analyst Kash Rangan is still a fan.

Assessing the print, the analyst said, “With a fundamental/valuation reset now in the rearview, we believe Twilio can better execute on its revenue/margin targets, due to: 1) Best-in-class communications suite and burgeoning software portfolio that remains under-penetrated relative to +$100bn TAM opportunity, and 2) Management’s pivot to more disciplined growth should manifest in consistent margin accretion closer to the high-end of its 100-300 bps target range (leaner GTM org., layoffs/hiring slowdown, higher reliance on self-serve channel).”

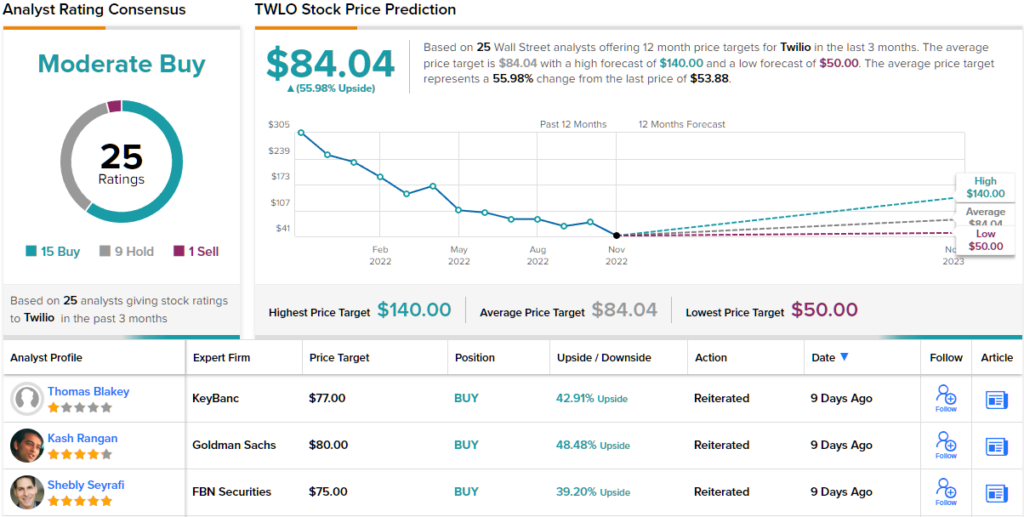

To this end, Rangan has a Buy rating on Twilio shares backed by a price target of $80. Should the figure be met, the stock will be changing hands for a 48% premium in twelve months time. (To watch Rangan’s track record, click here)

Overall, TWLO holds a Moderate Buy rating from the analyst consensus view, based on 15 Buys, 8 Holds, and 1 Sell. The stock’s $84.04 average price target indicates room for about ~56% upside from the current share price of $53.88. (See Twilio stock forecast on TipRanks)

Bank of N.T. Butterfield & Son (NTB)

The next Goldman-backed name we’ll look at offers an entirely different value proposition. With its headquarters in Bermuda, the Bank of N.T. Butterfield & Son provides a wide range of banking services, including corporate banking, retail banking and wealth management. Essentially, the bank serves as the holding company for an offshore banking operation with 10 worldwide locations but with a focus on Bermuda and the Cayman Islands, spots where it is a market leader.

Revenues and earnings have been steadily rising throughout the year. In the latest quarterly report, for Q3, the top-line showed $141.1 million, amounting to a 13.2% increase on the same period a year ago, while also meeting Street expectations. Non-GAAP EPS of $1.16 beat the forecast, coming in $0.05 above the $1.11 consensus estimate.

This allowed the company to support a solid dividend. NTB declared its Q4 dividend at 44 cents per common share. At the current rate, the dividend annualizes to $1.76 and brings a yield of 5.37%. The yield is almost triple the average found in the broader markets.

All of this has Goldman Sachs’ Will Nance bullish on NTB. The analyst sees the stock as “a good opportunity to gain exposure to an extremely low risk balance sheet, with structurally higher returns relative to U.S. bank peers as a result of its tax neutral jurisdictions and its 30%+ market shares in its core markets of Bermuda and Cayman.” The analyst added, “We believe this should drive attractive shareholder returns for income oriented investors and insulate the business from a slowdown in the broader economy.”

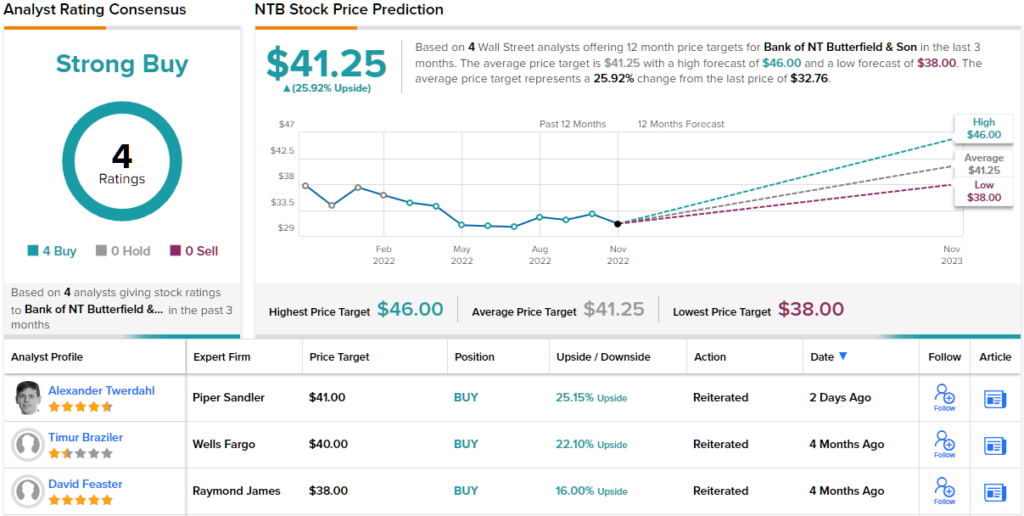

Accordingly, Nance rates NTB shares a Buy, while his $46 price target makes room for 12-month gains of ~40%. (To watch Nance’s track record, click here)

Other analysts don’t beg to differ. With 4 Buy ratings and no Holds or Sells, the word on the Street is that NTB is a Strong Buy. The average target clocks in at $41.25, suggesting the shares will climb ~26% higher over the one-year timeframe. (See NTB stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.